Originally posted by bart

-

Re: Bernanke: Talks the Dove, Acts the Hawk

the down move in usdx looks like we're back to business as usual. dollar down, yen down, other currencies up, stocks up, gold up, oil up. -

Re: Bernanke: Talks the Dove, Acts the Hawk

EJ, Bob Prechter thinks the explosion in Sovereign Country Funds is a massive contrary bell ringing top signal..... i.e.. After a historical 27 year bull market the dumb money (governments) decide that stocks are the place to be instead of staying in safe Treasury instruments.Originally posted by EJ View Post

I'm not a Prechtarian but I think that is a very very interesting observation.Leave a comment:

-

Re: Bernanke: Talks the Dove, Acts the Hawk

that's interesting. i thought you were crediting the fed with more creativity and more power than heretofore, and thus thought they could moderate these processes.Originally posted by ej

also, i had conceived of poom as a re-run of the 70's, and in fact the 70's have been the model for many commentators who talk about inflation ahead. then gold had an irregular run with its spike, of course, but other real assets [like real estate] had extended moves over long periods of time. it's much more daunting to conceive of moves comparable to the recent movement in tbills.Leave a comment:

-

Re: Bernanke: Talks the Dove, Acts the Hawk

Originally posted by EJ View Post

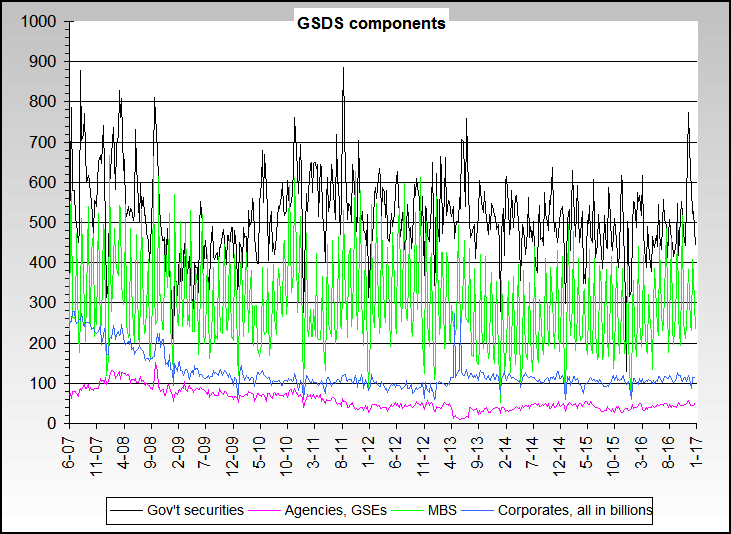

Here's one possible hint, but fairly esoteric. It's a record of the GSDS - Government Securities Dealer Stats - showing that there hasn't been much change in how the trading amongst the Fed's primary dealers for MBS instruments has been going.

They've been in the $300-500 billion weekly range for quite a while with only two exceptions - no liquidity issues to speak of.Leave a comment:

-

Re: Bernanke: Talks the Dove, Acts the Hawk

Originally posted by zoog View Post

Assuming we're still talking about the discount rate cut, yes. It's both a way to shore up confidence in the dollar and in the "system" itself.

The down move today in the USDX is probably related to the large outflow from the Fed custodials account last week... which measures, among other things, international confidence in the dollar.Leave a comment:

-

Re: Bernanke: Talks the Dove, Acts the Hawk

It confirms the portion of Ka-Poom Theory that predicts that during the unwinding of the Greenspan credit bubble (debt deflation) we are not likely to see monetary deflation, that is, a negative inflation rate. The debt deflation will largely occur via the dollar depreciation, inflationary Poom part of the process. The Fed's recent action supports the idea that no run-for-the-hills, banking system failure driven run-away money supply collapse is in the offing, with commodity prices due to fall in price by half�I heard this from some commentators last week. Instead, we will experience disinflation, that is, a falling rate of inflation and a rising dollar along with falling demand UNTIL the Fed acts to stimulate domestic demand.Originally posted by jk View Post

Despite the short term rise in the bonar, the negative long term prospects for the bonar remains. From today's WSJ:How a Gulf Petro-StateAs to your rate of change question, recent events in the credit markets remind me of why I first conceived of Poom as a sudden process. As we saw over the past few weeks, imbalances build for long periods of time and then change is very sudden when the basis of confidence in market forces supporting the imbalance suddenly evaporates. Prices that no one thought could change so rapidly, such as in the yields on short term treasury bonds and munis, moved in ways that not even the most creative out-side-the-box thinkers imagined. The guys on the Goldman call this Wed were clearly dumbfounded, and not in the manner of comments coming from managers of failed hedge funds whose "How could we have known?" statements are earning the derision of commentators now. They just couldn't believe what they were seeing.

Invests Its Oil Riches

Kuwait's Mr. Al-Sa'ad

Likes Asian Real Estate

But Is Cool to Treasurys

By HENNY SENDER

August 24, 2007; Page A1

KUWAIT CITY -- Kuwait is a world away from New Haven, Conn. But when a government investment fund here got a new chief in 2004, one of the first things he did was commission a study of the sophisticated ways Yale University invests its endowment.

It was a sign that Bader Al-Sa'ad intended to shake things up at the huge but sleepy Kuwait Investment Authority.

The investments he has since pursued put his fund at the forefront of far-reaching change in how the oil wealth of the Persian Gulf is deployed. Instead of mostly U.S. Treasury securities, Kuwait now invests in things like higher-yielding bonds, Chinese office buildings and Asian private-equity funds. And, in a move with implications for the strength of the U.S.'s currency and economy, the Kuwait fund is de-emphasizing holdings priced in dollars.

How a Gulf Petro-State Invests Its Oil Riches

Similarly, when the Poom part of the process does happen it will be sudden and create extreme market dislocations.Leave a comment:

-

Re: Bernanke: Talks the Dove, Acts the Hawk

So do you view this as more of a way to improve the dollar value vs other currencies?Originally posted by bart View Post

(speculating now) It seems to me that at some point they will have to lower the federal funds rate, but obviously don't want to do that while the $USD index is hovering down near 80. I'm sure they are now and will continue doing anything they can to raise that level higher before making that rate cut, (if such a cut becomes necessary in the future).Leave a comment:

-

Re: Bernanke: Talks the Dove, Acts the Hawk

Originally posted by Spartacus View Post

I don't believe it was intended to arrive at the end user.

I view as more of a confidence building attempt than a real move. In other words, it doesn't matter if it has been loaned out or not.

One of my favorite definitions of money is "an idea backed by confidence", and one of the primary jobs of a central bank is to support its currency.

Note that I'm not disagreeing with EJ's OMOF concept either.Leave a comment:

-

Re: Bernanke: Talks the Dove, Acts the Hawk

but does that count the money that actually made it to the troubled end-user?

So far all we know is that the banks have that money - has anyone borrowed it from them (did they actually intermediate? or is the money just sitting there? )

Originally posted by bart View PostLeave a comment:

-

The audio I posted earlier has a little history on the discount window

http://www.itulip.com/forums/showthr...4690#post14690

This type of operation had become hightly dis-favored for a long, long time and now is apparently being resurrected and repurposed.Leave a comment:

-

Re: Bernanke: Talks the Dove, Acts the Hawk

I have 2 problems with this approach:

1. Only $2B was taken from the Discount window. This is not enough to bailout even 2 large hedge funds as Bear Stearns found out.

2. The Discount window loans are for only 30 days. This postpones the day of reckoning to mid September while the redemption fiasco for hedge funds is at the end of September.

Still, the reality is that the equity markets and ABX index have calmed. So, the Fed's approach is temporarily working very well.Leave a comment:

-

Re: Bernanke: Talks the Dove, Acts the Hawk

I don't want to over-state the importance of this one method. Again, as there is no precedent, there is no way of evaluating whether the OMOF system will work long term. It does serve as evidence to support our belief that the Fed has thought this through and likely has more ideas than this one. The old maxim "don't fight the Fed" meant don't discount the Fed's ability to step in and support the system with rate cuts. Now it means don't underestimate the range of market engineering options that the Fed may develop and institute.Originally posted by ratfink View PostLeave a comment:

-

Re: Bernanke: Talks the Dove, Acts the Hawk

That is one of the more clever aspects of OMOF system. It creates a market where markets have previously frozen up. If only one bank stepped in to borrow $500M at the window to use to buy hedge fund and investment bank assets, then there'd be no pricing mechanism. Citi, BoA, etc., compete for the assets. The remaining mystery is how a market is to made for a glut of overpriced houses without a fed funds rate cut.Originally posted by metalman View PostLeave a comment:

Leave a comment: