Tweet

Tweet

How can this possibly not end badly... very badly?

http://seekingalpha.com/article/2107...5-trillion-bet

From the article:

http://seekingalpha.com/article/2107...5-trillion-bet

From the article:

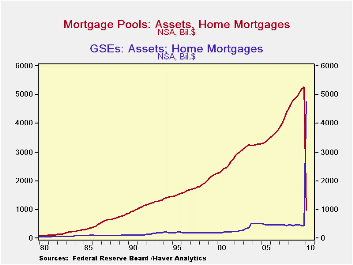

The FASB's new accounting rules 166 and 167 on the use of off-balance sheet accounting for securitized debt issues took effect at the beginning of 2010 for financial institutions with a calendar year fiscal year. From a data user's perspective, earlier this year, they were reflected in changes to commercial bank balance sheet data, and last week, with the release of the Q1 Flow-of-Funds data, we saw their impact more broadly on banks, GSEs and the special purpose vehicles (SPVs) these rulings were intended to reform.

It has been routine practice for issuers of securitized debt to "spin" the specific loans and the securities issues off the institutions' balance sheets to a subsidiary set up for the express purpose, an SPV. As FASB's notice explains, this SPV procedure is helpful for financing a narrowly defined project without putting an entire firm at risk.

However, the original intention of the SPVs was not to distort the institution's underlying risk profile over a protracted period, which had in fact been happening, as investors found to their dismay during the recent financial crisis. These new rules basically cause the securitized debt issuers to move assets and associated securities liabilities back to their balance sheets.

The chart (Editor's Note: see above ) shows the dramatic impact of the rule changes on the biggest item.

First, in the mortgage sector, 1-4 family mortgages that are held at "agency- and GSE-backed mortgage pools" plunged from $5.27 trillion at the end of 2009 to just $983 billion on March 31. By contrast, the direct mortgage holdings of the agencies themselves surged from $438 billion at year-end to $4.75 trillion on March 31."

It has been routine practice for issuers of securitized debt to "spin" the specific loans and the securities issues off the institutions' balance sheets to a subsidiary set up for the express purpose, an SPV. As FASB's notice explains, this SPV procedure is helpful for financing a narrowly defined project without putting an entire firm at risk.

However, the original intention of the SPVs was not to distort the institution's underlying risk profile over a protracted period, which had in fact been happening, as investors found to their dismay during the recent financial crisis. These new rules basically cause the securitized debt issuers to move assets and associated securities liabilities back to their balance sheets.

The chart (Editor's Note: see above ) shows the dramatic impact of the rule changes on the biggest item.

First, in the mortgage sector, 1-4 family mortgages that are held at "agency- and GSE-backed mortgage pools" plunged from $5.27 trillion at the end of 2009 to just $983 billion on March 31. By contrast, the direct mortgage holdings of the agencies themselves surged from $438 billion at year-end to $4.75 trillion on March 31."

My question: Does the government have a plan, or is this all ad hoc, extend and pretend and hope for the best?

Comment