Originally posted by DSpencer

View Post

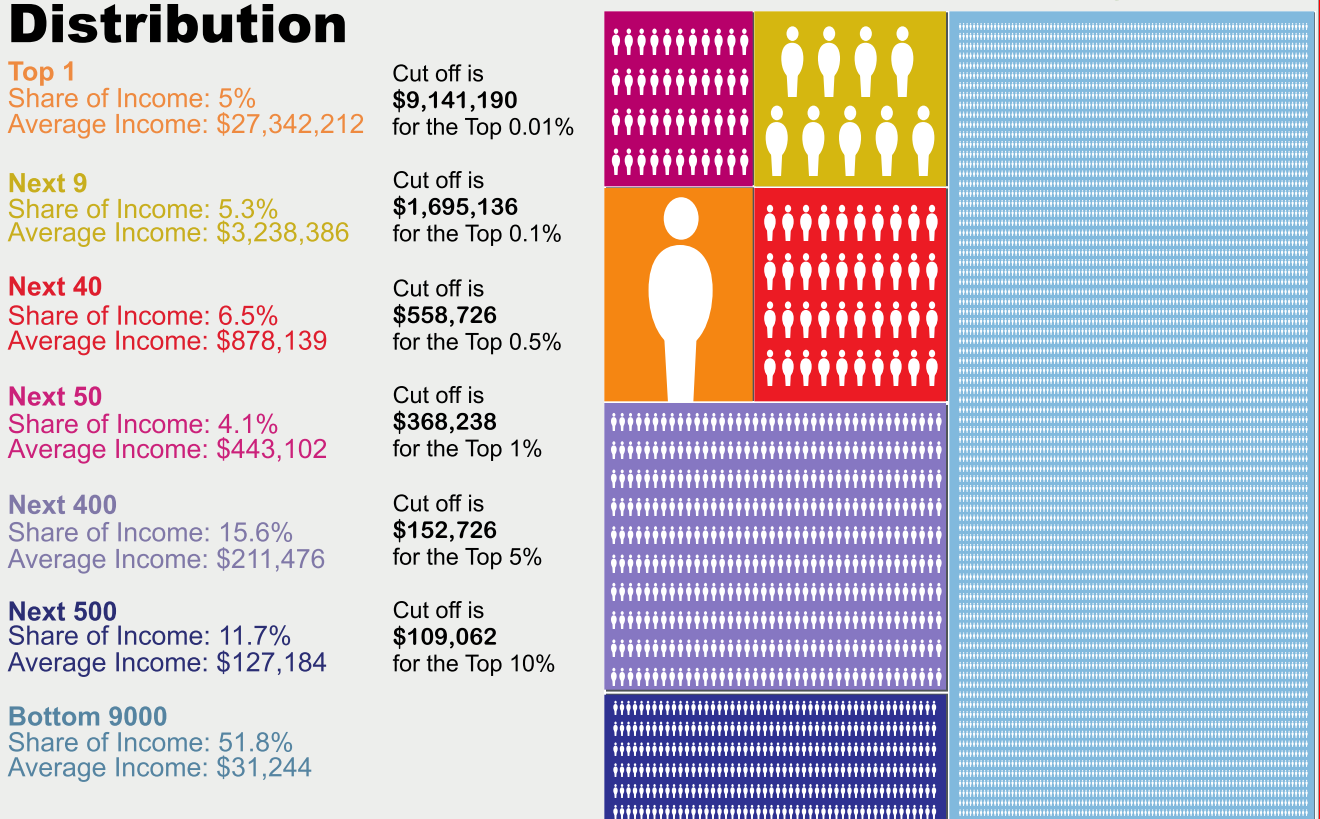

Top 1% = $368,238 (20.9% of income)

Top 0.5% = $558,726 (16.8% of income)

Top 0.1% = $1,695,136 (10.3% of income)

Top 0.01% = $9,141,190 (5% of income)>

click for larger chart

Does this matter at all to the conversation on inequality?

It sure seems we are quick to put blame on the weakest and least powerful among us. Why, I wonder?

Leave a comment: