Originally posted by Andreuccio

View Post

-

Re: Boom in the Doom

Yes, years ago I worked with folk who bought in Bakersfield and the Inland Empire and worked in LA. -

Re: Boom in the Doom

EJ writes in:Originally posted by GRG55 View PostNo argument. Modern houses are better, cars are better, bicycles are better, medical care is better, and on and on. Visiting a museum and living in one are two entirely different experiences. Whenever I visit the kinds of flats you're talking about I'm reminded that those who complain about how the dollar has losing 95% of its purchasing power over the past 60 years are losing sight of how much our standard and quality of living has improved, romantic ideas of rustic living aside. You may need $10 to buy a lunch that cost $0.25 during the 1930s but you can buy with a few month's salary a car that $1,000,000 would not buy 20 years ago.

In my original projection of the housing bust from Dec. 2005 I figured MacMansions were destined to be divided up into multifamily dwellings. I have no idea what might happen to improve the picture in Bakersfield. Maybe if oil prices rise to $200 there's something under the ground there that will help? I recall an oil pump or two in the area.

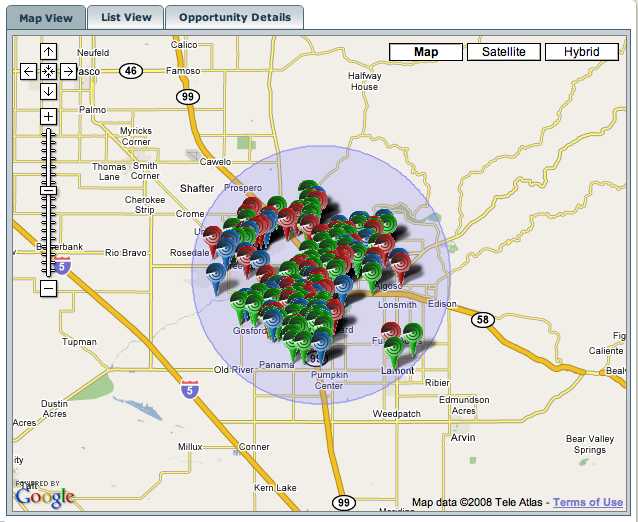

Pictured are 4399 homes within a 10 mile radius of Bakersfield now in

pre-foreclosure, foreclosure, or bank owned as of Feb. 7, 2008. From ForeclosureRadar.com

Leave a comment:

-

Re: Boom in the Doom

Did people really go as far as Bakersfield because of LA housing prices? It's over 100 miles and nearly 2 hours away (assuming no traffic, so double that during rush hour). I can see places like Santa Clarita, Palmdale, Ontario, Riverside. These are all about 60 miles, and less than 1 hour away. (Again, when there's no traffic.) Another advantage all these places have, desolate as they are, over Bakersfield, is that at least they are not Bakersfield.Originally posted by EJ View Post

Apparently, people would have been willing to move to the banks of the river Styx itself to buy a house, despite the commute.Leave a comment:

-

Re: Boom in the Doom

Originally posted by EJ View Post- Bakersfield doesn't qualify as one of those desirable locations I was thinking about. I know. For reasons I won't elaborate, I've made at least one visit to Bakersfield EVERY year since 2003 (and that's not exactly a cross-town jaunt from where I live).:p

- You and I are in agreement about the relative economic value of housing - I tried to make the same point.

- Only a small amount of the money that got poured into new housing in the past decade or more has been left half-finished. Yes, that part of it will prove to be useless, but so did a bit of the tech investment that was put in late in that game. Doesn't mean most of the stuff, in both cases, isn't of some use.

- Nothing caused me to rethink my views on modern housing more than the experience of hunting for a decent flat in Central London a few years ago. I got a concentrated lesson on the general state of the UK urban housing stock. My budget was not the issue. Just about every place I got dragged around to look at had serious problems - 150 year old plumbing that didn't work, problematic heating systems, electricals that threatened to burn the place down if one attempted to toast a crumpet, crumbling masonry and damp, damp, damp, mouldy interiors everywhere. What truly amazed was that the owner-occupied residences I was privileged to be invited to were largely in the same state, with only the occasional exception. We Canadians and Americans have it good in comparison.

Leave a comment:

-

Re: Boom in the Doom

Welcome, godrad, and thank you for the thoughtful and detailed post, very much in the iTulip spirit.Originally posted by godraz View Post

JoeSixpack's point is key: "I am more concerned than ever that the debt deflation and demand destruction might outpace the attempts to keep the system going..." (That's the iTulip user JoeSixpack, not to be confused with term Joe Sixpack, commonly used to describe the average, middle-class American.)

We predicted a demand implosion in 2000 and were quite wrong. We misjudged the Fed's Bag of Tricks (BOT). As it is not in the Fed's interest to make the entire contents of the public, but reveal only enough to convince markets to not panic but not so much to induce further moral hazard, it is something of an article of faith that the bag is not already nearly empty at a time when it better have a lot more really good policy stuff in it.

Ultimately our error was in underestimating the depth of the Fed BOT, the volume of the contents, and the effectiveness of their application. Perhaps we are overestimating it this time. Only time will tell.Leave a comment:

-

Re: Boom in the Doom

My cousin, actually. Was there a year ago with my niece. I pulled over to pick up a tumbleweed that she thought might make an interesting thing to bring back to my sister's house. I figured a tumbleweed was just a loose bush that got blown around until it was round. Turned out it was a very prickly loose bush and getting it into the back of my sister's BMW was no picnic, and she wasn't all that happy to see it, either.Originally posted by GRG55 View Post

I'm comparing the economic value of homes left over from the housing bubble to the economic value of fiber-optic cable left over from the telco bubble. The latter enables all kinds of economic activity, much as a road does, provided it isn't a road to nowhere. You can argue that a house does, too, but not if it's half finished, or abandoned and need of repair before it can be used, and is likely to stay abandoned because it is too far from areas of job growth. A house has only one use – to house people, who may or may have no economic reason for being where the house is. That's why Bakersfield came to mind. It only exists because the housing bubble made houses too expensive in suburban LA. As the housing in LA gets cheaper, guess what happens to the abandoned houses in Bakersfield?Leave a comment:

-

Re: Boom in the Doom

I disagree with the sentiment of this statement.Originally posted by FRED View Post

I don't believe that housing is ever a productive investment in an economy, in the sense that national resources consumed by housing do not create a sustainable economy by producing something that someone else in the world wants to purchase or exchange, for something they produce.

However, housing a nation's workers can't be done at zero cost. I believe that rapidly escalating national housing costs, which eventually manifest in some form of increased labour cost for employers, were a material contributor to the steady decline in US labour competitiveness (Who wants to invest in a new plant in Southern California when your workers have to paid so highly just to afford a place to house their kids?).

Coming back to the statement above...most of the houses were not Toll Brothers McMansions, and hell-holes like Bakersfield were "discovered" only late in the housing bubble (EJ: Does your brother-in-law still live there?).

Although construction booms always create quality problems due to lack of skilled trades, for the most part the housing stock built in the recent boom/bubble has far better plumbing and electrical, and more energy-efficient windows, doors, HVAC, and appliances than the post-war pink stucco bunagalows that our parents purchased.

The grossly overbuilt inventories and recent affordability trends suggest that the US will not have to divert nearly as much of its national investment resources into the housing sector for a long, long time. As housing deflates (even in US $ terms!!!) it will compound the improving labour competitiveness from the falling US$. Desirable jurisdictions with cheaper housing eventually attract both talent and employers.

As for the McMansions...well who knows, maybe some of them will be converted into apartments for students or sorority houses, just like some of the mansions of the formerly wealthy left over from the various booms & busts in the last century.Leave a comment:

-

Re: Boom in the Doom

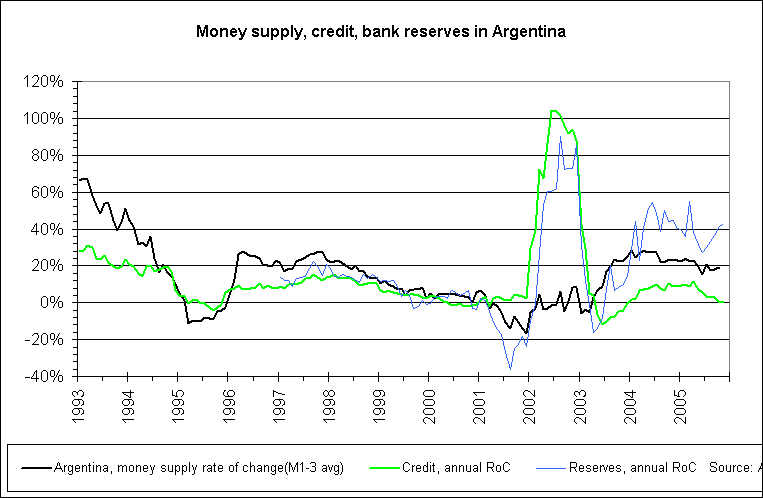

A friend of mine runs a company that was selling lots of oil and gas equipment into Argentina in the years before and during the inflation. He told me his partners and business contacts were doing all sorts of creative things to get out of the currency. Buying fully loaded 7-Series BMW sedans and storing them in secure garages out in the countryside (the 12 cyl models got cleaned out the dealerships first). Buying the whole family the most expensive 1st-Class round-the-world air tickets, make the first leg from BA to NY, cash in the rest of the ticket for US$ and stuff it into a Manhattan bank account.Originally posted by metalman View Post

No end to the ways we humans will find to get around the "rules", even bans on the ownership of gold, or capital controls.

Leave a comment:

-

Re: Boom in the Doom

OK. I don't know much when it comes to all the nuances of economic theory and practice, but I do appreciate this discussion and many of the insightful, open and learned contributions made here.

With respect to what EJ wrote above:

I think that is not entirely true. While it may be true for purposes of discussion among economically minded folk of the jargon and context involved, the understanding at street level is (no thanks to MSM, poor education, etc.) is one of much obfuscation.The measures of inflation have changed, not the meaning of the term.

For instance, we often read (or are told via TV) that "inflation" of whatever is on the rise, without any explanation as to what is actually causing this rise in prices. It's always couched in some other factor -- i.e., supply/demand, rising wages, other cost increases -- rather than telling it like it is: money and credit has been increased to such an extreme that our currency is depreciated in the process!

Yet right now, despite all the massive infusions of money/credit of late to fend off what akrowne identifies as "financial deflation" of falling prices of financial assets, which clearly is due to all the speculative excesses of the housing bubble coming home to roost, a lot of other prices have reset higher and look to stay high. Some things are in deflationary mode and others are not. And why they are isn't always so straight forward.

For instance we had the sudden price rise in oil, of which some would say our currency increase/depreciation finally caught wind of and responded to. To an extent I agree, but I also think there is another aspect of this problem that is overlooked or diminished, and that is the theory that any commodity in demand higher than readily available supply will accordingly price itself higher.

Without intending to open another can of worms I suspect that within this astonishing oil price rise was a signal of supply/demand constraints above and beyond simple monetary "inflation" explanation. Hence I think peak oil is a relevant factor too. Calling it "peak 'cheap' oil" doesn't alter it's geologic and production/extraction rate reality -- one of an absolute limit against unlimited demand.

In any event, metalman makes fine note that:

As a lay person in all the finer points of economics raised here, I agree that in this "inflation" discussion/debate, it is such distinctions that can cause befuddlement when not sufficiently distinguished beforehand as such!here we make a distinction between asset price inflation/deflation and p/c econ inflation/deflation in goods and stuff.

I think too jk's Argentine example follow-up reply also sheds light of further illustration upon "the lack of clarity we have most of the time when using these words." About which he concludes:

Baring an outright ban on the word, what I would like to see is that where the word "inflation" is used, we would be mindful that it can be and is often used too vaguely (particularly in common usage -- perhaps purposely so as to mask the real problem -- as opposed to distinct in-depth economic usage), and hence a definition/distinction should be established ahead of or clearly within the discussion context to try and minimize any confusion that could and does arise. At least to me.i think we should stop using these words except when specifying the currency in which the term is to be interpreted. or just stop using them altogether. reminds me of alfred kahn who, warned not to use the word "depression," said the country was heading for the worst banana in 45 years if it didn't get inflation [there's that pesky word again] under control.

Alas, as to whether Mish's dogged reporting on the deflationary housing/financial debacle and his apparent belief that it is or will result in a "catastrophic 'spiral' deflation" (hat tip to akrowne) does pose a possibility which JoeSixpack expresses: "I am more concerned than ever that the debt deflation and demand destruction might outpace the attempts to keep the system going..." This is IMHO a valid question. To the extent that our economy involves a pyschological component, no one knows the extent that this present unwinding may bring to bear upon our "expectations" despite all the efforts to "manage" them while also not allowing the pyramid of unwinding debt to get out of control.

I think here is the bone that strikes at the heart of this contretemp with Mish and the deflasionistas camp. As someone who has played a certain amount of my chips in PM (awhile ago due to economic turmoil concerns) it would seem to follow that I think iTulip is going to prove right. But quite honestly I don't believe any of us can know for certain what comes our way. Sometimes I think my wife said it best: "All my facts are based on opinion." Well, at least when it comes to predicting the future.

I also think donalds raises an extremely relevant issue whereby iTulip's thesis of KaPoom (and the potential ensuing alt. energy/infrastructure boom) does entail "the sphere of political" decisions, policies and all that this involves. As someone who is involved in a community effort to see our town use town owned land for wind power installations I am well aware of this political process, about which I do have more hope for local success than that which is practiced in D.C.

This communal effort along with many ongoing individual and private enterprise installation efforts may well provide the lift-off base for the Poom phase, but I am also mindful of unforeseen exogenous events (geo-politically, economically, and thus too psychologically, to go along with climatological and/or ecological ones, and even peak oil/energy ones), that could delay, if not derail entirely, this future envisioned economic boom.

I can hope our better angels or sheer luck in conjunction with sufficent profitability may prove correct. Still there is no denying we do live in a time that is fraught with more potential tipping points of whose irreversibility we can't know ahead of time where a crossing occurs and suddenly find ourselves no longer in control of all that we think we can control.

All I can do is wait and see how it all plays out while listening in (and chiming in like now) on interesting discussions as happens here. Thanks and Ciao!Leave a comment:

-

Re: Boom in the Doom

What I am struggling with is the apparent disconnect in dollar de(valuation) in the domestic US economy and in global markets.

The trade weighted dollar has declined significantly over the last few years as we all know. This shows up recently (as EJ and Fred point out) in high commodity valuations (there is a supply demand driver also, but since 2004 I think, the dollar story has been more important).

However, the higher commodity prices have not fed into inflation -- yet, but is poised to do so. Yes, I know the widely held belief that the government is faking the numbers, but I don't think that purchasing power loss due to general price inflation is at the same level as that due to trade weighted dollar decline. Said in another way, commodity price inflation appears to be higher than general price inflation.

So if one is talking about inflation or deflation, which of the two "dollars" is the right measuring stick? Or is it different depending on what is being measured?

Or am I completely off-base here?Leave a comment:

-

Guest repliedRe: Boom in the Doom

Guest repliedRe: Boom in the Doom

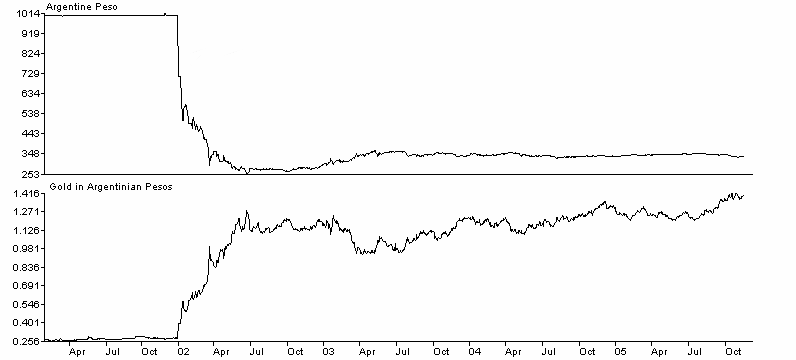

Don't all local 'inflations' have a severely weakening currency as central component? Couldn't this always be percieved from outside that currency zone as 'deflation' or 'cheapening' of assets or goods & service prices?

Mish lavishes attention upon 'deflation of assets', which is in fact readily observable from outside an affected weakening currency zone. Concurrent depreciation of an asset might also be very observable even within that currency zone. But does Mish make any mention of the corollary - that this environment's prime symptom, a sharply weakening currency - without gold backing, seems most often to coincide with generally rising net costs for people trapped within that currency?

Maybe an Argentine would have found it whimsical, if anyone addressed them with a comment about their 'asset deflation', if all they noted meantime was a soaring cost of living? What can we recognize meantime here in the US that is strikingly similar? A weakening dollar perhaps? Maybe a rising cost of living? Are these fantastic notions, or do they appear to be readily observable?

According to Mish everyone outside the US dollar zone might more readily observe asset deflation going on over here? Yes, OK. That's perhaps even understated, as the US dollar is global reserve currency, and it's rate of descent is disguised by the fact other currencies are drifting downwards with it. So the full extent of this USD event is not even readily apparent.

But am I to understand the plunging US dollar, (even if it's a milder version of Argentina's currency implosion), has departed from the above standard corollary effects, and is now not conducive to prices rising inside the dollar zone?

It seems the great majority of sharply or chaotically weakening currencies in history caused rising prices within their currency zone (denominator of prices shrinking) - but in our case, the US dollar which is quite obviously devaluing vs. other currencies, is not supposed to exert an upward pressure upon the cost of goods here?

This is a startlingly novel idea, which must be why I am finding it so difficult to grasp.Last edited by Contemptuous; February 06, 2008, 09:03 PM.Leave a comment:

-

Re: Boom in the Doom

they did. iirc what finally triggered the revaluation was accelerating capital flight.Originally posted by metalman View Post

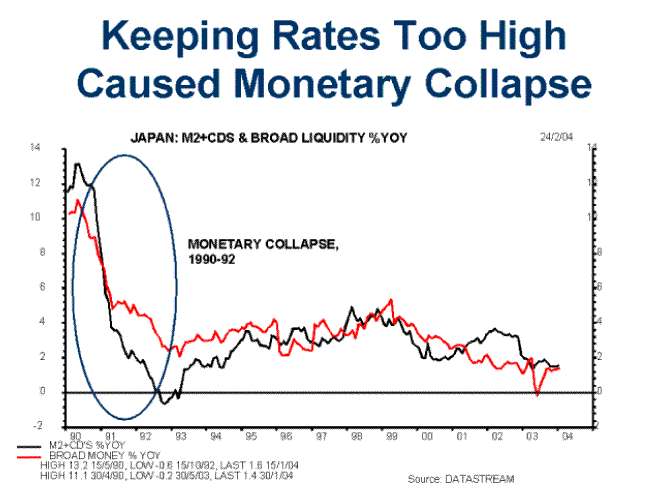

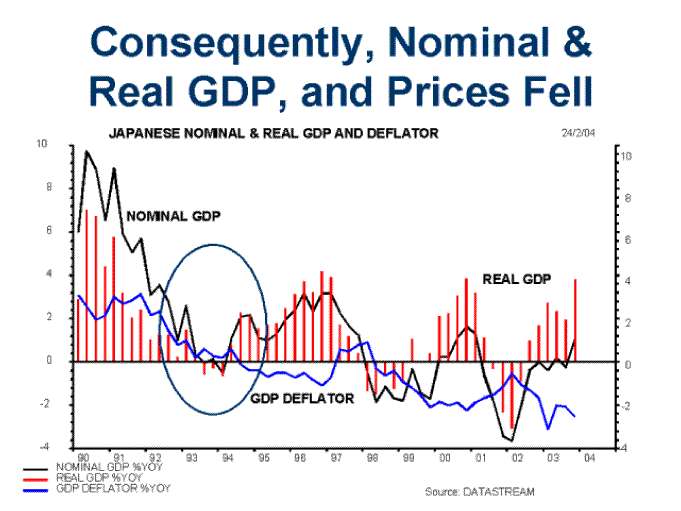

re "inflation" and "deflation," i brought up the argentine example to illustrate the lack of clarity we have most of the time when using those words. argentina had a severe inflationary depression viewed in local currency terms, and a severe deflationary depression viewed in global currency terms - i.e. the dollar or gold.

i think we should stop using these words except when specifying the currency in which the term is to be interpreted. or just stop using them altogether. reminds me of alfred kahn who, warned not to use the word "depression," said the country was heading for the worst banana in 45 years if it didn't get inflation [there's that pesky word again] under control.Leave a comment:

-

Re: Boom in the Doom

And EJ replies:

"Anyone that thinks the FED has any credibility needs to read this missive about FED Bubble Talk from 1999."Originally posted by FREDEtc.

That is an accurate representation of your position until recently when you stopped using it and started to refer to a decline in the monetary base as deflation. But prices are the only meaningful result of inflation and deflation. Not talking about inflation and deflation in the context of prices is like talking about obesity without talking about weight but only caloric input and exercise.Point #2

“Sometimes deflation is falling prices.”

No that is a misrepresentation of my position.

The discussion goes: the problem is obesity, the cause is excess caloric input and lack of exercise. Same deal with inflation: the problem is high prices, the cause is excessive money creation. If you could eat all you wanted and not exercise and not get fat, who'd care about diets and gyms? If not for rising prices which are the result of excessive money creation, who'd care about the money supply and the Fed? The answer is the same in both cases: no one.

You've been expecting prices to go down for years, but they keep going up. Rather than admit your model is wrong and go back and fix it, as we had to years ago, you'd rather pretend that prices are persistently rising because prices are not related the money supply; if facts don't conform to model, the model can't be wrong, it's the facts that are wrong, not the model. This approach will not serve you well in the long term. Why not say, "Well, prices sure are rising everywhere. That's not what our model anticipated. What we didn't build into our model was the impact of dollar depreciation because not in our wildest dreams when we developed our model did we expect that the Fed and Treasury would allow the dollar to fall more than 30% against major currencies." Then move on, try to determine whether the trend will continue or not.I expect prices to go down but I have repeated stated and repeat now that falling prices are not proof of deflation nor are rising prices proof of inflation. I often talk about prices but never as proof of either inflation or deflation. Nonetheless I am on official record of saying prices will likely fall on all kinds of goods and services. It simply is not a requirement they do so.

The phrase "Gold is money" is good ideology but has little practical meaning to investors. I recall hearing the "Gold is money" rallying cry in 1980, 1981, 1982, and on through 2001 during which time it meant "I'm a stubborn gold bug getting my ass handed to me for 20 years." It will have that meaning again some day in the future after the global monetary system gets it's act together again, whenever that is. Then all the gold owner will have left is a slogan, but no money.Point #3

I believe gold is money.

You counter that I need to be consistent.

I am consistent.

I consistently say gold is money.

Obviously you do not believe gold is money.

Once again you are imposing a definition of money on me.

The inconsistency is once again, you using definitions I do not agree with.

If the dollar is deflating against gold, gold prices are rising in dollar terms. If gold is deflating against the dollar, then gold prices are falling in dollar terms. In the first case the purchasing power of gold is rising, in the second of cash dollars. It's either one way or the other and cannot be both at once. It can be one THEN the other, and that's Ka-Poom Theory. At some point it will be time to trade out of gold and into assets that appreciate against dollars.Point #4

You claim “Deflation is not bullish for gold. In a deflation, no one has any money.”

My reply is “Gold is money. In deflation, those with gold will have money by definition.”

The gold will not disappear will it?

The Austrian school, as a lot of classical economists (my personal favorite is Joseph Schumpeter due to his focus on the importance of entrepreneurs in the economy) have a lot to offer, and I agree that a lot of modern economists have lost sight of basic principles of the classicists, such as the relationship between credit and innovation. But there was a lot they did not understand about economics, just as there is much that was not understood then about physics and human psychology.Point #5

There are numerous Austrian economists that agree with my definitions. If you choose to have a different viewpoint then I cannot change that. My viewpoint at least explains why gold is soaring and treasury yields are dropping.

I know you're no fan of Keynes. Have you read him? Keynes' contribution is in seeing an economy as a business that governments can influence but not control. The free market utopians think that's awful, that the economy should not be influenced by government at all. What we have learned over the past 30 years is that this in practice means ceding influence over the economy to finance, culminating in serial bubbles in asset prices and an absurd concentration of wealth. The results, I hope you will agree, have been less than delux. Leave any business to run itself and shortly the thugs and bullies take over.

Positive inflation, to be sure. But not a weak dollar and positive inflation. You really need to plug currency depreciation into your model.Point #6

Pull up a long term chart of gold.

Gold fell from 800 to 250 with positive inflation the entire time.

Gold is a very poor inflation hedge by that measure.

However, gold as a currency (money) handles the situation nicely. In periods of monetary disinflation, money does poorly compared to assets.

Less relevant model: demand is collapsing, economy in recession, money supply falling, currency appreciating.

More relevant model: demand is collapsing, economy in recession, money supply exploding, currency depreciating.

I mean what I said: thousands if not millions are better off for your diligent coverage of the fraud and greed, and I'm sure you get many letters of thanks from readers. We do, and it's very gratifying.Thank you for the otherwise favorable comments. I appreciate them. I was hoping this debate would not get acrimonious. I think it has been kept mostly within bounds. I too think you have done your readers a great service. You have made some extremely good calls.

The measures of inflation have changed, not the meaning of the term. The CPI was politicized under the Nixon administration.However, your rebuttals against deflation, even your current post, continue to debate without agreement as to definitions. If you look it up, the meaning of inflation has changed over time. I believe this is on purpose. It is of the central bank’s interest to not have people understand what inflation is. This give bankers the ability to inflate until it all blows up . And it blows up when no more debt can be forced into the system. That is, at least in my opinion, a very favorable environment for gold. It is also consistent with my definitions. From 1980 to 2000 you simply cannot make the same claim. Gold was a horrid inflation hedge.

To say that gold is rising because of inflation conveniently overlooks 20 year periods where there was inflation by either your definition or mine, and gold fell like a rock. No matter how hard you try, your gold responds to inflation theory does not hold up for considerable periods of time, decades in fact.

Gold is a currency depreciation hedge, with inflation a secondary effect of currency depreciation.

Make you a deal. Let me post to your site and you are welcome to post to mine. Fair enough?Since I cannot reply on iTulip, I would appreciate it if you would post this for me.

You are welcome to have the final word on this discussion, if you wish. I won't reply.I am not inclined to do another blog on it, we have both had our say.

Thanks

Mish

Eric

Last edited by FRED; February 06, 2008, 06:35 PM.Leave a comment:

-

Re: Boom in the Doom

i wonder... why didn't the argentines buy shitloads of gold to protect their wealth? i figure... the rich could hedge with dollar assets and the poor didn't have any money. hey, sounds familiar, except now it's hedge with non-dollar assets and gold for the rich.Leave a comment:

Leave a comment: