Originally posted by don

View Post

-

Re: Pop goes the Globaloney Economy

Is that the right way around, I thought the old money was the FIRE/military? I grew up in England and it certainly was that way round there. My experience of US when I lived there was that it was the same but far more so - massive respect and brown nosing of old wealth. -

Re: Pop goes the Globaloney Economy - Eric Janszen

Originally posted by Chris Coles View Post

Ah, my mistake.

I assumed this was just for new house buying customers. It shows you just how stuck I am in my perception of an old fashioned banking system.

I'm definitely not 21st century. :rolleyes:

Wow, is all I can say now.

I think I had a past life in the 30s or 50s or something.

Oh man. Would the inflation from a weak exchange rate filter into wages and house prices too, or would the economy be too depressed to make much difference? I think that's a key question.Leave a comment:

-

Re: Pop goes the Globaloney Economy - Eric Janszen

Some commentary along the same line of reasoning, from historian Niall Ferguson, writing in the FT [Don Coxe made mention of this article in his weekly conference call Friday morning]:Originally posted by EJ View PostThe age of obligation

By Niall Ferguson

Published: December 18 2008 19:10 | Last updated: December 18 2008 19:10

In the Old Testament Book of Leviticus, God commands the children of Israel to observe a jubilee every 50 years. Nowadays we tend to associate the word with celebrations of royal anniversaries such as Queen Elizabeth�s golden jubilee in 2002. But the biblical conception of a jubilee was more precise: that of a general cancellation of debts...

...Is it really plausible that the cure for excessive leverage in the private sector is excessive leverage in the public sector? Might there not be a simpler way forward? When economists talk about �deleveraging� they usually have in mind a rather slow process whereby companies and households increase their savings in order to pay off debt. But the paradox of thrift means that a concerted effort along these lines will drive an economy such as that of the US deeper into recession, raising debt-to-income ratios.

The alternative must surely be a more radical reduction of debt. Historically, such reductions have been done in one of four ways: outright default, restructuring (for instance, bankruptcy), inflation or conversion. At the moment, more and more American households are choosing the first as a way of dealing with the problem of negative equity, while more and more companies are being driven towards bankruptcy. But mass foreclosures and bankruptcies are not a pretty prospect.

Inflation, by contrast, is hard to worry about in the short term, not least because the Fed�s expansion of the monetary base is leading to no commensurate expansion of the broad money supply; the banks would rather shrink than expand their balance sheets.

That leaves conversion, whereby, for example, all existing mortgage debts could be wholly or partly converted into long-term, low and fixed-interest loans, as recently suggested by Harvard�s Martin Feldstein. (In his scheme, the government would offer any homeowner with a mortgage the option to replace 20 per cent of the mortgage with a low-interest loan from the government, subject to a maximum of $80,000. The annual interest rate could be as low as 2 per cent and the loan would be amortised over 30 years...

Leave a comment:

-

Re: Pop goes the Globaloney Economy - Eric Janszen

yeah, and those barriers are going to get a lot lower now that the game is exposed. if this results in a less leveraged dependent society, well good, but if it encourages the masses to game the system with a "debt doesn't matter, I can always get out of it, so just get as much credit as you can" attitude, that's bad IMOOriginally posted by GRG55 View Post

It could be a good thing for the reasons you state, namely the consumer gets out from underneath that underwater mortgage, banks liquidate the repo assets and real estate prices come back down to be in line with incomes. AND iff Creditors eat the losses, not the taxpayer.This could actually be a "good thing' because it will force the asset price adjustments and debt resets to occur much faster than they did in Japan

But, the banks or holders or insurers of those defaulted mortgages or securities may become insolvent and the gov will bail them out - in fact, is this not what the TARP is/was for? So here again you have specific elements of the society being bailed out at the expense of another and larger group. The argument put forward by some that no one wants home price declines in their neighborhood, and so this kind of approach benefits all home owners is specious imo. Again, banks made the loans, and whoever holds the loan or portion thereof is an investor and has assumed the risk of default - it's capitalism 101.

I own a modest home with a mortgage, but I would think it a good thing for home prices to come down (so I and others wouldn't have had to borrow so much to buy even a modest home, make sense?)Leave a comment:

-

Re: Pop goes the Globaloney Economy - Eric Janszen

No, the mortgages do not seep into the system, the system brings them in as a logical part of the constant need to refi. When your initial "term" is up, and the rate changes, that is not simply a matter of telling you the rate has changed, it means you get a new mortgage and when they deliver the documents, you get no choice. So within the time needed for all the refi's to go through the entire system changes gear. Everyone that has to refi is now on a completely new deal....Originally posted by labasta View PostLeave a comment:

-

Re: Pop goes the Globaloney Economy - Eric Janszen

I suspect that the social/cultural barriers to walking away from a mortgage debt, or declaring personal bankrupcy, are probably much, much lower [and falling] in the USA than they were in Japan during its debt deflation.Originally posted by FRED View Post

This could actually be a "good thing' because it will force the asset price adjustments and debt resets to occur much faster than they did in Japan.Leave a comment:

-

Re: Pop goes the Globaloney Economy - Eric Janszen

Originally posted by FRED View Post

ok, I see.

So what you are saying is that these new kind of mortgages will seep into the economy, draining consumer spending at a rate similar to the number of these mortgages being issued.

An ever increasing burden. That is of course if people are duped into these mortgages. I suspect a lot of people would be, but it also might put off an awful lot of folks too. If this happens, won't these new mortgages kill house prices as coupled with rising unemployment, prices will further shoot down with no-one buying?

It people get wise, this could kill the mortgage industry dead coudn't it?

People would buy houses for cash or borrow from relatives. Jesus, back to the ole ole days.

Then, people would reduce consumer spending by saving to buy a house outright, so we come full circle again. Mmmm.

I think if no-one took on these new loans (less pressure in a declining house price market), then the mortgage industry would have to change back, wouldn't it?

Just trying to go though some logic hoops here I think.

Leave a comment:

-

Re: Pop goes the Globaloney Economy

Somewhat minor correction considering the context, but the First Bank of the United States existed from 1791-1811.Originally posted by whitetower View Post

In the overall area, some hints about the framers intentions can be derived by them having rejected a clause that would have given Congress the authority to issue paper money, and also rejecting another clause that would have specifically denied that ability to the federal government.

The Coinage Act of 1792 (which established the US Mint) wherein the dollar was defined as specific weights of gold and silver further muddies the waters.Last edited by bart; December 20, 2008, 11:57 AM.Leave a comment:

-

NY Times: Japan Offers US a Roadmap (for recovery)

Fred, you hit the nail on the head. Yves Smith, of www.nakedcapitalism.com, who is VERY sharp, agrees.

U.S. "elite" are starting to comment favorably on the "Japanese solution" for examples on how to resolve our problems here in U.S.

Below are Yves' comments, exerpts from NY Times article, and link to article.

So Now We Are Trying to Emulate Japan's Lost Decade?

US economists have relentlessly harangued the Japanese for their supposed mismanagement of their post bubble era, which has lead to nearly 20 years of low growth, borderline deflation, with a not-much-discussed, robust export sector.

Along with others, we complained in the early days of the Fed/Treasury emergency response that they were taking one of the worst elements of the Japanese playbook, namely, trying to prop up the value of dud assets, rather than figuring out how to do more price discovery and ameliorate the attendant reaction (not damage, mind you, the damage was already done when the bad loans were made). Yes, the Treasury has made some capital injections into banks, but without cleaning up the balance sheets, the benefits are limited. Even with supposedly more aggressive action on realizing losses, our banks act a lot like their Japanese pre-writedown zombie counterparts.

So in yet another "putting lipstick on a pig" initiatives, the authorities, having unwittingly copied the heretofore-seen-as-failed Japanese playbook, are now trying to reposition Japan as a source of valuable lessons.

Trust me, you would never have seen anything along these lines two year ago, starting with the title of the New York Times story "Japan Offers a Possible Road Map for U.S. Economy." Pretty soon, we'll have our very own Ministry of Truth (I kid you not, read the article).

From the New York Times:The Bank of Japan kept rates near zero for most of the last decade in an effort to end a long economic stagnation, and raised them only two years ago. Many economists say they believe that the zero interest-rate policy finally worked in Japan after regulators took aggressive steps that succeeded in restoring faith in Japan�s financial system and Tokyo�s ability to oversee it.Yves here. Why does this remind me of that phase of the Iraq war when the US claimed the problem was not how the war (notice how we never say occupation?) was going, but the perceptions of the war within Iraq, and launched a PR campaign? That was such an astounding success that it gets nary a mention these days.

Now, with the Fed and President-elect Barack Obama turning to the same sorts of unconventional policy tools to battle the worst global economic crisis since the Depression, economists and bankers say they hope that Japan�s lessons are not lost on Washington. They say the United States needs to take the same kinds of confidence-building steps, and much more quickly than Japan did....

Back to the article:Economists and former Bank of Japan officials say the biggest lesson they learned was that cutting rates alone has almost no effect when the financial system has fallen into a crisis as deep as the one Japan faced in the 1990s.Yves here. The need for writedowns along with recapitalization was the lesson of the widely-touted Swedish approach, in the wake of its early 1990s financial crisis. But Sweden went even further. It nationalized dud banks, replaced management, spun out bad assets into an independent company. That entity was deliberately overcapitalized, It was able to do triage on borrowers, liquidating ones that were goners, but more important, restructuring loans and often extending new credit to ones who looked viable.

Japanese banks simply refused to lend in an environment where borrowers could suddenly go bankrupt, saddling lenders with huge, unforeseen losses. The Bank of Japan tried even more extreme measures, like using its powers to create money to essentially stuff cash into the nation�s commercial banks in hopes they would start lending again.

Exasperated central bankers found that commercial banks just let the money pile up instead of lending it out.

Economists say the United States faces a similar situation, after the sudden collapse in September of Lehman Brothers created fears of additional failures. Economists also fault Washington for its inconsistency in dealing with the financial crisis, leaving the impression that it does not have a clear strategy for dealing with ailing lenders.

In Japan�s case, economists and former bankers say, credit began to flow freely again only after 2003, when regulators adopted a tough new policy of auditing banks and forcing weaker ones to raise new capital or accept a government takeover. Economists said the audits finally removed paralysis in credit markets by convincing bankers and investors that sudden failures were no longer a risk, and that the true extent of problems at banks and other companies was finally being revealed.

Economists say Washington needs to do something similar to make banks and financial companies more transparent, and reassure investors that there were no more collapses like that of Lehman Brothers on the horizon.

Back to the Times, this time for comic relief:Economists and former central bankers said another lesson from Japan�s experience was the importance of consistency. This became apparent in 2000, they said, during one of the bank�s more embarrassing episodes, when it raised interest rates, and lowered them back to zero a year later when the economy faltered.It's a little late to worry about consistency....Leave a comment:

-

Re: Pop goes the Globaloney Economy - Eric Janszen

As housing prices decline and unemployment rise, the order of 50% of all mortgages will fall into this category.Originally posted by labasta View Post

That has always been our position, since 1998. You are making an understandable logical leap. Yes, policies will try to keep people in their homes. No, the overall macro outcome will not be deflationary.How many of these new loans are people taking out now? Not many. At least not as many as before. If another housing bubble arises in say 20 years then we could go Japanese. But at the moment people are just sending jingle mail.

If this isn't like Japan, what does this mean?

Also, what about the exchange rate fiasco, boosting import prices for easy inflation. I think the UK and US would be looking at very strong inflation coupled with a shrinking economy. As you have already mentioned, a disorderly poom might occur as private investors flee, possibly resulting in hyperinflation.

That's not like Japan at all.Leave a comment:

-

Re: Pop goes the Globaloney Economy - Eric Janszen

I see your point Fred, but...

These full recourse loans have only recently started, haven't they?

If these loans had been made from 1995 onwards, I'd say your case for a Japan re-run would be strong.

How many of these new loans are people taking out now? Not many. At least not as many as before. If another housing bubble arises in say 20 years then we could go Japanese. But at the moment people are just sending jingle mail.

If this isn't like Japan, what does this mean?

Also, what about the exchange rate fiasco, boosting import prices for easy inflation. I think the UK and US would be looking at very strong inflation coupled with a shrinking economy. As you have already mentioned, a disorderly poom might occur as private investors flee, possibly resulting in hyperinflation.

That's not like Japan at all.Leave a comment:

-

Re: Pop goes the Globaloney Economy

Here's the "life isn't fair" answer.Originally posted by Smitty View Post

Politicians elected by FIRE Economy are busy re-creating the Japan 1990 to who knows when scenario for the US. In Japan, mortgages are full recourse. So are the new loans being offered by the now nationalized Fanny and Freddie that are designed to replace existing mortgage loans are for all intents and purposes full recourse.

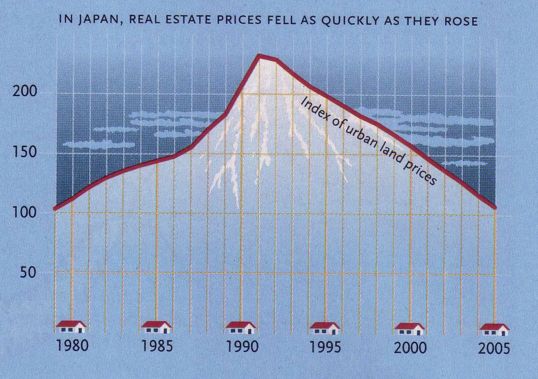

If this happens in the US, cash flow from US households will be drawn off for 20 years until all of the debt taken on during the housing bubble is paid off. Here's what will happen to your home price.

Never mind what it will do to the US economy and your opportunities to invest because the only source of savings will be export earnings, and in a shrinking economy, as this post forecasts, where is the export demand going to come from?

Leave a comment:

-

Re: Pop goes the Globaloney Economy

Not quite. To coin and to print are substantially different actions, and if you have been reading iTulip.com for a while you will know how critical the distinction is.Originally posted by whitetower View Post

Leave a comment:

-

Re: Pop goes the Globaloney Economy

As a debtor who bought during the government engineered for FIRE Economy interests housing bubble we propose that mortgage holders owe only that portion of home price that was not produced by the government sponsored asset price inflation.

For example, if comparable houses in your area sold for $100K before the bubble and $300K at the peak and $150K now, and you bought at $250K with $0 down, you still owe $100K but the bank has to eat the $150K asset price inflation difference.

What's wrong with that?----------------------------------------------Originally posted by FlyingBoat View Post

Totally agree with FlyingBoat. To tag only the banks is scapegoating. The greed that led people to buy houses with "liar's loans" should not be rewarded. The banks must suffer as must the greedy liars.Last edited by FRED; December 20, 2008, 09:55 AM.Leave a comment:

Leave a comment: