Tweet

Tweet

an industry still run amuck . . .

You will notice that most ads to purchase a car or a home always discuss financing with big bold letters but never dive into an adequate income analysis before you should even consider buying a European luxury car or a home in an expensive metro area. Income is the most important feature yet never discussed like a taboo topic. This might reveal a glaring reality about household incomes but also net worth. This isn’t something that is new. There are many households especially in California that funnel large portions of their household income into purchasing a home. Any person that has had the fun experience of driving on our freeways must come to the conclusion that every person living in California is able to afford a $30,000+ car even though most are financed. The artifacts of wealth simply do not highlight a decade of stagnant incomes and oh, by the way, a 20+ percent underemployment rate and state deficits for as far as the eye can see. This is a major reason why FHA insured loans are facing massive defaults. People think just because they qualify they can somehow afford an expensive home.

What is affordable after all?

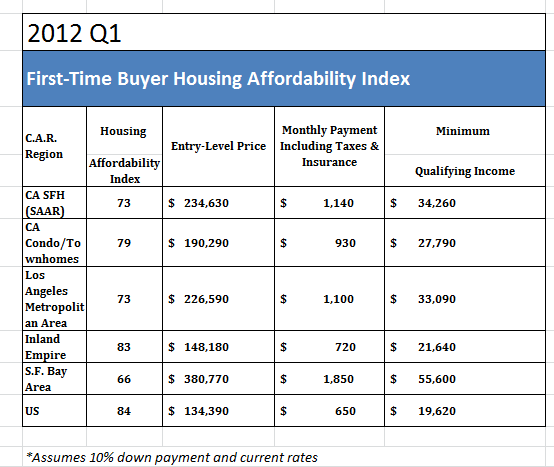

The California Association of Realtors has a first-time home buyer affordability chart on their website. The figures are interesting:

I find this chart amusing. First, what constitutes an entry level house in Los Angeles? At a price point of $226,590 I’m really curious to see some samples of this. Yet more importantly, take a look at the qualifying income. Do you really think a household making $33,000 can afford a $226,000 home? This is nearly 7 times the annual income of this household. Compare this to the US where half of households are making $50,000 or more and the median price home is roughly $180,000 (closer to ratio of 3.6). That looks more affordable.

This data isn’t surprising. Or look at the Bay Area. Can a household pulling in $55,000 a year really afford a $380,000 home? According to the above figures, yes they can. Let us not include the other big spending items in California such as cars, fuel, insurance, food, healthcare, and everything else in life.

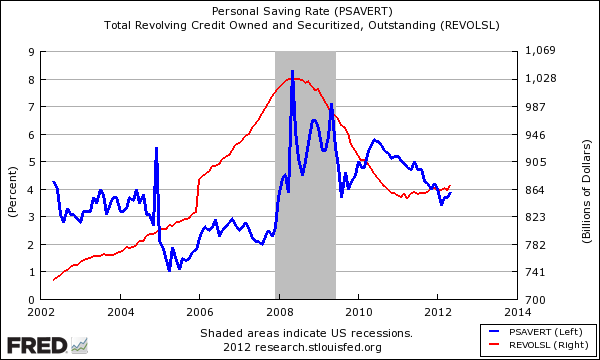

The concept of affordability is so out of whack. Part of this is that first, the US is a high consumption society. We have a tough time saving money as demonstrated by multiple sources of data:

At some point in the early 2000s we actually had a negative savings rate. Why save when you can go into debt? This is exactly what Americans did. California is even more extreme in that it is a hyper-consumption state. Billion dollar deficits for years to come yet somehow, going into massive debt just because interest rates are low seems to make sense for some. Those cities going bankrupt are not exactly a beacon of financial stability. The income stream has dried out just like the millions currently in foreclosure.

Spending to squeeze into a home

FHA insured loans continue to be the entry point for new buyers. 1 out of 3 homes purchased in California come from this low down payment option. Contrary to the above chart, the vast majority are diving in with a typical 4 percent down payment (slightly above the minimum 3.5 percent). Another 1 out of 3 buyers are buying homes with all cash or for investment purposes. So you have those barely able to squeeze in and those buying for investment purposes as the bulk of your market.

We discussed this before, but FHA is a big player in California and default rates are surging:

Source: CNN Money

Why is this not surprising? Of those that own homes, over 50 percent spend more than 30 percent of their gross income on housing costs. In fact, more than 40 percent spend more than 35 percent! The Census caps out at 35 percent but you have people spending 40, 50, and even 60 percent of their gross income just to get into a home in California. Is it any wonder why California has such a massive amount of underwater mortgages?

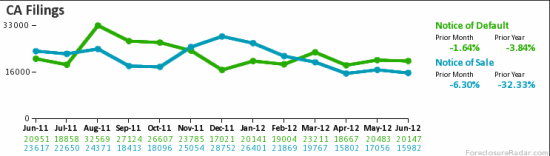

Just because you qualify by these odd measures of affordability does not mean you can actually afford a home. Foreclosure filings are still robust:

Half of homes sold in California last month were part of the distressed pipeline (foreclosure re-sales or short sales). Those homes are attached to families that are taking a loss one way or another. Yet the focus is always on jamming people in and the lack of income analysis in the media is astounding but not at all surprising. Like casinos that state they are for responsible gambling but offer major comps to players that lose the most. So for the time being the low interest rate and constrained inventory is pushing prices higher. Yet higher prices without stronger household incomes and a better economy is simply setting up a short-term push up. For California, this is very similar to the First-Time Home Buyer tax credit a couple of years ago.

It is startling how ill prepared many are for retirement and this mindset is one of those reasons. For many especially in California, some baby boomers look to have as their retirement plan Social Security while staying in a Prop 13 protected property. Yet with the spendthrift habits of decades will people be able to adjust? They really have no choice. What an odd state we live in where someone can live in a $700,000 (not purchased at that price) paid off house and collect $1,500 a month in Social Security as their only source of income. Then you wonder why our state has so many fiscal issues.

http://www.doctorhousingbubble.com/c...income-levels/

You will notice that most ads to purchase a car or a home always discuss financing with big bold letters but never dive into an adequate income analysis before you should even consider buying a European luxury car or a home in an expensive metro area. Income is the most important feature yet never discussed like a taboo topic. This might reveal a glaring reality about household incomes but also net worth. This isn’t something that is new. There are many households especially in California that funnel large portions of their household income into purchasing a home. Any person that has had the fun experience of driving on our freeways must come to the conclusion that every person living in California is able to afford a $30,000+ car even though most are financed. The artifacts of wealth simply do not highlight a decade of stagnant incomes and oh, by the way, a 20+ percent underemployment rate and state deficits for as far as the eye can see. This is a major reason why FHA insured loans are facing massive defaults. People think just because they qualify they can somehow afford an expensive home.

What is affordable after all?

The California Association of Realtors has a first-time home buyer affordability chart on their website. The figures are interesting:

I find this chart amusing. First, what constitutes an entry level house in Los Angeles? At a price point of $226,590 I’m really curious to see some samples of this. Yet more importantly, take a look at the qualifying income. Do you really think a household making $33,000 can afford a $226,000 home? This is nearly 7 times the annual income of this household. Compare this to the US where half of households are making $50,000 or more and the median price home is roughly $180,000 (closer to ratio of 3.6). That looks more affordable.

This data isn’t surprising. Or look at the Bay Area. Can a household pulling in $55,000 a year really afford a $380,000 home? According to the above figures, yes they can. Let us not include the other big spending items in California such as cars, fuel, insurance, food, healthcare, and everything else in life.

The concept of affordability is so out of whack. Part of this is that first, the US is a high consumption society. We have a tough time saving money as demonstrated by multiple sources of data:

At some point in the early 2000s we actually had a negative savings rate. Why save when you can go into debt? This is exactly what Americans did. California is even more extreme in that it is a hyper-consumption state. Billion dollar deficits for years to come yet somehow, going into massive debt just because interest rates are low seems to make sense for some. Those cities going bankrupt are not exactly a beacon of financial stability. The income stream has dried out just like the millions currently in foreclosure.

Spending to squeeze into a home

FHA insured loans continue to be the entry point for new buyers. 1 out of 3 homes purchased in California come from this low down payment option. Contrary to the above chart, the vast majority are diving in with a typical 4 percent down payment (slightly above the minimum 3.5 percent). Another 1 out of 3 buyers are buying homes with all cash or for investment purposes. So you have those barely able to squeeze in and those buying for investment purposes as the bulk of your market.

We discussed this before, but FHA is a big player in California and default rates are surging:

Source: CNN Money

Why is this not surprising? Of those that own homes, over 50 percent spend more than 30 percent of their gross income on housing costs. In fact, more than 40 percent spend more than 35 percent! The Census caps out at 35 percent but you have people spending 40, 50, and even 60 percent of their gross income just to get into a home in California. Is it any wonder why California has such a massive amount of underwater mortgages?

Just because you qualify by these odd measures of affordability does not mean you can actually afford a home. Foreclosure filings are still robust:

Half of homes sold in California last month were part of the distressed pipeline (foreclosure re-sales or short sales). Those homes are attached to families that are taking a loss one way or another. Yet the focus is always on jamming people in and the lack of income analysis in the media is astounding but not at all surprising. Like casinos that state they are for responsible gambling but offer major comps to players that lose the most. So for the time being the low interest rate and constrained inventory is pushing prices higher. Yet higher prices without stronger household incomes and a better economy is simply setting up a short-term push up. For California, this is very similar to the First-Time Home Buyer tax credit a couple of years ago.

It is startling how ill prepared many are for retirement and this mindset is one of those reasons. For many especially in California, some baby boomers look to have as their retirement plan Social Security while staying in a Prop 13 protected property. Yet with the spendthrift habits of decades will people be able to adjust? They really have no choice. What an odd state we live in where someone can live in a $700,000 (not purchased at that price) paid off house and collect $1,500 a month in Social Security as their only source of income. Then you wonder why our state has so many fiscal issues.

http://www.doctorhousingbubble.com/c...income-levels/

Comment