Tweet

Tweet

|

At least one good thing came out of the housing fiasco. We’ll never have to clean up after another mess made by mortgage brokers selling liar loans to borrowers who can’t afford to repay.

No more exploitation of the dreams of new entrants to the middle class, built on the fantasy that they can afford a home that sports a price that has been inflated by decades of government loan subsidies.

No more Fed buying blown up asset-backed securities that backed bogus sub-prime mortgages to rescue banks that should be allowed to fail.

That’s all behind us. We learned our lesson! The government will prohibit these kinds of loans, prosecute violators, and never allow this mistake to happen, again.

Wait. What?

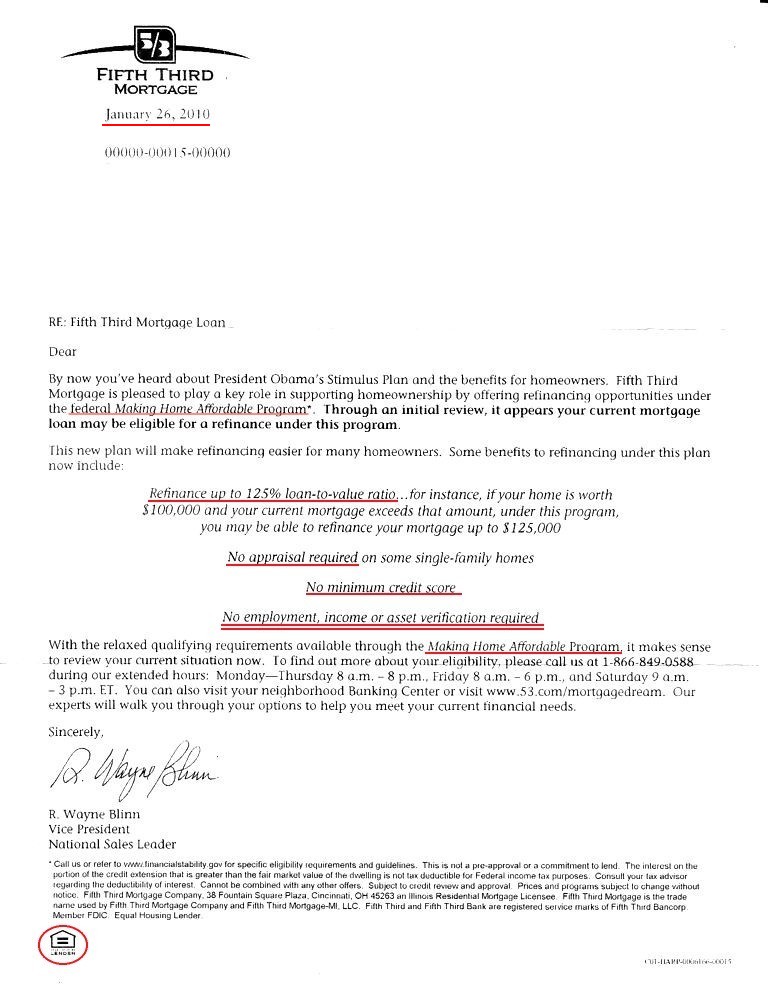

Under new The Making Homes Affordable Again to People Who Can’t Afford Them program the government is now not only allowing liar loans, it’s backing them with your tax dollars.

iTulip Select: The Investment Thesis for the Next Cycle™

__________________________________________________

To receive the iTulip Newsletter/Alerts, Join our FREE Email Mailing List

To join iTulip forum community FREE, click here for how to register.

Copyright � iTulip, Inc. 1998 - 2010 All Rights Reserved

All information provided "as is" for informational purposes only, not intended for trading purposes or advice. Nothing appearing on this website should be considered a recommendation to buy or to sell any security or related financial instrument. iTulip, Inc. is not liable for any informational errors, incompleteness, or delays, or for any actions taken in reliance on information contained herein. Full Disclaimer

__________________________________________________

To receive the iTulip Newsletter/Alerts, Join our FREE Email Mailing List

To join iTulip forum community FREE, click here for how to register.

Copyright � iTulip, Inc. 1998 - 2010 All Rights Reserved

All information provided "as is" for informational purposes only, not intended for trading purposes or advice. Nothing appearing on this website should be considered a recommendation to buy or to sell any security or related financial instrument. iTulip, Inc. is not liable for any informational errors, incompleteness, or delays, or for any actions taken in reliance on information contained herein. Full Disclaimer

:eek::mad:

:eek::mad:

Comment