Re: How much house should you finance? Follow the 20/28/36 rule.

One thing to remember when looking at inflation rates - these are multipliers - and hence when calculating average rates, we should use a geometric mean, and not a arithmetic mean.

-

Re: How much house should you finance? Follow the 20/28/36 rule.

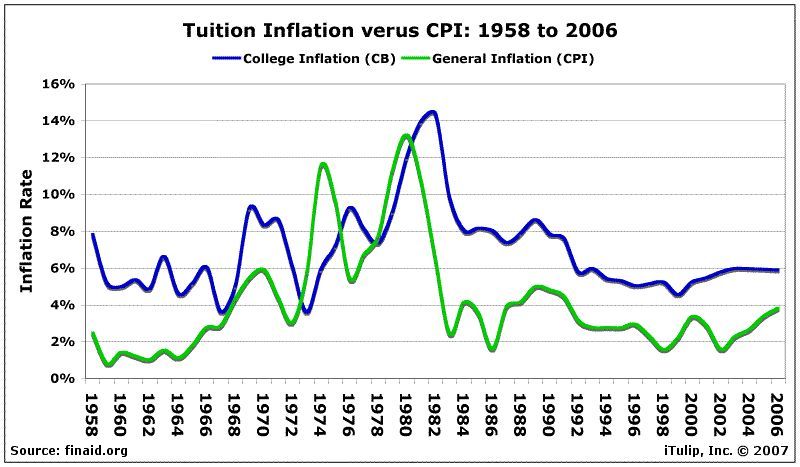

Tuition inflation running ahead of CPI inflation appears to be a long term trend.

From 1958 when the data series starts, tuitions ran about five times the rate of CPI inflation at around 5%. During the period of CPI inflation that started in 1964 and peaked in 1981, CPI inflation in some years exceeded tuition inflation. Since the post Volcker Fed period after 1982, tuition inflation has settled in at about 1.6 times CPI inflation. Note also that tuition inflation increases and decreases lag CPI changes by about a year. With CPI inflation rising since 2002, tuition inflation appears likely to rise to 6% from 5% this year.

Leave a comment:

-

Re: How much house should you finance? Follow the 20/28/36 rule.

The other Cost item that has been outpacing inflation is health care. and that has been rising at 2 1/2 times inflation. See Health Care Costs 101

And Education and Health Care are the two places where any proposed solution is greeted by shouts of "SOCIALISM" (Gasp!!) :rolleyes:

Sorry got the wrong URL. It has been corrected now!Last edited by Rajiv; January 25, 2007, 11:04 PM.Leave a comment:

-

Re: How much house should you finance? Follow the 20/28/36 rule.

But the problem is that college tuition is rising at twice the general inflation rate. So it is extremely unlikely that stagflation will enable what you propose -- unless banks charge a low rate -- but that then giving free money away would be regarded in some rarified circles as "SOCIALISM"is this a set-up or what? inflation, dude! that's how he's gonna pay it off. add a zero into the end of that nominal income. that's the ticket!Leave a comment:

-

Re: How much house should you finance? Follow the 20/28/36 rule.

is this a set-up or what? inflation, dude! that's how he's gonna pay it off. add a zero into the end of that nominal income. that's the ticket! now let's do the math:

median salary for a pharmacist in 2015 is b$988,280 (b$ is bonars, man) or approx. $680,000 per year after taxes, $57,000/mo. to pay off his $150,000 student loans from 2008 - 2014 undergrad and grad school in two years, he needs to pay $6,250/mo. or 11% of his after-tax income. no problemo!!!Leave a comment:

-

Re: How much house should you finance? Follow the 20/28/36 rule.

Having gone to grad school in the early to late 70's, I see how much more of a burden we have added on to the backs of young people. It started in the Reagan era, when government support for educational institutions was cut way back. The efforts at privatization have just accelerated the burden on the students.

I remember that it was possible to get a 4 year college education working 30hours a week at the sandwich shop (from 6pm to 10pm - 7 days /wk)) - going home to a large 6 bedroom house shared between 8 people -- studying till 2am - getting up at 8 am - rushing to class. Hard work, but that 30 hours a week of low wage work enabled you to do it -- college costs were low enough and you got your education without being in debt. But today that is an impossibility.Leave a comment:

-

Re: How much house should you finance? Follow the 20/28/36 rule.

You know what's funny as i sit here with my 20k in student debt after having graduated 4 and a half years ago from grad school, I had never considered this. Everyone has student loan debt nowadays - everyone. I just kind of assumed that it's always been like that and my situation isn't that crazy, but after reading this thread i kind of had a "duh" moment. And I'd probalby have closer to 40-50k if my parents hadn't significantly helped out with the loans.Originally posted by Rajiv

I know plenty of people who are graduating in my field (starting salary around 50k/year) of well over 100k, and they work weekends to be able to make 1000/month student loan repayments. I thought I was getting a deal at 400/month for student loan payments but now I just go uuuuuuugh.

In any case that's just one man's story. I'm way better off than most people though, from what I see.Leave a comment:

-

Re: that's exactly the type of info I was asking about

people do seem to be trying to cut expenses but just cannot do it - it's either pay the piper or do without, and doing without is painful - without a 4 year degree one's career choices these days are limited.

Originally posted by RajivLeave a comment:

-

Re: How much house should you finance? Follow the 20/28/36 rule.

You should read Generation Debt: Student Loans, Credit Cards, and Their Consequences

And here is the data on college cost and inflation. This is the main reason for the increased student loans.In the 1992-93 academic year, just over 49 percent of graduates from 4-year state universities had taken out federal student loans. By the end of the decade, nearly 65 percent of college graduates had taken out such loans. In the decade since the legislative change, inflation-adjusted student loan volume has risen by 137 percent.Last edited by Rajiv; January 24, 2007, 09:45 PM.Leave a comment:

-

Re: How much house should you finance? Follow the 20/28/36 rule.

We subject our readers to many intelligence tests, sometimes on purpose. We sleep soundly tonight, reassured that the second smartest man on earth can tell the difference.Originally posted by JeffLeave a comment:

-

Re: How much house should you finance? Follow the 20/28/36 rule.

EJ, I've always said you were the third smartest man in the world, but how you got a dateline of December 2007 escapes me. Could you bring back a WSJ for me so I can make some time in the market?Leave a comment:

-

Re: How much house should you finance? Follow the 20/28/36 rule.

Today, a Bachelor's is the equivalent of a HS diploma 20 years ago. A BS or BA is no sure thing for a "career", and now many professions are requiring a Master's or even a Ph.D. for significant career advancement. So you're not just talking tuition for undergrad, but grad as well. If one is lucky, as I was, they'll take a job for a university and use that benefit to get a free or discounted advanced degree. I did that at Johns Hopkins. The pay absolutely sucked for the 5 years I was there, but I got a free MS from an ivy! Now I've moved on to bigger and better things, because although Hopkins will pay for your school, once you get that advanced degree, no pay raise for you!Originally posted by Spartacus

If I could do it over again, however, I would have taken the other route. Find a job with a company that will pay for your advanced degree, or at least contribute significantly to tuition.

My point is that an advanced degree is becoming more of a requirement, and not everyone can be a TA or work for a university. School debt continues after 22, and if one is in grad school, paying tuition until they're 30, that pushes the timeline out even further.Leave a comment:

-

Re: How much house should you finance? Follow the 20/28/36 rule.

Are we talking about people who refuse to live at home and go to a decent but cheap state school

or people who have to have an Ivy League degree and absolutely have to go to college on the opposite coast?

EDIT: I just looked at the pictures again and i realized I'm saying that these people may be getting the equivalent of the BMW, on credit.Originally posted by EJLast edited by Spartacus; January 24, 2007, 04:45 PM.Leave a comment:

-

Re: How much house should you finance? Follow the 20/28/36 rule.

That's an excellent point and a topic for another article. On the moral side, it's simply wrong for young people to have to start their lives in debt. They don't have much choice. Here's a good USA Today article by Sandra Block:Originally posted by Rajiv

Students suffocate under tens of thousands in loans

Tom Dillon, 19, a pre-pharmacy major at the University of Connecticut, is carrying $52,000 in student loans. And he's just getting started. When he gets his pharmacy doctorate in four years, he expects his debt to exceed $150,000. Dillon's been drawn to pharmacy since age 5, when he found out he had epilepsy.

"The first person who helped me was my pharmacist," he says. Dillon, who no longer has epilepsy, would like to go into pharmaceutical research. But he knows he'd earn more money as a pharmacist for one of the big drugstore chains.

"When I get out, I'm going to have that $150,000 weighing over me," he says. "What I decide is going to be dependent on that debt."

And the cost of that debt is about to rise. On July 1, the rate on new federally guaranteed student loans will hit a fixed 6.8%, the highest rate since 2001. It comes as the average graduate owes $19,000. Many undergrads, though, have debt exceeding $40,000.

Those higher payments carry huge implications for this generation of college graduates. The weight of debt is forcing many to put off saving for retirement, getting married, buying homes and putting aside money for their own children's educations.

Heavy student debts may also keep young adults from starting businesses, says Diana Cantor, director of the Virginia College Savings Plan. Some graduates will refuse to risk what little money they have on entrepreneurial ventures. And securing loans will now be harder. "It's a real crisis," Cantor says. "You're strapped before you get started."

"Low mortgage rates" have not "eased the impact of soaring home prices" but rather have caused them. The Monthly Payment Consumer accepts the new higher total cost of a house because the monthly cost was made affordable by low rates and creative financing. A different dynamic drives up tuitions. Without a college education, earning potential is very limited in the US. Yet with a college education, a middle class undergrad student graduates with close to $20,000 in debt. This student debt is bad news for two main reasons: 1) students don't have enough credit left to use to start a business, the best way to build wealth, and 2) they don't have enough credit to buy a house, the second best way to build wealth.

The average debt for a college graduate has soared 50% in the past decade, after inflation, according to the Project on Student Debt, a non-profit advocacy group. Just as record-low mortgage rates have eased the impact of soaring home prices, low student-loan rates have let borrowers cut their payments, softening the impact of rising debt.

The median salary for a pharmacist is $98,828 or approx. $68,000 per year after taxes, $5,700/mo. To pay off his $150,000 student loans in ten years, he needs to pay $1726/mo. or 30% of his after-tax income.

If that's typical, I wonder how this generation is going to have enough money to pay into the entitlements system if they also have to pay off these college education debts.Leave a comment:

-

Re: How much house should you finance? Follow the 20/28/36 rule.

While what you say makes sense, you forget to include one very important fact that occurs in today's world. Young people coming out of school are already saddled with a very large burden of student loans. This conceivably will put off home buying for five to seven years. This would imply that the first home is not bought at the age of 25 as you suggest, but closer to the mid 30's. Given the earning life span of a person, it makes home equity even more distant.Last edited by Rajiv; January 24, 2007, 10:02 AM.Leave a comment:

Leave a comment: