Tweet

Tweet

Roland Flexner, Untitled, 1992

Illusion of Recovery – Part I: Print and pray has officially failed

It’s 1938 all over again

• Mid-gap recession arrives

• Last call for fire sales

• We’re all goldbugs now

• Our ten-year-old gold plus Treasury bonds portfolio melts up

• The slow stop before the sudden stop

• Get ready for Emergency Measures

I warned in my 2010 book The Postcatastrophe Economy: Rebuilding America and Avoiding the Next Bubble

that the US was in a race against time to get its economic house in order. The window of opportunity to get the economy back on a strong growth track was approximately two years starting in the second quarter of 2009.

that the US was in a race against time to get its economic house in order. The window of opportunity to get the economy back on a strong growth track was approximately two years starting in the second quarter of 2009. By the time my book came out in the fall of 2010, I was warning in book tour interviews that recovery policies were taking us in the wrong direction, that attempts to restart the FIRE Economy -- the economy oriented around the finance, insurance, and real estate industries -- will fail at the expense of the Productive Economy -- the economy of goods and services producers that employs over 90% of consumers.

If policy makers persist with this wrong-headed approach, I warned, the result will be persistent high unemployment, a depreciating dollar, rising consumer price inflation, falling home prices, and rising budget deficits.

I further warned that if the economy is permitted to fall back into recession while still recovering from the previous recession we risk a crisis of confidence in US government bonds and the US dollar as foreign investors withdraw support for the economy by reducing or even withdrawing investment, leaving more of the burden of deficit financing to domestic bond buyers. In so doing they may precipitate the very condition they fear: a collapse in tax revenue and national creditworthiness, launching a sudden stop process, a kind of national run on the bank. A sharp run-up in gold prices will presage a sudden stop that we have modeled here as Ka-Poom Theory since 1999.

Congress did not understand the urgency of the mission to restructure the economy toward productive activity and away from finance-based activities, if they understood that as the mission at all.

They argued and experimented, as if we had all the time in the world to exhaust all other options before doing the right thing.

Now, as Q3 2011 winds down and we head into the fall, it’s apparent that our two-year deadline has come and gone -- and the stock market knows it.

The best opportunities for sustained recovery have been squandered. Now we’re in real trouble. Getting out of it will not be as simple as the print, spend, and wait policy formula of the past three years that has failed to spur growth, produce jobs, and get the economy going again.

Time’s Up: Mid-gap Recession Arrives

The incipient recession that the stock, bond, and gold markets smell is not a so-called “double dip” recession. It is a mid-gap recession, a recession that occurs in the midst of an output gap, a far more serious economic event than a recession that produces an output gap. The US has not experienced a recession inside of an output gap since 1938, except for one produced on purpose by the Volcker Fed in 1983 to squeeze the last breath of life out of an inflation spiral that was showing signs of resurgence in 1982.

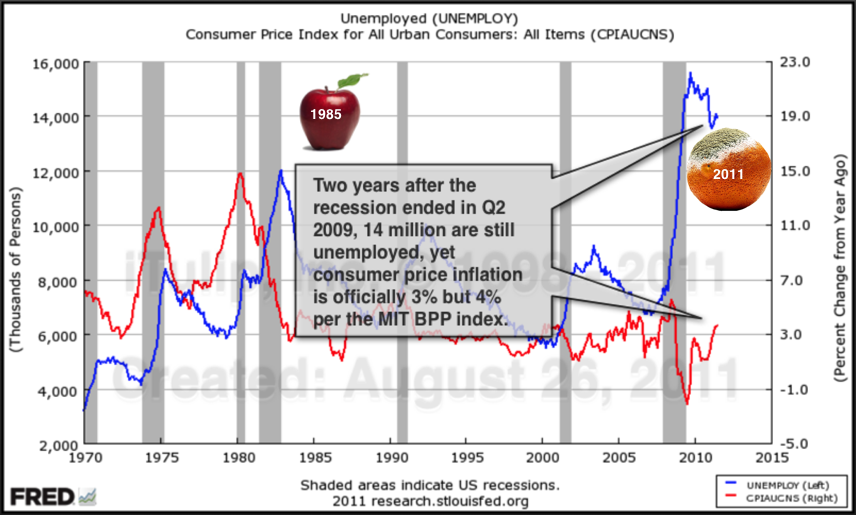

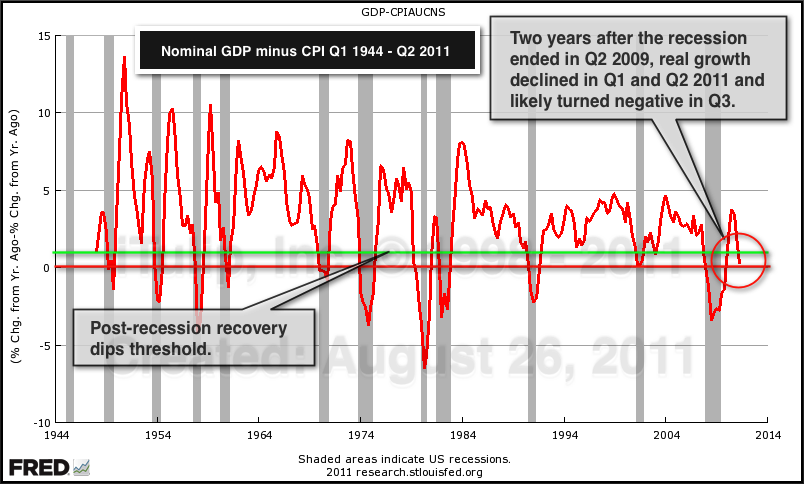

I published the chart below in June 2009 to help readers to understand that the key characteristics of the recession that we had been in since Q4 2007 were the opposite of those of the 1981 to 1983 recessions. At the time the two periods were frequently and incorrectly equated and I wanted readers to filter out such misguided comparisons.

The 1981 to 1983 recessions were manufactured by the Fed with double digit short-term interest rates designed to kill off the inflation spiral that ran from 1975 to 1980. The inflation of that period wiped out private sector debt -- mortgage and credit card debt, auto and student loans, and corporate debt – that accumulated on household and business balance sheets over the previous decades. As a result, the Reagan administration started with a clean slate of low private sector debt levels, virtually no public sector debt, and a massive tail wind of falling interest rates that fueled the growth of the finance-based economy.

By the end of Reagan's first term in 1985, two years after the recession that ended in 1983, the number of unemployed had fallen from 12 million to 8 million as inflation fell from 15% to 3%. Reagan's re-election bid was assured.

The so-called Great Recession, in contrast, was not manufactured to kill off an inflation spiral that wiped out a generation’s debts. It followed a seizure of the great credit machine that fueled the nation's growth since the early 1980s and left it buried under a mountain of both private and public debt.

The Fed cut rates to zero and via quantitative easing and other monetary tricks attempted to get the machine going again. Rather then exit the recession with private sector debt wiped out and public debt near zero as in 1983, in 2009 private debt levels were higher than ever, and deficit spending to stimulate the economy expanded public debt well beyond the already worrisome levels reached before the recession.

The result is the outcome I warned about in 2009: high unemployment, high inflation, and high deficits.

Here’s is the same chart updated to August 2011.

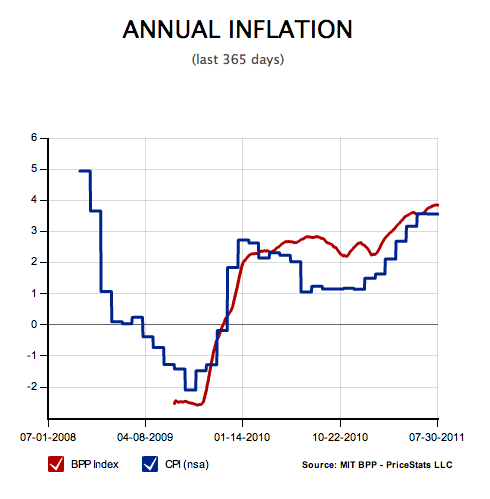

Two years later more than 14 million Americans remain unemployed and consumer price inflation is officially over 3%, but is closer to 4% according to the MIT Billions of Prices Project price index.

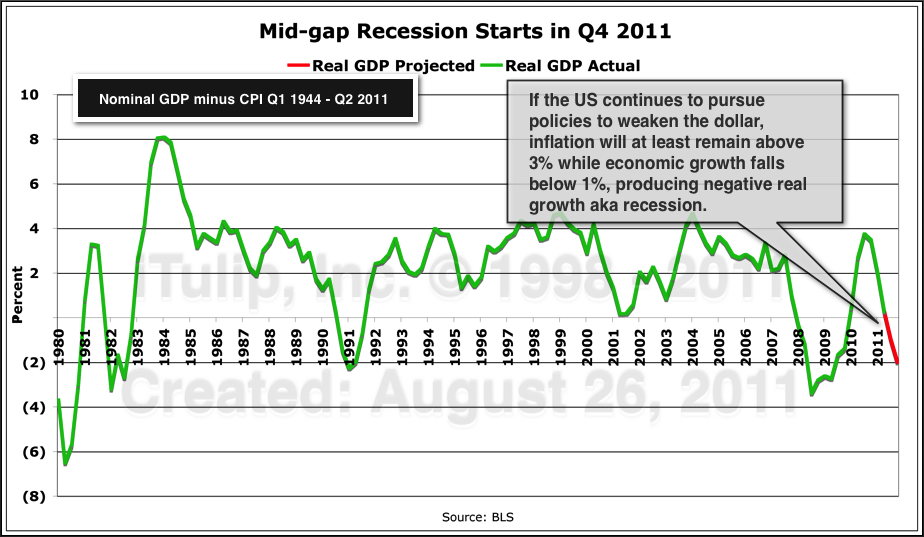

Yet for all of the printing and spending starting in 2009, and the Fed's success at producing inflation as Bernanke promised, all evidence points to recession by Q4 2011. In fact, the economy may have entered recession in Q2.

The evident downward trend in economic growth two years into recovery is highly unusual from a historical perspective.

Since the Fed is locked into a deflation-fighting stance, inflation will be maintained above a 2% annual rate even as nominal growth declines to below zero. The result: negative 2% annual growth rate by Q4 2011.

We had two years to close a trillion dollar output gap, but we blew it.

Yesterday’s cure is today’s disease

Money supply expansion via central bank operations, government spending, and direct cash injections into failing financial institutions stopped the financial crisis in its tracks. Fed chairman Ben Bernanke kept the promise that he made to prevent a repeat of the deflation spiral and economic contraction that gripped the US economy from 1930 to 1933. I noted in 2006 a Fed paper on deflation that pre-dated by six months Bernanke's now famous 2002 speech titled “Deflation: Making Sure "It" Doesn't Happen Here.”

"Once inflation turned negative and short-term interest rates approached the zero-lower-bound, it became much more difficult for monetary policy to reactivate the economy. We found little compelling evidence that in the lead up to deflation in the first half of the 1990s, the ability of either monetary or fiscal policy to help support the economy fell off significantly. Based on all these considerations, we draw the general lesson from Japan’s experience that when inflation and interest rates have fallen close to zero, and the risk of deflation is high, stimulus–both monetary and fiscal–should go beyond the levels conventionally implied by baseline forecasts of future inflation and economic activity."

Board of Governors of the Federal Reserve System

International Finance Discussion Papers – Number 729 – June 2002

Preventing Deflation: Lessons from Japan’s Experience in the 1990s (pdf)

But Bernanke's speech was more colorful and clearly addressed to a wider audience. He asserted that the misguided, ideological laissez-faire policy approach to the previous credit bubble crash in the 1930s will not be repeated on his watch. Instead, an activist and radical reflation policy will be pursued. And he made a reference to gold that he may regret today.Board of Governors of the Federal Reserve System

International Finance Discussion Papers – Number 729 – June 2002

Preventing Deflation: Lessons from Japan’s Experience in the 1990s (pdf)

"The conclusion that deflation is always reversible under a fiat money system follows from basic economic reasoning. A little parable may prove useful: Today an ounce of gold sells for $300, more or less. Now suppose that a modern alchemist solves his subject’s oldest problem by finding a way to produce unlimited amounts of new gold at essentially no cost. Moreover, his invention is widely publicized and scientifically verified, and he announces his intention to begin massive production of gold within days. What would happen to the price of gold? Presumably, the potentially unlimited supply of cheap gold would cause the market price of gold to plummet. Indeed, if the market for gold is to any degree efficient, the price of gold would collapse immediately after the announcement of the invention, before the alchemist had produced and marketed a single ounce of yellow metal.

"What has this got to do with monetary policy? Like gold, U.S. dollars have value only to the extent that they are strictly limited in supply. But the U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. By increasing the number of U.S. dollars in circulation, or even by credibly threatening to do so, the U.S. government can also reduce the value of a dollar in terms of goods and services, which is equivalent to raising the prices in dollars of those goods and services. We conclude that, under a paper-money system, a determined government can always generate higher spending and hence positive inflation.”

At the time Bernanke gave this speech I doubt he had any idea how prophetic his statement about gold and fiat dollars was to be after he executed his inflation plan five years later to fight off a post-crisis deflation spiral. "What has this got to do with monetary policy? Like gold, U.S. dollars have value only to the extent that they are strictly limited in supply. But the U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. By increasing the number of U.S. dollars in circulation, or even by credibly threatening to do so, the U.S. government can also reduce the value of a dollar in terms of goods and services, which is equivalent to raising the prices in dollars of those goods and services. We conclude that, under a paper-money system, a determined government can always generate higher spending and hence positive inflation.”

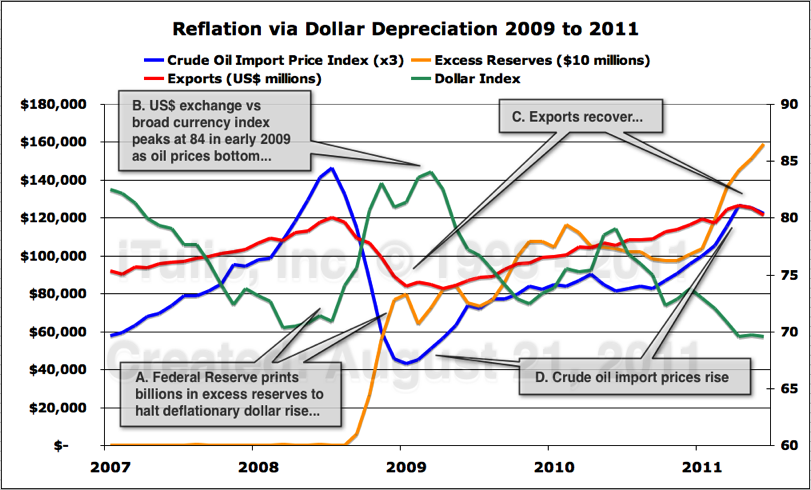

But the “production of as many U.S. dollars as it wishes” by the Fed has not come “at essentially no cost.” Trillions of dollars of credit and money expansion ran head long into a few thousand tons of gold that cannot in fact be expanded rapidly and at no cost. Anti-deflation policy – a pro-inflation policy by any other name – weakened the dollar and every currency on earth, as we shall see, and exploded the gold price more than five-fold from $300 at the time of his speech to over $1700 at this writing.

A consequence of government spending and zero interest rates is a depreciating dollar. The policy succeeded at boosting exports over the following quarters and years, but the immediate aim of dollar depreciation policy was not to improve the prospects of US producers but to halt asset price deflation in the FIRE sector with cost-push inflation from rising energy import prices.

A similar strategy that was executed by FDR under similar circumstances but using gold instead of oil as the price anchor. In 1933 FDP halted a runaway deflation spiral by calling in gold and devaluing the dollar against gold by 70%. As I forecast in my book, without an international gold standard the unspoken strategy this time around was to not wait three years for deflation to get out of control but to move immediately – via aggressive interest rate and fiscal policy - to depreciate the dollar against oil. And so it was.

The immediate impact of these policies was positive. Credit contraction and deflation stopped in their tracks. While I have argued since 2006 that the original sin was to allow so much private sector debt and financial sector credit risk to build up in the global financial system in the first place, no serious economic observer argues that the policies that Bernanke envisioned and later executed were not necessary to prevent the economy from collapsing once the inevitable crisis began.

The pilots who flew us into this hurricane were Alan Greenspan and the Reagan, Clinton, and Bush administrations that he served under. Bernanke did not have the option of compounding the error by putting the plane on autopilot and hoping for the best. That does not mean that Bernanke will not be the scapegoat for inflationary policies in the future. But the real culprits here are in the White House and Congress, who failed to follow emergency reflation measures with viable long-term solutions.

Two years later we have the worst of all worlds. The US economy is not “catching” and growing steadily under its own power as it must in order for monetary and fiscal stimulus to be withdrawn. Yet if stimulus is continued, consumer price inflation, nacent but persistently growing, will get out of control.

Running out of time and options

I said in 2010 we had until 2011 at the latest to get the economy ramped up to a sustained 4% annual real GDP growth rate. I suggested a way to do this by investing public funds into energy and communications infrastructure projects to boost growth to a 4% level. Rather than adding to the nation’s debt burden, these government outlays produce a return on investment on borrowed taxpayer money by reducing the energy intensity of the US economy, the number of BTUs of energy needed to produce a dollar of GDP. Such a reduction is as stimulative as a tax cut and for the same reason: household income now devoted to fuel and food is freed up for spending on other goods and services.

But we didn’t do that. Instead we wasted the two years and trillions of dollars, mostly borrowed, on a haphazard and misguided mix of projects, from “Cash for Clunkers” to make-work maintenance of existing transportation infrastructure.

Then we wasted more time arguing about whether the nation has too much public debt, when in fact public debt as a portion of total private and public debt outstanding is only 6% of total debt, down from 13% in the 1960s. Financial corporate debt, on the other hand, has over the same period grown from 2% to 37% of total debt.

It is this excessive financial sector debt that is weighing down the economy and preventing the economy from recovering at a high enough rate to close the output gap. It is why this recovery is unlike any other, and why every recovery since 1980 has been weaker and weaker, generating fewer and fewer jobs, and requiring more and more new debt growth to get the economy going again.

Finally, to cap two years of fumbling, Congress passed a bill to reduce government spending, a decision that can only slow the economy even further and make existing debt even more difficult to finance.

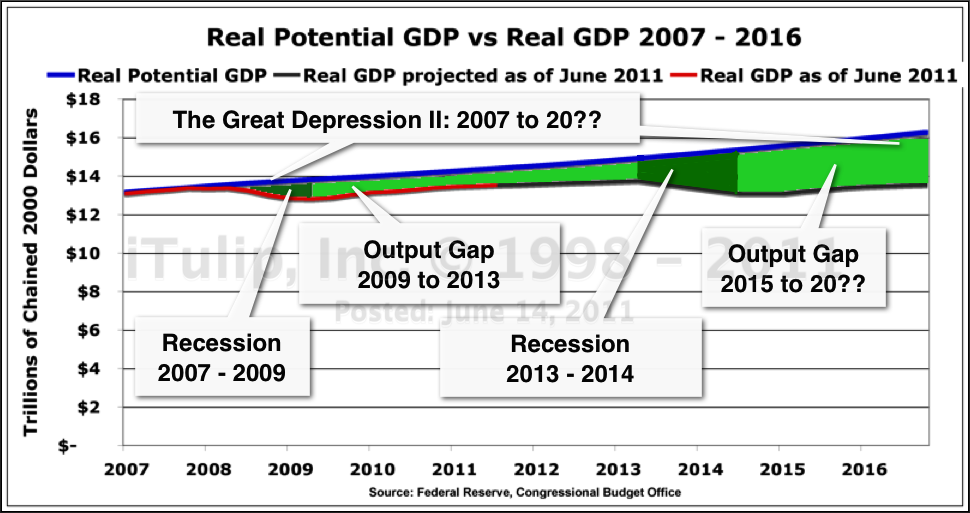

Implications of the Mid-gap Recession

To understand the meaning of the new recession that is upon us it's important to get your head around the last mid-gap recession that happened despite muddled efforts to avert it.

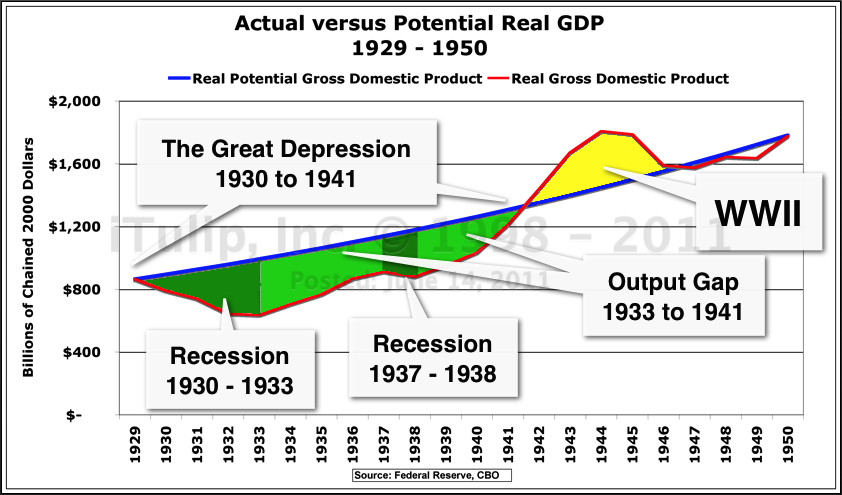

The Great Depression happened in two parts. Part I was a massive recession that saw GDP decline by 25%. Part II was an output gap, the gap of between the potential output of an economy under conditions of low inflation and full employment. New Deal spending closed the gap from 24% to 14% of GDP.

But New Deal stimulus spending was cut in 1937 after months of partisan bickering about the risks to the nation’s credit that deficit spending posed. Sound familiar? The spending reductions caused a new recession that widened the output gap to 17% of GDP. By the end of 1941, WWII spending, acting as gigantic public works project, closed the output gap and created a positive gap with high inflation.

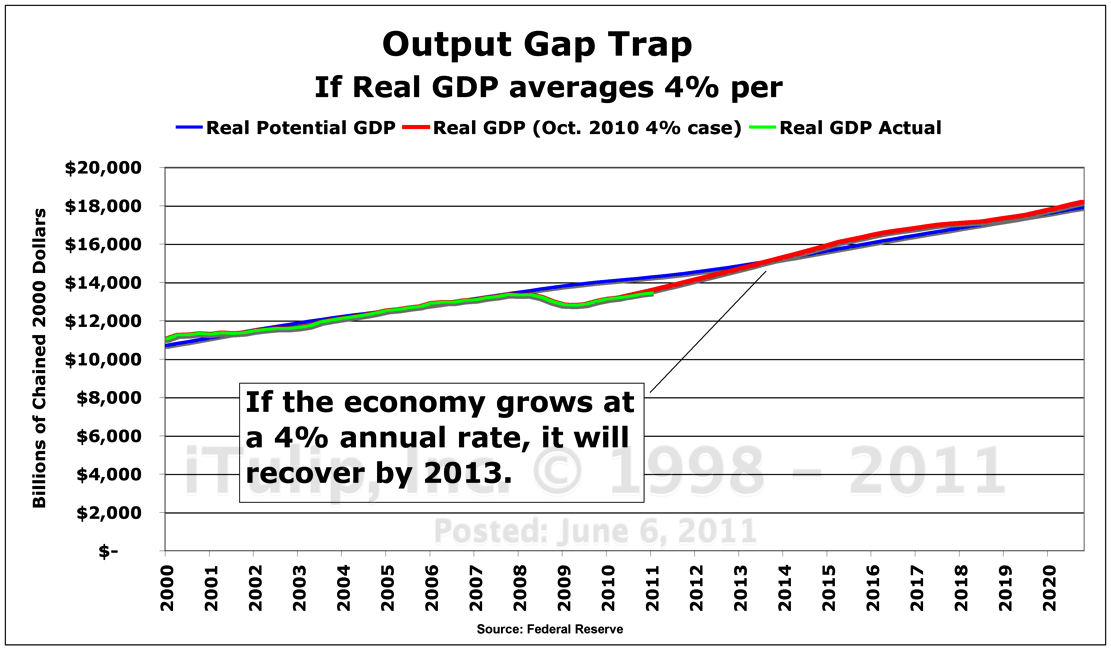

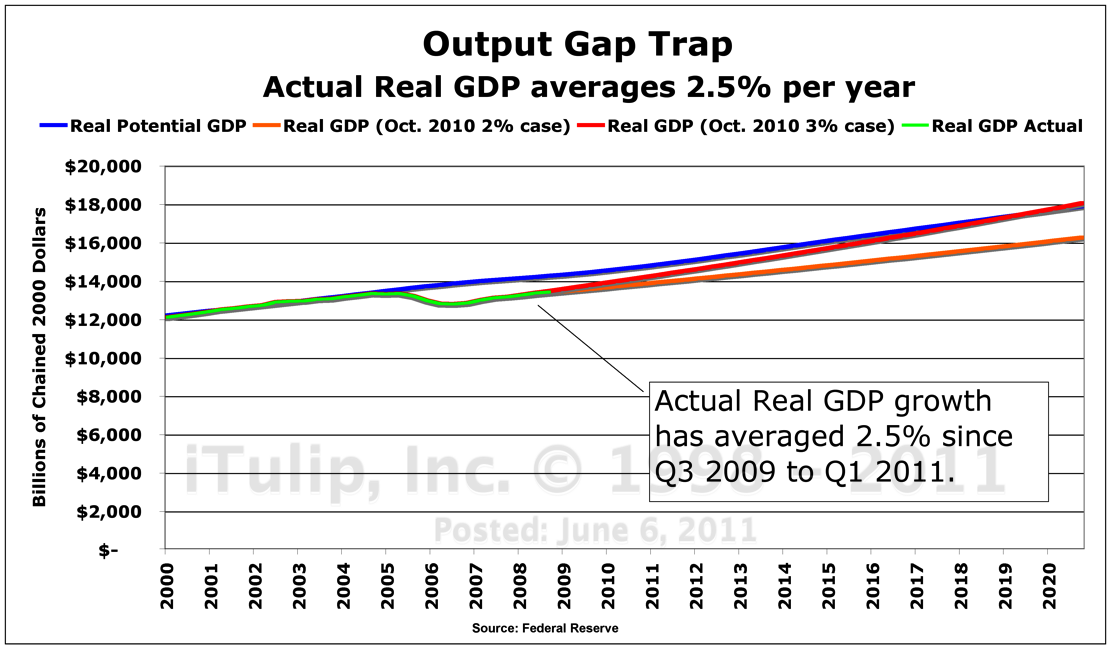

The current depression, like The Great Depression, is also happening in two parts. The 2008 to 2009 recession left a more modest output gap of 4% of GDP, thanks to the Bernanke Fed's radical reflation approach. To close this gap by 2013, the economy needed to grow at an average of 4% per quarter starting in Q2 2009.

A combination of monetary policy and stimulus spending helped close the output gap to 2% of GDP by the fourth quarter of 2010. But growth has averaged only 2.5% of GDP since the recovery began in the second quarter of 2009, not the 4% we need to close the gap. At that rate, the gap was never going close. Ever.

But that, believe it or not, is the good news. Today the BLS revised Q1 GDP growth down from 1.9% to 0.4% almost no growth, and the first pass at Q2 growth is 1.4%. The past record of revisions during our feeble crawling out of the output gap suggests another cut to near zero or negative growth is likely.

Deficit reductions spelled out in the Budget Control Act of 2011 virtually guarantee that the economy, already teetering on the edge of recession in the first half of the year, will fall into recession and contract in the second half of the year.

This political acceleration into a mid-gap recession is occurring a full two years before my previous projection of a next recession occurring in 2013 if the US fails to pursue a program of energy and communications infrastructure targeted, ROI producing stimulus programs. Once again, try as I might, just as I failed in 2001 to imagine that our leaders were crazy enough to create a housing bubble to bail the economy out of the fallout from the tech stock bubble, I was unable to think darkly enough to foresee the economic nightmare our leaders were capable of creating with alacrity.

With the onset of a new recession, the current output gap will open further, and for nearly identical reasons as in 1938: fiscal stimulus was cut before the output gap was closed.

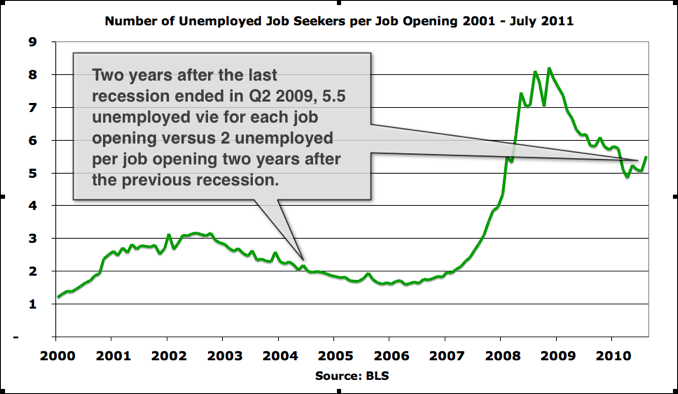

An output gap is the difference between the output of a productive economy running at full capacity and an economy running below capacity. Potential output is the old trend growth rate of the economy. It represents the good old days of 2006, with only two unemployed vying for each job opening, the prosperous economy that both producers and consumers – and investors – still hoped until July was just around the corner.

Now they know it isn’t.

The output gap we are in today is the difference between the actual output of the economy after the 2007 to 2009 economic contraction versus the potential output of the economy at full employment without inflation if the financial crisis and economic contraction had never happened.

The gap created by the global financial crisis and recession must be – must be -- closed before the next recession arrives to widen the gap further, I warned in 2010. If that is not accomplished the US will find itself in an economic predicament far more dire than the one posed by the fallout of the financial crisis.

I warned that if we don’t make the Q2 2011 deadline to get the US economy moving again at a 4% annual growth rate the US will run out of foreign buyers for its government debt and sooner or later face a full-blown debt and currency crisis. As the US is at the center of the global monetary system, and over 80% of the world’s international transactions are dollar-based, a dollar crisis is a global economic calamity without precedent that will drag all other currencies down with it, with no quick-fix solution like the multi-trillion dollar global fiscal stimulus and bailouts that pulled the world economy back from the brink in late 2008 and early 2009.

This second recession will put US finances on an even more precarious footing.

When in 2009 I forecast a next recession for 2013, I said: "The other antecedent to recovery to keep in mind is government spending. We’re not supposed to worry about this because we’re going to grow our way out of it, but try to imagine what might happen if the next recession occurs before tax receipts recover to previous levels while government outlays are cut. We think it might go something like this. Might deficit spending to stimulate the economy in a next recession produce a $4 trillion shortfall, or 21% of GDP?"

I supplied the following as a warning of the consequences of a failure to avoid a recession before the US exits its post-recession output gap.

Might deficit spending to stimulate the economy in a next recession

produce a $4 trillion shortfall, or 21% of GDP?

The chart above highlights the major difference between the 1938 relapse into recession and the current version: today the US is a major net foreign debtor versus a lender. If the US government debt-to-GDP ratio reaches 20% or perhaps even 15% of GDP, the dollar will come under even heavier pressure.

The past two months stock markets crashed around the world and gold prices soared as global investors decided that the US has lost its race against time. A new recession is upon us before we even half-closed the output gap left open from the last recession.

It means even larger deficits and an even weaker dollar. The price of gold and Treasury bonds is telling us that a full-blown international bond and currency crisis is approaching.

There is no international policy mechanism available to stop the panic short of re-opening the gold window that the US closed unilaterally and “temporarily” in 1971.

In 1980 interest rates had one way to go if the Fed was determined to stop an inflation spiral from developing into full blown hyperinflation: down.

Inflation had one way to go: down.

The dollar had one way to go: up.

Today the opposite is the case.

Interest rates have one way to go: up.

Inflation has one way to go: up.

The dollar has one way to go: down.

Gold is starting to look like a can't lose bet to more and more market participants, including dozens of national governments.

To me this explains why the stock market delivered its worst month in two years in August while gold gained more than in any month since 1982.

Illusion of Recovery – Part II: Global panic into gold

Roland Flexner, Untitled, 1992

Countdown begins to re-open the gold window

"I hope the U.S. will engage in efforts and in cooperation to maintain exchange stability so we will not succumb to the temptation to sell off treasury bills and switch our funds to gold."

- Japanese Prime Minister Ryutaro Hashimoto speaking at a luncheon meeting at Columbia University, June 24, 1997

The event of a parabolic gold price rise followed by a dramatic plunge this summer raises questions that come up here from time to time since 2001 when we bought gold. Is the volatility arising from another rumor/news-driven period like so many we have witnessed in the gold market since we entered it in 2001? Or does it indicate that we entering a new stage of the process of the dissolution of the US$ Treasury based global monetary system that began in 2001? Or is a final stage in the global monetary system upon us, a sudden reversal of the epoch that began in 1980 when gold's role as a monetary asset began a slow decline and the US$ Treasury system coalesced? As long-term gold investors it is critical that we distinguish between fleeting volatility driven by government gold sales and purchase rumors, versus profound volatility that indicates a turning point in the larger trend we have tracked here since 2001.- Japanese Prime Minister Ryutaro Hashimoto speaking at a luncheon meeting at Columbia University, June 24, 1997

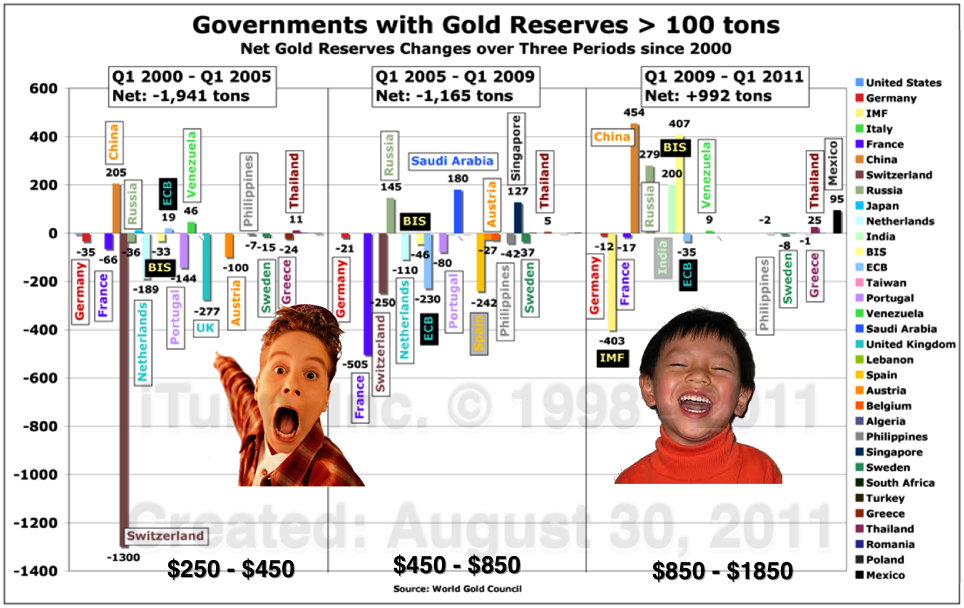

Join me for a wide ranging exploration of the gold/10-Year Treasury bond yield ratio that unveils the relationship between the new role of gold as a reserve currency anchor and the old US$ Treasury bond reserve currency anchor, of gold purchases and sales by governments and international banking institutions since Q1 2000, of the tumultuous recent history of currencies priced in gold, of the steady decline in foreign Treasury bond holdings since 2010, and of periods of severe gold price volatility going back 40 years. We conclude with a forecast of gold, stock, and precious metals prices over the next six months.

One is tempted to divide the buyers and sellers during this period into two groups, smart countries that buy low and stupid countries that sell low, but as we'll see the divide is not intellectual but strictly geopolitical.

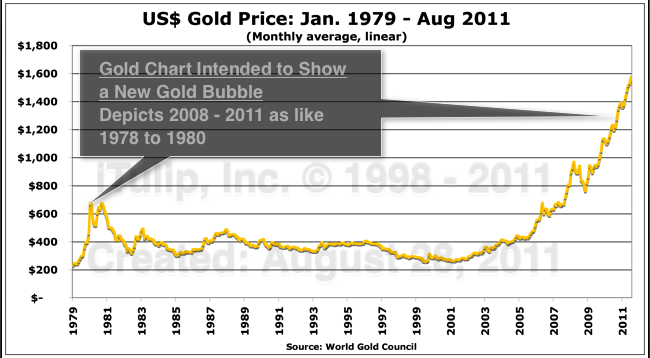

Before we get too much further into the minutiae of government gold, of who bought how much when, here are two charts to frame the discussion.

We will use them to start every article about gold going forward, to re-program readers who may have seen 100 charts elsewhere and in the MSM since their last visit here, charts that miss the true story of gold.

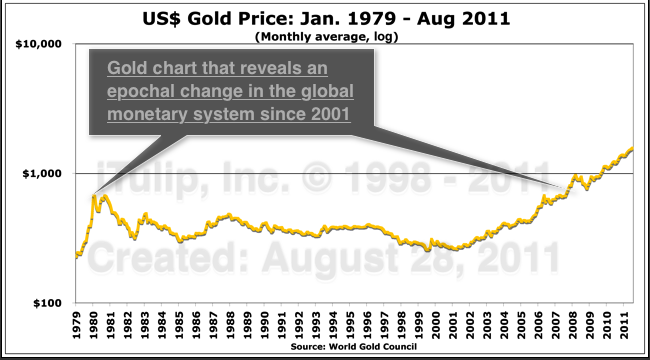

The first is the most common gold chart of all: gold prices since the gold price spike of 1979 and since.

The data are always shown on a linear scale to depict gold as a bubble of fantastic and frightening proportions today compared to the 1979 price spike.

But the chart is distorted. You cannot display a time series over such an extended period on a linear scale without exaggerating major changes that occur over long periods of time. I have made this mistake myself, such as back in 2006 when I wrote this.

Viewed on a log scale, the gold data tell a different story.

They tell us that an epochal shift in the gold market started in 2001 and has continued, with periods of volatility, at more or less the same trend rate ever since.

My theory since 2001 is that the rising gold price trend traces the gradual dissolution of the US$ Treasury system punctuated by crisis and temporary resolution.

It will eventually end with a Sudden Stop crisis that I have since 1999 called Ka-Poom Theory, possibly mitigated by a re-opening of the gold window.

The meaning of the recent gold price spike and correction is the focus of our investigation. more... $ubscription

iTulip Select: The Investment Thesis for the Next Cycle™

__________________________________________________

To receive the iTulip Newsletter or iTulip Alerts, Join our FREE Email Mailing List

Copyright © iTulip, Inc. 1998 - 2011 All Rights Reserved

All information provided "as is" for informational purposes only, not intended for trading purposes or advice. Nothing appearing on this website should be considered a recommendation to buy or to sell any security or related financial instrument. iTulip, Inc. is not liable for any informational errors, incompleteness, or delays, or for any actions taken in reliance on information contained herein. Full Disclaimer

Comment