Tweet

Tweet

Consumer Sentiment Metric

Couple that with - Consumers Still Chopping Up The Credit Cards, As June Revolving Credit Falls Again

And you get

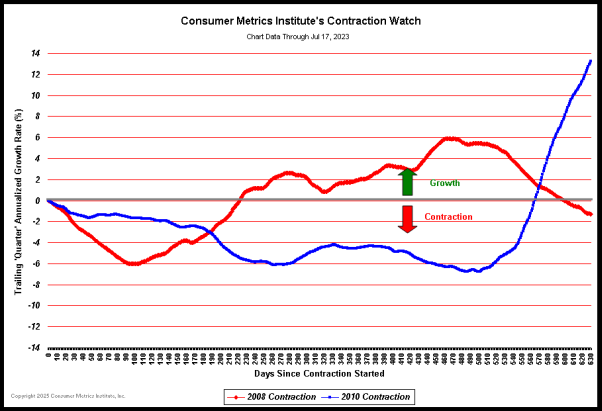

Also Consumer Metrics Institute's Contraction Watch

Couple that with - Consumers Still Chopping Up The Credit Cards, As June Revolving Credit Falls Again

The process of cutting up credit cards continues.

The Fed is out with June consumer credit data (correction: the post originally identified it as July data... there is one-month lag), and it shows that while total consumer credit fell just .7%, revolving consumer credit shrank 6.5% on an annualized basis.

On a sequential basis, the decline went from $831 billion to $826 billion.

The Fed is out with June consumer credit data (correction: the post originally identified it as July data... there is one-month lag), and it shows that while total consumer credit fell just .7%, revolving consumer credit shrank 6.5% on an annualized basis.

On a sequential basis, the decline went from $831 billion to $826 billion.

Also Consumer Metrics Institute's Contraction Watch

Comment