Originally posted by jk

View Post

-

Re: A "Flood" of new oil : Be Careful What You Wish For

Is it worth including in that "How to best play temporarily cheap energy?" -

Re: A "Flood" of new oil : Be Careful What You Wish For

Think it might be a class thing? I'm starting to get suspicious.Originally posted by Lasher View Post

Considering this, it's hard not to be . . .

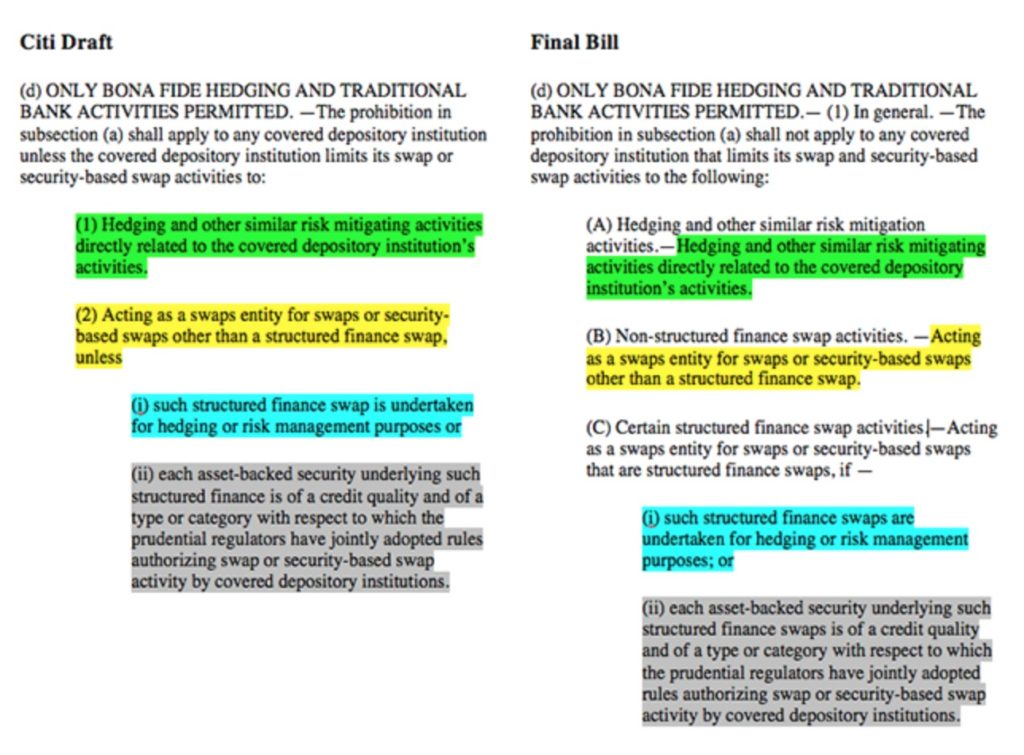

Courtesy of the Cronybus(sic) last minute passage, government was provided a quid-pro-quo $1.1 trillion spending allowance with Wall Street's blessing in exchange for assuring banks that taxpayers would be on the hook for yet another bailout, as a result of the swaps push-out provision, after incorporating explicit Citigroup language that allows financial institutions to trade certain financial derivatives from subsidiaries that are insured by the Federal Deposit Insurance Corp, explicitly putting taxpayers on the hook for losses caused by these contracts. Recall:We say explicitly, of course, because taxpayers have always been on the hook implicitly for the next Wall Street meltdown.

Five years after the Wall Street coup of 2008, it appears the U.S. House of Representatives is as bought and paid for as ever. We heard about the Citigroup crafted legislation currently being pushed through Congress back in May when Mother Jones reported on it. Fortunately, they included the following image in their article:

Unsurprisingly, the main backer of the bill is notorious Wall Street lackey Jim Himes (D-Conn.), a former Goldman Sachs employee who has discovered lobbyist payoffs can be just as lucrative as a career in financial services.

Why?

Exhibit A: US banks are the proud owners of $303 trillion in derivatives (and spare us the whole "but.. but... net exposure" cluelessness - read here why that is absolutely irrelevant when even one counterpaty fails):

Exhibit B: Here are the four banks that are in complete control of the US "republic."

At least we now know with certainty that to a clear majority in Congress - one consisting of republicans and democrats - the future viability of Wall Street is far more important than the well-being of their constituents. Which also, implicitly, was made clear when Hank Paulson was waving a three-page "blank check" term sheet, and when Congress voted through the biggest bailout of banks in US history back in 2008.Leave a comment:

-

Re: A "Flood" of new oil : Be Careful What You Wish For

This just makes me crazy. When AIG was going under, they had to pay out bonuses because the contracts were sacred. But now we have pensioners getting what they worked for, and suddenly the contract doesn't matter?Leave a comment:

-

Re: A "Flood" of new oil : Be Careful What You Wish For

Are we seeing the international implications from this practice?Originally posted by vinoveri View Post

and speaking of moral hazard - now such a quaint notion - from Jesse's Cafe Americain:

When the Operation of the Machine Becomes So Odious

"This is the contempt in which they hold the majority of American people and the political process: the common people are easily led fools, and everyone else who is smart enough to know better has their price. And they would beggar every middle class voter in the US before they will voluntarily give up one dime of their ill-gotten gains."

Simon Johnson

Congress is crafting a bipartisan deal to allow retiree benefits to be cut.

"A measure that would for the first time allow the benefits of current retirees to be severely cut is set to be attached to a massive spending bill, part of an effort to save some of the nation�s most distressed pension plans.

The rule would alter 40 years of federal law and could affect millions of workers, many of them part of a shrinking corps of middle-income employees in businesses such as trucking, construction and supermarkets."

As you may recall, Congress responded to business lobbying by allowing their pension plans to make outrageously optimistic assumptions about future returns, so the corporations could divert more of their money from pension contributions to short term profits.

Now that corporate profits are at record levels, someone has to take up the slack and that must be the elderly. Let's just rewrite the contracts after the fact, and take the money from them.

In a conversation today some were tut-tutting this decision. But after all, someone has to tighten their belts in hard times. It certainly can't be the privileged class, so it may as well be the pensioners.

I hope people are so sanguine when the Banks come to seize their assets to make up their derivatives losses, which emboldened they will almost certainly do. First they come for the pensions, and then they come for the savings deposits and IRAs. It is a sign of the times.

Speaking of a sign of the times, the Manhattan based 2nd US District Court of Appeals knocked my socks off today, with a ruling that basically overturns 80 years of securities principles, and probably does more to erode the 14th amendment than Citizens United.

2nd US District Court of Appeals Issues the Equivalent of the Dred Scott Decision for US Securities Markets

Here is the money shot in the decision that overturned the insider trading convictions of the infamous ring involving SAC and what looked like an organized conspiracy to violate securities laws.

"Although the government might like the law to be different, nothing in the law requires a symmetry of information in the nation's securities markets."

Barrington Parker, 2nd U.S. Circuit of Appeals Judge

And I will wager that if you have not seen this here and a few other places in the blogosphere, you would not even understand what the heck was going on. The mainstream news stories made it seem like the conviction was overturned on insufficient evidence.

Well technically it was. Especially if you maintain the perspective of a servile tool of the corporate media. To paraphrase Mario Savio, would you ever imagine a manager in a firm making a statement that is in contradiction to his board of directors?

In its attempt to give a get out of jail card to some of the particularly well-connected, the appeals court has set a precedent that is noxious and repugnant to the Constitution, particularly the 14th amendment. Its willingness to torture the law should make us wary of what other things that the crony capitalists have in mind with regard to overturning bank reform and confiscating assets.

If this stands, there is no excuse for any foreign investor to complain when they are robbed blind by the US markets. At least those in the US can make the case that getting all their money away from the US banks is an onerous task. The character of this government is being writ large for all to see.

Other than this, I just don't have the words. The stench coming out of New York and Washington is getting so bad I can't breathe, whether it is from being water-boarded, or slammed to the ground and choked to death for a cigarette, or being robbed blind by white collar criminals who have friends in high places. Don't bother to do anything. Sit back and relax. They will come for you and yours too, sooner or later.

To paraphrase Martin Luther King, never forget, everything they do will be 'legal.'Leave a comment:

-

Re: A "Flood" of new oil : Be Careful What You Wish For

Originally posted by don View Post

If the fed wanted to it could start buying high yield bonds - and of course it would if they have been securitized and their collapse in price was a threat to the banking system

They can monetize student loan debt, car loan debt, anything they please - let's see, the Treasury lends ~$50k over 4 yrs to 1 million college students; the Fed buys the notes from the Treasury, and "absorbs" any of the losses from default. In fact, the Fed could simply write of the loans and forgive all the debt; I suspect that as this progresses, limited piecemeal debt jubilees will occur - after all their is no private assetholder/creditor who will be the less for the write offs (oh, well except for those who actually earned their dollars through hard work), but we are way past moral hazardLeave a comment:

-

Re: A "Flood" of new oil..........

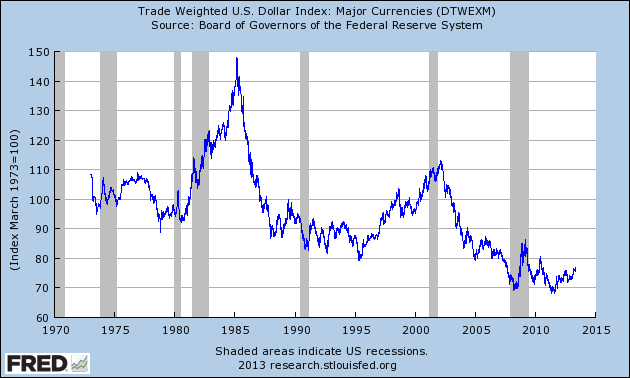

In the chart above, the sharp fall in the dollar in 1985 is due to the Plaza Accord and not the decline in crude oil prices.Originally posted by meofio View PostLeave a comment:

-

Re: A "Flood" of new oil..........

here's an article on 1980s oil glut

http://en.wikipedia.org/wiki/1980s_oil_glut

US dollar crashed along with oil from 1986-2000

US stock market suffered a crash in 1987Leave a comment:

-

Re: A "Flood" of new oil..........

And look what happened in 1985

"November - December 1985: Opec decides to increase market share; price war begins"Leave a comment:

-

Re: A "Flood" of new oil : Be Careful What You Wish For

$550 Billion Energy Junk Bond Bubble Busts; "Whac-A-Mole" Distortions in Multiple Markets

The energy junk bond bubble has finally popped. Falling crude prices were the catalyst. Junk bonds of Energy XXI Ltd. plunged to 64 cents on the dollar from 106.3 cents since September. They now yield over 27%. Energy XXI Ltd. raised over $2 billion.

Energy production is extremely capital intense, and often accompanied by negative free cash flow.

Recently I have been getting numerous cold-calls, nearly all of them energy related. These companies need money, and snake-oil salesmen attempt to get it for them.

Energy investment added to GDP since 2010, with $550 billion in bond and loan offerings. Energy will now have a negative impact on GDP as funding dries up. And if oil prices do not head back up, expect outright defaults, and lots of them. This is what happens when bubbles burst.

Who Caused the Energy Bubble?

The Fed is responsible of course, by holding interest rates at record lows, stimulating all sorts of speculative investments. But it's exceptionally rare to see anyone in mainstream media point the finger in the right direction. Today I have a notable and welcome exception.

Kudos to Bloomberg writers Christine Idzelis and Craig Torres for placing blame precisely where it belongs in their report Fed Bubble Bursts in $550 Billion of Energy Debt.

Since early 2010, energy producers have raised $550 billion of new bonds and loans as the Federal Reserve held borrowing costs near zero, according to Deutsche Bank AG. With oil prices plunging, investors are questioning the ability of some issuers to meet their debt obligations. Research firm CreditSights Inc. predicts the default rate for energy junk bonds will double to eight percent next year.

�Anything that becomes a mania -- it ends badly,� said Tim Gramatovich, who helps manage more than $800 million as chief investment officer of Santa Barbara, California-based Peritus Asset Management. �And this is a mania.�

The Fed�s decision to keep benchmark interest rates at record lows for six years has encouraged investors to funnel cash into speculative-grade securities to generate returns, raising concern that risks were being overlooked. A report from Moody�s Investors Service this week found that investor protections in corporate debt are at an all-time low, while average yields on junk bonds were recently lower than what investment-grade companies were paying before the credit crisis.

Yields Surge

Yields on junk-rated energy bonds climbed to a more-than-five-year high of 9.5 percent this week from 5.7 percent in June, according to Bank of America Merrill Lynch index data. At least three energy-related borrowers, including C&J Energy Services Inc. (CJES), postponed financings this month as sentiment soured.

Stimulus Effect

The Fed�s three rounds of bond buying were a gift to small companies in the capital-intensive energy industry that needed cheap borrowing costs to thrive, according to Chris Lafakis, a senior economist at Moody�s Analytics in West Chester, Pennsylvania.

Quantitative easing �has been one of the keys to the fast, breakneck pace of the growth in U.S. oil production which requires abundant capital,� Lafakis said.

One of those to take advantage was Energy XXI Ltd. (EXXI), an oil and gas explorer, which has raised more than $2 billion in the bond market in the past four years.

The Houston-based company�s $750 million of 9.25 percent notes, issued in December 2010, have tumbled to 64 cents on the dollar from 106.3 cents in September, according to Trace, the bond-price reporting system of the Financial Industry Regulatory Authority. They yield 27.7 percent.

Energy XXI got its lenders in August to waive a potential violation of its credit agreement because its debt had risen relative to its earnings, according to a regulatory filing. In September, lenders agreed to increase the amount of leverage allowed.

The debt rout is one of the latest examples of a boom and bust in U.S. markets as unprecedented Fed stimulus fuels a hunt for yield. The fallout has been limited so far, yet the longer the Fed holds its benchmark lending rate near zero, the greater the risk of more consequential bubbles, according to former Fed governor Jeremy Stein.

�There are distortions in multiple markets,� said Lawrence Goodman, president of the Center for Financial Stability, a monetary research group in New York. �It is like a Whac-A-Mole game: You don�t know where it is going to pop up next.�

"Whac-A-Mole" Distortions in Multiple Markets

Lawrence Goodman along with writers Idzelis and Torres win the blue ribbon for accurate assessment of the month.

Yet, "Whac-A-Mole" has barely started. I suspect all junk bonds will come into question the moment the Fed hikes or the economy sours, whichever comes first.

Moreover, it's not just the US in play. I foresee global "Whac-A-Mole" in various currencies, equities, junk bonds, bank bonds and even sovereign bonds (especially European bonds).

For example, please consider the dismal state or European banks as noted in Charts Show 28 Seriously Troubled Mega-Banks: 24 of them in Europe.

http://globaleconomicanalysis.blogsp...JPkG3sKrJKT.99Leave a comment:

-

Re: A "Flood" of new oil..........

Is gold and oil price decoupling again? Last time this occurred was 1986-2000Leave a comment:

-

Re: A "Flood" of new oil : Be Careful What You Wish For

The energy sector now represents 15% of the U.S. junk bond market, a percentage that has doubled over the last few years. While some of that borrowing has gone to invest in refineries, which benefit from lower prices, and pipelines, which are close to neutral, any that has gone toward the production of oil or gas is likely to be very difficult to service.

this ignores the possibility that formerly investment grade securities were downgraded to junk because of the drop in energy prices. if so, the service required will be less punitive, since the financings would have been done at lower rates.

about the rest of the hutchinson piece: he assumes that $60-70 will remain the oil price indefinitely. i'm not convinced this lower price will persist very long.

i would love to hear grg55's take on that issue.

Leave a comment:

-

A "Flood" of new oil : Be Careful What You Wish For

December 8, 2014 posted by Martin Hutchinson

The OPEC meeting over Thanksgiving week failed to result in any oil production cuts, immediately sending prices down by $5 per barrel. Its action made it clear that, for the first time since 1972, there is no cartel able to control the oil market. At first sight that looks like excellent news for America's consumers, just in time for their Christmas shopping binge. However on closer consideration, it locks the U.S. into being the world's high-cost producer of a major commodity. The bonanza from fracking may be about to go into reverse.

The fall in the oil price is caused by a fundamental shift in the market. Price is now being driven by supply, whereas previously it was driven by demand. This has happened before: the oil price fell from $27 a barrel at the beginning of 1986 to $10 at the year's end, where it remained until around 2000, with only a short blip during the Gulf War. The transition from a market driven by demand to one driven by supply typically causes a large price shift because of the long lead time of oil investment and stickiness in the market. In 2011, when oil prices soared above $100 a barrel, there was considerable speculation that they would soon reach $200. Since then, the U.S. fracking revolution has both brought new supply on stream, making the U.S. a bigger producer than Saudi Arabia, and increased the potential resources for future production worldwide. At $100 a barrel, Canadian (and potentially Venezuelan) tar sands and shale deposits in Poland, Argentina and many other countries were potentially profitable. Investment would have poured into those sectors.

Just as in 1986, after several years of high prices, new sources of oil supply caused the price to collapse. In 2014, after several years of high prices, supply and potential supply caught up with demand, and the price dropped back to the level at which marginal supplies became unprofitable.

In the late 80s and the 90s, marginal supplies were profitable at $10 a barrel. Today that figure is more like $70. There is a certain amount of further efficiencies that can be gained from experience, so the initial estimates of $80 a barrel at which fracking and oil shale made sense were probably a little high. But it seems very unlikely that substantial new supplies will continue to be developed below $70. The oil price may spike downward for a while, but the $65-$70 level looks like a long-term floor.

Keynesian economists are overjoyed by the oil price drop. Capital Economics, a well-known London-based economic forecaster, has drawn substantial notice worldwide with its forecast that each $10 fall in the oil price causes a surge in global Gross Domestic Product (GDP) of about 0.5%. Capital Economics is slightly less ebullient about the prospects for the U.S. because of its substantial oil production. But as quoted by the American Enterprise Institute�s (AEI) James Pethokoukis, it believes that each $10 drop in the price of oil causes an increase in real U.S. GDP of $38 billion, or about 0.2%, of GDP.

Capital Economics' experts rely on the well-worn Keynesian argument that a fall in oil prices transfers wealth from oil producers, who tend to save it�think Saudi Arabia or Norway�to consumers who, at least in the U.S., spend about 96-98 cents of every dollar they can get their mitts on. That's why traditionally, a fall in oil prices has been thought to be very good for the U.S. It produced only about 60% of the oil it consumed, but had avid consumers ready to spend, spend, spend and push up economic activity if only oil prices fell from $4 to $2 a gallon.

This analysis is now wrong in a number of ways. First, it uses the mistaken Keynesian focus on consumption and ignores production. Consumers don't produce anything; their trips to the mall only increase the country's already excessive debt level. Today, when a high percentage of consumer goods, and an even higher percentage of "impulse buys," are produced internationally, consumer joie de vivre-fueled spending sprees do nothing for the productive side of the U.S. economy.

Second, it assumes that all oil producers are all like the traditional Saudi Arabia, which had nothing to spend the money on. Today's Saudi Arabia has a government spending budget of more than a third of GDP, only barely balanced and bloated by various expensive welfare programs intended to tamp down potential jihadist unrest. Thus the Saudi government's propensity to consume from its oil revenues is as high as that of any witless U.S. consumer. In any case, most of the revenue from unconventional oil production has associated production costs much closer to the current price level. And the great majority of the revenues are ploughed back into capital spending to search for and develop new, albeit mostly expensive, sources of oil.

Even on Keynesian assumptions, therefore, Capital Economics' analysis looks misguided. There is however a further reason why for the U.S. in particular its analysis look too optimistic. At the margin, after the fracking revolution and its investment in deep-sea drilling, the U.S and its neighbor Canada are the world's high cost oil producers.

At $80 or above, perhaps even at $70, this doesn't matter much. Between $80 and $100 the Keynesian analysis of U.S. GDP's oil dependency may have some validity (even if internationally, there appears to be little saved from oil revenues at prices below $100). Price increases above $80 indeed depress consumer spending, while they don't increase U.S. oil production much, as the country's oil producers are already investing to expand output. Above $100 a barrel, there is no question that further rises in price depress U.S. consumption while adding to surpluses in some of the oil producers, thus depressing global GDP overall. Thus the increase to $147 a barrel in 2008 was one of the major causes of the 2008-09 recession, albeit a cause much less celebrated than the housing and financial crashes.

However, once the oil price falls below $70, the economic ill-effects for the U.S. of being the world's high-cost oil producer kick in. Investment in the oil sector becomes hopelessly unprofitable, so a wave of bankruptcies must result. In the Austrian economic analysis, the U.S. and Canadian investment in fracking, tar sands and deep-sea drilling becomes "malinvestment" that must be liquidated. You can see the effect of this in the market's reaction late last month to the abolition of Seadrill's (NYSE:SDRL) dividend. The stock dropped 23% in one afternoon and has fallen a further 10% since. The energy sector now represents 15% of the U.S. junk bond market, a percentage that has doubled over the last few years. While some of that borrowing has gone to invest in refineries, which benefit from lower prices, and pipelines, which are close to neutral, any that has gone toward the production of oil or gas is likely to be very difficult to service.

There will be an important second-order effect on the U.S. economy from the energy price downturn. In the last few years, energy-intensive manufacturers have been encouraged to invest in the U.S. because of its relative cost advantage in energy. That has allowed manufacturers whose processes are intensive in energy and not especially in labor to make up for the U.S. labor-cost disadvantage, thus creating jobs that are relatively invulnerable to outsourcing to the Third World.

However, just as cheap money has reduced or even eliminated the U.S. advantage in the cost of capital, and encouraged the migration of U.S. jobs to emerging markets, so will the reduction or even elimination of the country�s energy-cost advantage bring a second wave of outsourcing to other countries of both capital investment and generally well-paid jobs. This is an effect entirely ignored by the simple first-order Keynesian models. But if oil prices remain below $70 a barrel there will be further unpleasant surprises for the U.S. workforce, which has already suffered so badly from U.S. economic mismanagement.

Energy-sector bankruptcies�many of which will result in production capacity being taken out of the market�and the accompanying outsourcing of energy-intensive manufacturing capacity are likely to cause damage that far outweighs any benefit from increased consumption. Capital destruction through bankruptcy reduces the wealth of society, which reduces the amount of capital available for each worker, That in turn reduces the long-term living standards of the workers themselves (and indeed their ability to consume). Additional consumption, much of which will be spent on imports, brings no benefit that is even close to the same level of importance.

The adverse effect of lower oil prices will be worsened by regulation, which by attempting to steer the U.S. economy toward energy sources that are now impossibly more expensive, has put itself on the path to vast malinvestment and waste. Ironically, if energy prices stay low, the Keystone XL pipeline may prove in the end to be an unattractive investment, as the Canadian oil that would be moved by it becomes uneconomic. However, to counter that spurious and random gain from the U.S regulatory morass, the billions of dollars of solar and wind farm investments that have been made will become spectacularly less economically justifiable in an era when oil and gas prices have unexpectedly dropped sharply.

The market and its Keynesian boosters have taken the fall in oil prices as yet another positive sign for the beleaguered U.S. economy. The cheerleaders are wrong.Leave a comment:

Leave a comment: