Re: Yes Virginia...It's a Bubble...

today's u.s. labor numbers don't make china's export prospects look any better.

so what does a bubble with chinese characteristics look like when it pops? we have remarked at times in the past on the potential advantages of a command economy in such situations. where can/will they apply stimulus and in what form? more ghost cities? more infrastructure? if they're truly serious about wanting to transition to a more consumption-based economy they should give everyone health insurance and a pension - those moves would promote spending. that last suggestion doesn't seem very likely, however.

-

Re: Yes Virginia...It's a Bubble...

China will have no option but to continue to devalue the yuan unless the Fed introduces QE4. This will give them a brief respite but will not last. Painfully the market thinks that QE was about inflating commodity prices and when QE4 demonstrates that it is not, China will turn down again.Originally posted by touchring View Post

That is not going to last: http://www.zerohedge.com/news/2015-1...est-their-debt

Earlier today, Macquarie released a must-read report titled "Further deterioration in China�s corporate debt coverage", in which the Australian bank looks at the Chinese corporate debt bubble (a topic familiar to our readers since 2012) however not in terms of net leverage, or debt/free cash flow, but bottom-up, in terms of corporate interest coverage, or rather the inverse: the ratio of interest expense to operating profit. With good reason, Macquarie focuses on the number of companies with "uncovered debt", or those which can't even cover a full year of interest expense with profit.

The report's centerprice chart is impressive. It looks at the bond prospectuses of 780 companies and finds that there is about CNY5 trillion in total debt, mostly spread among Mining, Smelting & Material and Infrastructure companies, which belongs to companies that have a Interest/EBIT ratio > 100%, or as western credit analysts would write it, have an EBIT/Interest < 1.0x.

As Macquarie notes, looking at the entire universe of CNY22 trillion in corporate debt, the "percentage of EBIT-uncovered debt went up from 19.9% in 2013 to 23.6% last year, and the percentage of EBITDA-uncovered debt up from 5.3% to 7%. Therefore, there has been a further deterioration in financial soundness among our sample."

[IMG]file:///C:/Users/Andrew/AppData/Local/Temp/msohtmlclip1/01/clip_image001.jpg[/IMG]

To be sure, both the size (the gargantuan CNY22 trillion) and the deteriorating quality (the surge in "uncovered debt" companies) of cash flows, was generally known.

What wasn't known were the specifics of just how severe this bubble deterioration was for the most critical for China, in the current deflationary bust, commodity sector.

We now know, and the answer is truly terrifying.

Macquarie lays it out in just three charts.

First, it shows the "debt-coverage" curve for commodity companies as of 2007. One will note that not only is there virtually no commodity sector debt to discuss, at not even CNY1 trillion in debt, but virtually every company could comfortably cover their interest expense with existing cash flow: only 4 companies - all in the cement sector - had "uncovered debt" 8 years ago.

[IMG]file:///C:/Users/Andrew/AppData/Local/Temp/msohtmlclip1/01/clip_image002.jpg[/IMG]

Fast forward to 2013 when things get bad, as about a third of all corporations are now unable to cover their annual interest expense, even as the total addressable corporate debt has soared to CNY4 trillion for just the commodity sector.

[IMG]file:///C:/Users/Andrew/AppData/Local/Temp/msohtmlclip1/01/clip_image003.jpg[/IMG]

And then in 2014, everything just falls apart. Quote Macquarie, "more than half of the cumulative debt in this sector was EBIT-uncovered in 2014, and all sub-sectors have their share in the uncovered part, particularly for base metals (the big gray bar on the right stands for Chalco), coal, and steel."

Compared with the situation in 2013, while almost all sub-sectors did worse in 2014, but things appear to have worsened faster for coal companies as more red bars have moved beyond the 100% critical level for EBIT-coverage.

It means that last year about CNY2 trillion in debt was in danger of imminent default.

[IMG]file:///C:/Users/Andrew/AppData/Local/Temp/msohtmlclip1/01/clip_image004.jpg[/IMG]

The situation since than has dramatically deteriorated.

So are we now? Macquarie again: "Given the slumps in metal and coal prices so far this year, it�s quite likely the curve will have deteriorated further for commodity firms this year, with total debt getting better in the meantime."

In other words, it is safe to assume that up to two-third of Chinese commodity companies are now at imminent danger of default, as they can't even generate the cash to pay down the interest on their debt, let alone fund repayments.

We fully expect this to be the source of the next market freakout: when the punditry turns its attention away from macro China, which has more than enough problems to begin with, and starts to focus on the cash flow devastation in China at the micro, or corporate, level.Leave a comment:

-

Re: Yes Virginia...It's a Bubble...

It's amusing to see that every commodity company in every country is going to go bankrupt because of "China's weakness", except for Chinese companies, at least for now.

Leave a comment:

-

Re: Yes Virginia...It's a Bubble...

Japanese Shipping Company Files for Bankruptcy Protection Over Glencore Fallout

Updated on

The Chinese economic slowdown that�s caused a rout in mining giant Glencore Plc�s stock price claimed a victim in Japan�s shipping industry, sparking a jump in thedefault risk for other competitors and trading companies reliant on the commodities and energy business.

Daiichi Chuo KK filed for bankruptcy protection in Tokyo on Tuesday with 120 billion yen ($1 billion) in liabilities, in the biggest failure by a publicly-traded Japanese company this year. The cost to insure shipper Mitsui OSK Lines Ltd.�s debt against nonpayment surged 43 basis points last month and touched 156, the highest since October 2013, while trading house Mitsui & Co.�s credit-default swaps climbed to the most since August 2012, CMA data show. The Markit iTraxx Japan CDS index rose 19 basis points in September.

China is Japan�s biggest trading partner and its deceleration is rippling through Prime Minister Shinzo Abe�s economy, which probably slipped back into recession after unexpectedly weak industrial production in August, according to a report by JPMorgan Chase & Co. on Wednesday. Daiichi Chuo filed for bankruptcy protection this week after four consecutive years of losses amid plunging freight rates and too many ships built to supply commodities to Asia�s biggest economy.

�If you look at the big picture, China�s weakness is the reason why Daiichi Chuo is heading for default,� said Mana Nakazora, the chief credit analyst in Tokyo at BNP Paribas SA.

Leave a comment:

-

Re: Yes Virginia...It's a Bubble...

Is Stock Investing for Suckers?

By Pam Martens and Russ Martens: September 30, 2015

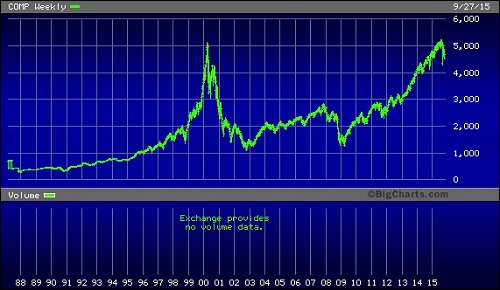

On March 10, 2000 the Nasdaq stock market, which is supposed to hold the technology and startup companies that will keep America globally competitive in the future, closed at a high of 5,048.62. Yesterday, more than 15 years later, it closed at 4,517.32, a decline of 10.5 percent from its level of March 2000.

Nasdaq Index Chart Since 1988

To fully grasp the unprecedented nature of the Nasdaq bubble of 2000, one has to look at where the three big stocks are today that made that 5,000 mark possible 15 years ago. Just three stocks, Microsoft, Cisco, and Intel, were valued at a market cap of $1.89 trillion in 2000. As of yesterday�s close, those three stocks had a combined market cap of $616.137 billion � a shrinkage of 67 percent after more than 15 years.

Much of the hype, as well as the money, that surrounded Microsoft, Cisco and Intel in early 2000, has moved to Apple today, which also trades on the Nasdaq. As of yesterday�s close, Apple commands a market value of $621.9 billion.

Back on March 19, 2000 the Silicon Valley Business Journal reported that one analyst was predicting Cisco was headed toward a market cap of $1 trillion. (Its market cap at yesterday�s close was $129.7 billion, down 80 percent from 2000.)

The article noted that �Thirty-seven investment banks recommend either a �buy� or a �strong buy.� None recommend a �sell� or even a �hold.� �

On March 23 of this year, an analyst at Cantor Fitzgerald made the same frothy market prediction that Apple would hit a $1 trillion market cap. It�s lost $122 billion in market cap since that call.

The Federal government has two decades of evidence that the integrity of Nasdaq as a stock market has been repeatedly compromised. Yet it does nothing material to rein in the abuses.

The excesses leading up to the crash of 2000-2002 and the crash of 2008-2009 resulted from a highly orchestrated wealth transfer machine on Wall Street that was allowed to operate with impunity from the Federal regulators. As we reported in 2008:

[Regarding the Nasdaq boom of the late 90s] �First, Wall Street firms issued knowingly false research reports to trumpet the growth prospects for the company and stock price; second, they lined up big institutional clients who were instructed how and when to buy at escalating prices to make the stock price skyrocket (laddering); third, the firms instructed the hundreds of thousands of stockbrokers serving the mom-and-pop market to advise their clients to sit still as the stock price flew to the moon or else the broker would have his commissions taken away (penalty bid). While the little folks� money served as a prop under prices, the wealthy elite on Wall Street and corporate insiders were allowed to sell at the top of the market (pump-and-dump wealth transfer).

�Why did people buy into this mania for brand new, untested companies when there is a basic caveat that most people in this country know, i.e., the majority of all new businesses fail? Common sense failed and mania prevailed because of massive hype pumped by big media, big public relations, and shielded from regulation by big law firms, all eager to collect their share of Wall Street�s rigged cash cow.

[Regarding the 2008 market]�The current housing bubble bust is just a freshly minted version of Wall Street�s real estate limited partnership frauds of the �80s, but on a grander scale. In the 1980s version, the firms packaged real estate into limited partnerships and peddled it as secure investments to moms and pops. The major underpinning of this wealth transfer mechanism was that regulators turned a blind eye to the fact that the investments were listed at the original face amount on the clients� brokerage statements long after they had lost most of their value.

�Today�s real estate related securities (CDOs and SIVs) that are blowing up around the globe are simply the above scheme with more billable hours for corporate law firms.

�Wall Street created an artificial demand for housing (a bubble) by soliciting high interest rate mortgages (subprime) because they could be bundled and quickly resold for big fees to yield-hungry hedge funds and institutions. A major underpinning of this scheme was that Wall Street secured an artificial rating of AAA from rating agencies that were paid by Wall Street to provide the rating. When demand from institutions was saturated, Wall Street kept the scheme going by hiding the debt off its balance sheets and stuffed this long-term product into mom-and-pop money markets, notwithstanding that money markets are required by law to hold only short-term investments. To further perpetuate the bubble as long as possible, Wall Street prevented pricing transparency by keeping the trading off regulated exchanges and used unregulated over-the-counter contracts instead. (All of this required lots of lobbyist hours in Washington.)�

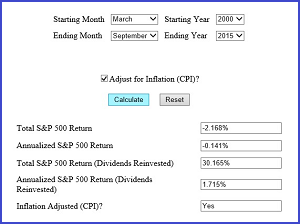

S&P Returns, March 2000 to Present With Dividends Reinvested and Adjusted for Inflation

You are likely thinking that Nasdaq doesn�t reflect the performance of the broader market. You will likely be shocked to see the performance of the Standard and Poor�s 500 index of stocks starting from March 2000 to September 2015, courtesy of this handy online calculator. Even with dividends reinvested, the S&P has delivered a paltry 1.715 percent annualized return since March 2000 on an inflation adjusted basis. And that�s before paying taxes on dividends.

Even if you are invested in diversified, actively managed stock mutual funds, over a working lifetime you are likely to lose two-thirds of your money because of the management fees, according to a PBS Frontline report.

This would also be a good time to remember that stock market performance following epic financial crashes that ravage the economy can be hazardous to your wealth. Following the 1929 crash, the stock market did not set a new high until 1954 � 25 years later.

Yesterday, the Securities and Exchange Commission announced that it will hold a hearingon October 27, open to the public, on the stock market�s structure. The SEC has had 15 years since the revelations of the rigged market of 2000 and 7 years since the worst market collapse since the Great Depression to actively engage in reining in the abuses. Yesterday�s announcement was decidedly too little too late.

Leave a comment:

-

Re: Yes Virginia...It's a Bubble...

Warren Pollock on the hollowing out economy.

Leave a comment:

-

Re: Yes Virginia...It's a Bubble...

touchring you have reminded me of the real role assigned to the 95%Originally posted by touchring View Post

Be silent

Consume

DieLeave a comment:

-

Re: Yes Virginia...It's a Bubble...

ZIRP helps lay the foundation for extreme speculation, over-the-top stock buybacks, etc. all of which have been discussed at length on the 'tulip.Leave a comment:

-

Re: Yes Virginia...It's a Bubble...

one pension crisis arises from the assumption that corporate pension funds will make 8% or more per year, ad infinitum. this assumption allows for smaller pension contribution from those companies which still have defined benefit plans.Originally posted by GRG55 View Post

the other pension crisis comes from the fact that the vast majority of people no longer have defined benefit plans, they've saved too little and they've invested poorly. the fact that there is no safe asset with a decent yield just makes it harder for people in that positionLeave a comment:

-

Re: Yes Virginia...It's a Bubble...

Pension funds tend to be heavy into bonds, large cap dividend paying equities and property holdings. All have performed magnificently under the Fed's policies. I don't understand where this "pension crisis" is sourced from?Originally posted by don View PostLeave a comment:

-

Re: Yes Virginia...It's a Bubble...

ZIRP, albeit not the only factor, is at the heart of the pension implosion. So while the very idea of pensions is ridiculed, this connection is seldom mentioned. Sounds conspiratorial, doesn't it (aka wealth transfer on a grand scale).Originally posted by thriftyandboringinohio View PostLeave a comment:

-

Re: Yes Virginia...It's a Bubble...

Pinus parviflora 'Miyajima' | Japanese White Pine

Donor: Diazo Iwasaki |

In Training Since 1855

The good professors at the Fed seem to forget that time scales matter.

A typical human being like me earns money for 30 or 40 years.

I can't afford to earn zero interest on my money for half my working lifetime.

Neither can you.

Our life savings are not bonsai trees that can be tended for a hundred and sixty years like the one above.Leave a comment:

-

Re: Yes Virginia...It's a Bubble...

Soft Power On Parade - what could be more benign sounding, and evasive, then forward guidance

It's right up there with Federal Reserve . . . .Leave a comment:

-

Re: Yes Virginia...It's a Bubble...

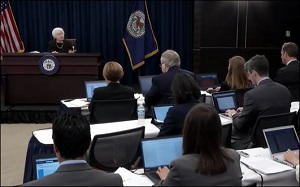

Reporter�s Bare-Knuckle Question to Janet Yellen Is Part of Markets� Turmoil

By Pam Martens and Russ Martens: September 22, 2015

Ann Saphir, Reuters, Asking Question at Janet Yellen�s Press Conference, September 17, 2015

Last Friday, one day after the Fed�s announcement that it would hold rates steady at the zero bound range, the Dow Jones Industrial Average dropped 290 points. It calmed itself a little yesterday but was off more than 200 points in the first five minutes of trading this morning.

One catalyst for the market gyrations is that Ann Saphir, a reporter for Reuters, boldly asked Fed Chair Janet Yellen at Thursday�s press conference what has been on many minds for more than a year: is the Fed ever going to raise interest rates or are zero rates here for the rest of our lifetimes. This was the exact exchange:

Ann Saphir: �Ann Saphir with Reuters. Just to piggyback on the global considerations, as you say, the U.S. economy has been growing, are you worried that given the global interconnecting this, the low inflation globally, all of the other concerns that you just spoke about that you may never escape from this zero lower bound situation.�

Janet Yellen: �So, I would be very� I would be very surprised if that�s the case. That is not the way I see the outlook or the way the committee sees the outlook. Can I completely rule it out? I can�t completely rule it out. But really that�s an extreme downside risk that in no way is near the center of my outlook.�

The Chair of the U.S. Central Bank admitting that she can�t completely rule out that the U.S. may never escape from its zero bound range of interest rates is very likely the most unnerving utterance to escape the tongue of a Central Banker since time immemorial.

It was two simple sentences from Yellen: �Can I completely rule it out? I can�t completely rule it out.� That was the honest academician speaking. And, given that Japan, one of the largest economies in the world, has been hovering between zero and one-half percent interest rates for the past 20 years, has plied its economy with Quantitative Easing and has now moved into desperation mode, buying up exchange traded funds and real estate investment trusts, Yellen�s answer was forthright.

The market turmoil stems from the reporter�s inclusion of the word �never� � that the United States �may neverescape from this zero lower bound situation.� While Janet Yellen may have thought she cushioned her remarks by calling it �an extreme downside risk,� Americans today fully grasp that Wall Street blowing itself up in 2008 was also an extreme downside risk but it happened, triggering a series of other highly unlikely extreme downside risks: the greatest economic collapse since the Great Depression, the biggest housing rout in seven decades, a global banking crisis that is still not fully under control, and the fastest expansion of the national debt in history. Since the repeal of the banking protections in the Glass-Steagall Act, 100-year financial floods are coming as frequently as afternoon showers in the tropics.

Janet Yellen�s Press Conference, September 17, 2015

The saga of global deflation took on more urgent overtones in overnight trading as commodity prices slumped further. Industrial metals took hits ranging from one percent to almost three percent with copper down 2.8 percent in early morning trade. At 10:22 a.m., West Texas Intermediate crude oil is down more than 2.36 percent at $45.58. European coal prices slumped to a record low according to a report from Bloomberg Business.

All of this is consistent with a global economy battling deflation and not consistent with a roster of Federal Reserve presidents filling the airwaves with chatter about when the Fed�s rate hike is coming. The gap between �never� and next month is simply laughable.

Janet Yellen apparently understands this �never� business has rattled markets and Washington insiders. She�s scheduled to deliver a speech this Thursday in Amherst, Massachusetts where she is likely to walk back any suggestion that the U.S. is locked in the zero bound range for eternity.

Just how seriously Fed officials worry that the U.S. could morph into Japan�s two-decade experience with deflation resides in this excerpt from a 2013 speech by William Dudley, President of the New York Fed:

�Let me start by briefly reviewing the experience of Japan and the United States. As you all know, Japan�s rapid economic ascent and investment boom came to an abrupt halt in the early 1990s with the bursting of a gigantic bubble in equities and real estate.

�Asset price deflation resulted in a huge decline in wealth. This led to a sharp fall in demand, a balance sheet squeeze for both businesses and households, and a large increase in problem loans for Japanese financial intermediaries. By some measures�such as the loss of wealth relative to the size of the economy�this was a bigger shock than the U.S. experienced in 2008. Growth slowed sharply and inflation fell.

�The Bank of Japan (BoJ) responded by reducing overnight interest rates from a peak of more than 8 percent in early 1991 to � a percent by the fall of 1995. Most studies of this period suggest that policy was generally appropriate given economic forecasts at the time, but too tight relative to the actual outcomes. Economic forecasts for Japan�both by the official community and by private sector agents�were consistently more optimistic than the actual outturns. It is noteworthy that as late as January 1995�on the eve of deflation�10-year Japanese Government Bond (JGB) yields were still at 4.7 percent.

�With the benefit of hindsight, we now understand that the disinflationary consequences of the asset price bust and financial stress where vastly more powerful than was widely realized at the time. As we later saw in the U.S., the forces of contraction and disinflation operated through many different channels�not just directly on household wealth, for example, but also through the impact of the asset price bust on the health of financial intermediaries and the supply of credit to households and businesses.

�Over time, the Japanese banking system came under mounting stress. This was a slow-motion crisis, as the assets were mainly loans that were not marked-to-market. Accounting practices and regulatory forbearance allowed banks to delay charging off bad loans and recapitalizing at the cost of impairing the availability of credit to new potential borrowers. A full-blown banking crisis finally materialized in 1997. Although some banks were recapitalized in 1999, the full regulatory response took several more years.

�The monetary and fiscal stimulus that was provided helped Japan avoid a deep recession. But expectations about future nominal income growth for both households and businesses ground lower over time. With inflation expectations sinking, inflation-adjusted real interest rates rose, and Japan became mired in deflation.

�While deflation is ultimately a monetary phenomenon, structural elements were also important. Long-term demographic factors added to the deflationary pressures and structural rigidities, and credit supply problems constrained the reallocation of resources to growth sectors. These structural factors made it substantially more difficult to escape the deflation trap.

�The Bank of Japan was active during this period. From the late 1990s onwards, it pioneered an extremely broad array of innovative tools�many of which were later adopted, in amended form, by the Fed and other major central banks. These included forward guidance on the future path of the policy rate, quantitative easing through purchases of government securities and private assets including asset-backed securities, equities and real estate investment trusts (REITs), a more quantitative inflation objective, and funding for bank lending.

�From my perspective, Japan�s experience with forward guidance for the policy rate, asset purchases and a more formal inflation goal are particularly instructive, as this helped inform the later use of such tools in the United States.

�In early 1999, the Bank of Japan said it would maintain its zero interest rate policy until �deflationary concerns� were �dispelled.� This commitment was lifted in August 2000, and the BoJ raised the policy rate by a quarter-point. However, the BoJ was subsequently obliged to reverse course, and reintroduced forward guidance in March 2001. This guidance was tied to the realization of a new inflation objective.

�With deflation intensifying, the Bank of Japan embarked on a quantitative easing (QE) program in 2001 designed to increase the size of the monetary base. The Bank of Japan engaged in purchases of JGBs that were large in scale, but confined to short-dated maturities. This reflected a view that such purchases primarily acted through the liabilities side of the central bank�s balance sheet�pushing up the amount of reserves in the banking system. Because the growth of the monetary base was deemed the goal of policy, it was logical to purchase short-dated assets, which could be allowed to run off once a sustainable recovery was in place.

�The downside of this approach was that the purchases did not change the composition of the private sector�s balance sheet very much because the policy essentially resulted in the exchange of one short-term risk-free asset for another. As a consequence, the purchases had only modest direct effects on financial conditions.

�Starting in 2006, when the initial wave of QE ended, the BoJ began to formalize its inflation goal in numerical terms. This was initially expressed as an �understanding of medium-to long-term price stability� based on individual policymakers� views. The inflation objective went through several iterations before being defined in 2012 as a Committee �goal� of a positive range of 2 percent or lower, with a lower interim goal of 1 percent.

�Following the onset of the global financial crisis in 2007-2008, Japan resumed QE, and gradually tightened the link between its policy actions and its objectives. By January 2012, the BoJ had committed to keep rates at the zero bound and to continue purchasing assets until the 1 percent goal was �in sight.�

�Several prominent Japanese experts have argued that there was a �start-stop� aspect to monetary policy during the 1990s and 2000s with reversals in policy beginning before deflationary expectations were eliminated. Fiscal policy also reversed abruptly on several occasions before economic recovery was firmly established. While Japan did enjoy a period of respectable real per capita growth in the mid-2000s, escape from deflation proved elusive.

�More than a decade after Japan�s bubble burst, the U.S. housing bubble burst. This exposed extensive vulnerabilities in our financial system and triggered a global financial crisis. Unlike Japan, we had the advantage of being able to learn from another nation�s recent experience. We applied what we understood to be the lessons from Japan, though with hindsight, perhaps not in every respect as completely as we could have.

�In particular, Japan�s experience reinforced the lessons of the Great Depression here in the U.S. and made us sensitive to the disinflationary force of an asset price bust and financial crisis. We recognized that we had to be very aggressive to prevent deflation and deflation expectations from becoming well entrenched.

�The Federal Reserve reduced short-term interest rates to nearly zero by late 2008�a little over a year and a half after the initial shock hit in August 2007. Immediately upon reaching the zero bound, we provided additional stimulus by expanding our balance sheet and deploying forward guidance on the policy rate. These actions, in the context of a strong commitment to both our inflation and employment mandates, succeeded in preventing deflation expectations from taking hold, even though real outcomes were disappointing. We also took steps to formalize our 2 percent inflation objective.� [Read the full speech here.]

It is now seven years since the Wall Street crash. The Fed has been at the zero bound range since December 2008 and the U.S. is currently seriously undershooting an inflation target of 2 percent. Ann Saphir was courageous to ask the question that is on so many of our minds.

Leave a comment:

Leave a comment: