Tweet

Tweet

The Hard Way or the Harder Way

Two Options for Correcting Global Economic Imbalances

By Eric Janszen

September 28, 2006

In one of my previous commentaries on this subject, "The Coming End of the US Foreign Investment Bubble" I make the case that foreign investment in the US is mostly driven by belief versus fundamentals. In "China vs USA: Economic M.A.D." I describe the unstable and unsustainable economic interdependency between the US and its major goods trading partners, especially China. I occasionally run across thoughtful arguments to the contrary, such as the Deloitte Research Study, Global Economic Outlook 2007: "Is a crisis imminent, or are things better than we thought? (pdf)."

The Deloitte study makes the argument for a benign correction of global imbalances, what I will call the Easy Way. They frame their case like this.

The US invests far more than it saves (its current account deficit) and the rest of the world saves far more than it invests (a current account surplus). This is the big imbalance in the global economy. It involves a massive flow of capital to the US from the rest of the world. The magnitude of this transfer is unprecedented in recent history and probably cannot be sustained indefinitely. Therefore, when it ends, it could have a destabilizing effect on the global economy, if only because of the shifting of gears.

Some pundits argue that financial market participants recognize this fact and will ultimately move exchange rates and interest rates in a direction that will lead to a decline in the imbalance. The pessimists argue for a sudden decline, the optimists for a gradual decline. In either case, the imbalance has persisted far longer than anyone expected, and a correction, with or without onerous consequences, has not yet happened. Perhaps we have entered a "New Era"–a rhetorical red flag if ever there was one–which massive one-way capital flows can take place for long periods without any serious consequences.

The Deloitte report does not argue that the imbalance is sustainable, but asks: "Is the terrifying hard landing imminent or not?" In other words, is there an Easy Way?

They describe two schools of thought, the "Pessimists" and the "Optimists":

Pessimists

Optimists

There is one glaring problem with this framework, and most long time iTulip readers no doubt caught it. The "historical precedent for large, sustained, one-way capital flows" between Great Britain and the US, Canada, Australia, and the rest of the British Empire" were capital flows going in the opposite direction. The standard of living of Great Britain's citizens did not depend on its colonies' need to fund the consumption of the goods they produced with the savings they earned through trade. The relationship between the US and its trading partners is not between an empire and its colonies. The relationship is a reverse variant, best described as global vendor-finance, with the US in the role of a national "company town" owned by its goods exporting, financial assets purchasing trading partners.

The Deloitte study asserts that there are elements of truth in both the Optimist and Pessimist arguments. "Asia is certainly prone to excess savings, while the US seems prone to excess borrowing. Perhaps the best explanation of the current situation is that the US and Asia have a comfortable symbiosis." The report concludes: "The US can engage in wanton profligacy largely because Asians have so much savings to dispose of."

They are wrong. There is no Easy Way. This proposal of the Easy Way reminds me of the "soft landing" arguments I'd get back in the late 1990s when I was writing about the stock market bubble and the "soft landing" arguments I got in 2004 and 2005 when I was writing about the housing bubble (see some of the nasty-gram comments).

I understand why. Bubbles are belief systems. You cannot reason a person out of a belief that he or she did not arrive at by reason, particularly if they have money, reputation, or employment–or all three–that depend on the asset in question: dot com or telecoms stocks, or housing, or dollar denominated assets–or all three. A man or woman with everything on Number Seven has got to believe that Seven is their lucky number. Or that they are not betting at all but are "investing" in the latest New Era.

But there is no Easy Way. There is only the Hard Way and The Harder Way. Here's why.

Asian countries and their citizens have a lot savings. That begs the question: Why? Top three reasons:

The US is running the largest trade and fiscal deficits in history, and its citizens have a negative savings rate. But, why? Top three reasons:

A nation of financially fearless citizens is both good and bad. Good, because it encourages the risk-taking that has made the US the engine of innovation. Bad, because–when the imbalances correct–either the Hard Way or the Harder Way, many citizens are woefully unprepared.

The US government doesn't provide incentives for its citizens to save. Instead, it demands that its trading partners–China especially–motivate its citizens to save less and "allow" their currency to appreciate.

US politicians claim that Chinese currency appreciation will solve everything: Chinese households will save less and consume more. They will buy more, cheaper US exports. US households will consume fewer, more expensive exports, and thus save more.

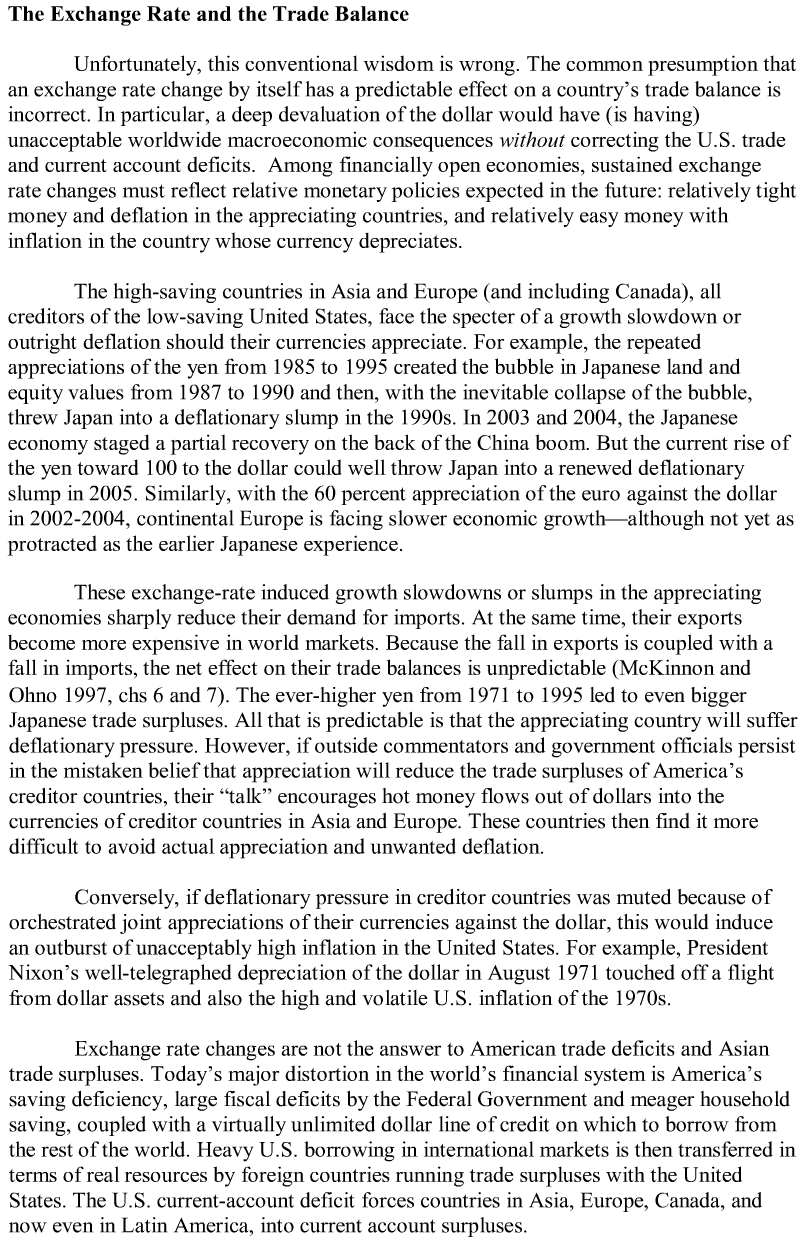

But as explained in this paper by Stanford professor Ronald MacKinnon "Exchange, Wage Rates and International Adjustment" in December 2004, currency appreciation by key US trading partners China and Japan will not solve the US trade imbalance.

Currency appreciation by China will expose it to the kind of deflation that Japan suffered in the 1990s. Japan fell for the same bad advice from the US in the late 1980s, and for the same reasons: the US was running a huge trade deficit with Japan because Japan exported and saved, and the Japanese people worked, produced, and saved, while the US government spent and borrowed, and its citizens borrowed and borrowed some more.

MacKinnon's paper predicted that the US policy of dollar depreciation undertaken around 2002 to help re-start the US economy after the post stock market crash recession was not going to help improve the US trade imbalance, as the US government believed. MacKinnon warned that the policy might make it worse. It did. While a euro went from buying $0.78 worth of US exports in 2001 to $1.12 in 2005, the US trade deficit grew from $436 billion in 2001 to $651 billion in 2005.

That's not how it's supposed to work.

The answer to the global savings imbalance is as complicated as it is painless–it is neither. The imbalance will correct, sooner or later, the Hard Way or the Harder Way.

Professor of economics Laurence J. Kotlikoff in his paper "Is the United States Bankrupt? (pdf)" explains the Hard Way.

What's the Harder Way? As the IMF stated in its Global Financial Stability Report last week: "A low-probability but potentially high-cost risk to the global financial system is that a dollar decline could become self-reinforcing and hence disorderly.'' Rapidly rising inflation, interest rates and unemployment, attended by series of recessions at least as severe as those that happened between 1980 - 1983.

The idea that there is an Easy Way, as the Deloitte Research Study suggests, is politically convenient but requires a new New Era in global economics and trade. Even to buy the Hard Way argument you have to believe that intellectual honesty will return to the political establishment and that the political will to legislate Hard Way policies will emerge before Mr. Market fixes the imbalances the Harder Way.

I contributed to America\'s Bubble Economy: Profit When It Pops because I do not expect to see intellectual honesty and strong political will–from either Republicans or Democrats–return without a crisis to motivate it, and I want iTulip readers to have a specific, actionable plan to address the risks posed to them and their families.

because I do not expect to see intellectual honesty and strong political will–from either Republicans or Democrats–return without a crisis to motivate it, and I want iTulip readers to have a specific, actionable plan to address the risks posed to them and their families.

Join our FREE Email Mailing List

Copyright � iTulip, Inc. 1998 - 2006 All Rights Reserved

All information provided "as is" for informational purposes only, not intended for trading purposes or advice. Nothing appearing on this website should be considered a recommendation to buy or to sell any security or related financial instrument. iTulip, Inc. is not liable for any informational errors, incompleteness, or delays, or for any actions taken in reliance on information contained herein. Full Disclaimer

Two Options for Correcting Global Economic Imbalances

By Eric Janszen

September 28, 2006

In one of my previous commentaries on this subject, "The Coming End of the US Foreign Investment Bubble" I make the case that foreign investment in the US is mostly driven by belief versus fundamentals. In "China vs USA: Economic M.A.D." I describe the unstable and unsustainable economic interdependency between the US and its major goods trading partners, especially China. I occasionally run across thoughtful arguments to the contrary, such as the Deloitte Research Study, Global Economic Outlook 2007: "Is a crisis imminent, or are things better than we thought? (pdf)."

The Deloitte study makes the argument for a benign correction of global imbalances, what I will call the Easy Way. They frame their case like this.

The US invests far more than it saves (its current account deficit) and the rest of the world saves far more than it invests (a current account surplus). This is the big imbalance in the global economy. It involves a massive flow of capital to the US from the rest of the world. The magnitude of this transfer is unprecedented in recent history and probably cannot be sustained indefinitely. Therefore, when it ends, it could have a destabilizing effect on the global economy, if only because of the shifting of gears.

Some pundits argue that financial market participants recognize this fact and will ultimately move exchange rates and interest rates in a direction that will lead to a decline in the imbalance. The pessimists argue for a sudden decline, the optimists for a gradual decline. In either case, the imbalance has persisted far longer than anyone expected, and a correction, with or without onerous consequences, has not yet happened. Perhaps we have entered a "New Era"–a rhetorical red flag if ever there was one–which massive one-way capital flows can take place for long periods without any serious consequences.

The Deloitte report does not argue that the imbalance is sustainable, but asks: "Is the terrifying hard landing imminent or not?" In other words, is there an Easy Way?

They describe two schools of thought, the "Pessimists" and the "Optimists":

Pessimists

- The imbalance is due to the sins of Americans. That is to say, American consumers save too little and borrow too much, while their elected government does much the same. The result is a need to import capital from overseas in order to maintain the American standard of living. The argument is that the imbalance will become unsustainable once the rest of the world becomes reluctant to finance America’s largesse. At that point, the dollar will drop and interest rates will soar, pushing the US into a recession and wreaking havoc on the global economy. Indeed Deloitte Research has warned of this outcome in past publications.

- There is historical precedent for this scenario. In the late 1970s and again in the late 1980s, a large US current account deficit was ultimately unwound through large dollar depreciations, rising interest rates, and recessions. This was followed by financial crises in emerging markets.

- The pessimists believe that this could happen again, but possibly on a larger scale.

Optimists

- Believe that the imbalance is principally due to excessive saving in Asia. For a variety of reasons, Asian consumers and businesses save far more than the demand for investment in their countries. They must therefore find outlets for this excess savings. The US is only too happy to import the excess savings given its propensity for budget deficits and consumer debt. Importing this capital enables the US to run large budget deficits combined with low personal savings without having to endure higher interest rates. The imbalance is Asia’s fault and that it will persist as long as Asia continues its excessive saving.

- There is historical precedent for large, sustained, one-way capital flows. In the late 19th century, massive amounts of capital flowed from Great Britain to the New World (US, Canada, Australia, and the rest of the British Empire). These flows, as a share of GDP, were much larger than what we see today and persisted for decades.

- There is nothing so bad about the current situation and that it can persist for much longer.

There is one glaring problem with this framework, and most long time iTulip readers no doubt caught it. The "historical precedent for large, sustained, one-way capital flows" between Great Britain and the US, Canada, Australia, and the rest of the British Empire" were capital flows going in the opposite direction. The standard of living of Great Britain's citizens did not depend on its colonies' need to fund the consumption of the goods they produced with the savings they earned through trade. The relationship between the US and its trading partners is not between an empire and its colonies. The relationship is a reverse variant, best described as global vendor-finance, with the US in the role of a national "company town" owned by its goods exporting, financial assets purchasing trading partners.

The Deloitte study asserts that there are elements of truth in both the Optimist and Pessimist arguments. "Asia is certainly prone to excess savings, while the US seems prone to excess borrowing. Perhaps the best explanation of the current situation is that the US and Asia have a comfortable symbiosis." The report concludes: "The US can engage in wanton profligacy largely because Asians have so much savings to dispose of."

They are wrong. There is no Easy Way. This proposal of the Easy Way reminds me of the "soft landing" arguments I'd get back in the late 1990s when I was writing about the stock market bubble and the "soft landing" arguments I got in 2004 and 2005 when I was writing about the housing bubble (see some of the nasty-gram comments).

I understand why. Bubbles are belief systems. You cannot reason a person out of a belief that he or she did not arrive at by reason, particularly if they have money, reputation, or employment–or all three–that depend on the asset in question: dot com or telecoms stocks, or housing, or dollar denominated assets–or all three. A man or woman with everything on Number Seven has got to believe that Seven is their lucky number. Or that they are not betting at all but are "investing" in the latest New Era.

But there is no Easy Way. There is only the Hard Way and The Harder Way. Here's why.

Asian countries and their citizens have a lot savings. That begs the question: Why? Top three reasons:

- With respect to national savings, Asian economies are organized around production and export; goods flow out and money flows in.

- National income earned from trade is used by Asian central banks to purchase US debt to the extent necessary to keep US interest rates low and the dollar strong so that US consumers can borrow money to buy their exports, and keep those exports cheap by exchanging their own currencies for dollars when they buy US financial assets.

- With respect to household savings, history and culture are the main cause. According to this December 2004 McKinsey report: "In China... the savings rate climbed to 44 percent of GDP last year, as opposed to 26 percent in Taiwan and 32 percent in South Korea. In big cities, such as Beijing and Shanghai, savings rates are as high as 50 percent, reflecting the consumers' propensity to save a higher proportion of their growing household income." The reason? "Few Chinese consumers, unlike their Western counterparts, are afraid of losing their jobs. Thanks to a booming economy, members of China's middle class are confident they can secure new employment almost at will and often at higher salary levels. But they do worry about a potential increase in health care, pension, and private-education expenses. Many estimate these potential costs to be much higher than they are likely to be. The instincts of these people have told them to save against the extreme case rather than the more likely outcome. As a result, they are over-saving for future events given what they would really have to pay if they could share risk through quality pension programs or health insurance products."

The US is running the largest trade and fiscal deficits in history, and its citizens have a negative savings rate. But, why? Top three reasons:

- With respect to national savings, the US economy is organized around domestic consumption, the inflating and trading of inflated assets among its citizens and the sale of financial assets to foreigners–the asset-based economy.

- Much of the resulting international obligations are denominated in our own home currency. This means that when international debts are paid to foreigners they are paid in US currency rather than foreign currency. This relieves the US from the need to sell products abroad to acquire sufficient foreign currency to repay its debts. The status if the US dollar as the world's reserve currency is the other reason why the US economy has gotten away with running the levels of trade deficits it has to date, besides the desire by exporting countries to continue to grow their economies via exports.

- With respect to household savings–again–history and culture are the main cause. As readers know, during the housing bubble, household savings in the US turned negative for the first time since The Great Depression. The official reason is that home owners came to believe that they didn't need to save income–all they had to do to build savings was sit on the couch and let the house do the saving for them. But the real historical and cultural reasons are the same that cause so many US citizens to go into debt, home or not. Unlike their counterparts in Asia who "worry about a potential increase in health care, pension, and private-education expenses" and whose "instincts ... have told them to save against the extreme case rather than the more likely outcome," US citizens simply cannot imagine a time when having debt and no savings can mean real hardship. The US has had only a couple of minor recessions since the early 1980s. That means that if you were born in the US since 1970 or so, you likely have no personal experience with economic hardship. Even if you were born earlier, you've likely forgotten what it was like because the last truly painful recession happened twenty five years ago. In the mean time, fresh credit seems to always be available, and while the job market can get tough, it has not left thousands of people camping on the White House lawn.

A nation of financially fearless citizens is both good and bad. Good, because it encourages the risk-taking that has made the US the engine of innovation. Bad, because–when the imbalances correct–either the Hard Way or the Harder Way, many citizens are woefully unprepared.

The US government doesn't provide incentives for its citizens to save. Instead, it demands that its trading partners–China especially–motivate its citizens to save less and "allow" their currency to appreciate.

US politicians claim that Chinese currency appreciation will solve everything: Chinese households will save less and consume more. They will buy more, cheaper US exports. US households will consume fewer, more expensive exports, and thus save more.

But as explained in this paper by Stanford professor Ronald MacKinnon "Exchange, Wage Rates and International Adjustment" in December 2004, currency appreciation by key US trading partners China and Japan will not solve the US trade imbalance.

Currency appreciation by China will expose it to the kind of deflation that Japan suffered in the 1990s. Japan fell for the same bad advice from the US in the late 1980s, and for the same reasons: the US was running a huge trade deficit with Japan because Japan exported and saved, and the Japanese people worked, produced, and saved, while the US government spent and borrowed, and its citizens borrowed and borrowed some more.

MacKinnon's paper predicted that the US policy of dollar depreciation undertaken around 2002 to help re-start the US economy after the post stock market crash recession was not going to help improve the US trade imbalance, as the US government believed. MacKinnon warned that the policy might make it worse. It did. While a euro went from buying $0.78 worth of US exports in 2001 to $1.12 in 2005, the US trade deficit grew from $436 billion in 2001 to $651 billion in 2005.

That's not how it's supposed to work.

The answer to the global savings imbalance is as complicated as it is painless–it is neither. The imbalance will correct, sooner or later, the Hard Way or the Harder Way.

Professor of economics Laurence J. Kotlikoff in his paper "Is the United States Bankrupt? (pdf)" explains the Hard Way.

Many would scoff at this notion. They’d point out that the country has never defaulted on its debt; that its debt-to-GDP (gross domestic product) ratio is substantially lower than that of Japan and other developed countries; that its long-term nominal interest rates are historically low; that the dollar is the world’s reserve currency; and that China, Japan, and other countries have an insatiable demand for U.S. Treasuries. Others would argue that the official debt reflects nomenclature, not fiscal fundamentals; that the sum total of official and unofficial liabilities is massive; that federal discretionary spending and medical expenditures are exploding; that the United States has a history of defaulting on its official debt via inflation; that the government has cut taxes well below the bone; that countries holding U.S. bonds can sell them in a nanosecond; that the financial markets have a long and impressive record of mis-pricing securities; and that financial implosion is just around the corner.

This paper explores these views from both partial and general equilibrium perspectives. It concludes that countries can go broke, that the United States is going broke, that remaining open to foreign investment can help stave off bankruptcy, but that radical reform of U.S. fiscal institutions is essential to secure the nation’s economic future. The paper offers three policies to eliminate the nation’s enormous fiscal gap and avert bankruptcy: a retail sales tax, personalized Social Security, and a globally budgeted universal healthcare system.

The Hard Way is comprised of policies that encourage saving. This paper explores these views from both partial and general equilibrium perspectives. It concludes that countries can go broke, that the United States is going broke, that remaining open to foreign investment can help stave off bankruptcy, but that radical reform of U.S. fiscal institutions is essential to secure the nation’s economic future. The paper offers three policies to eliminate the nation’s enormous fiscal gap and avert bankruptcy: a retail sales tax, personalized Social Security, and a globally budgeted universal healthcare system.

What's the Harder Way? As the IMF stated in its Global Financial Stability Report last week: "A low-probability but potentially high-cost risk to the global financial system is that a dollar decline could become self-reinforcing and hence disorderly.'' Rapidly rising inflation, interest rates and unemployment, attended by series of recessions at least as severe as those that happened between 1980 - 1983.

The idea that there is an Easy Way, as the Deloitte Research Study suggests, is politically convenient but requires a new New Era in global economics and trade. Even to buy the Hard Way argument you have to believe that intellectual honesty will return to the political establishment and that the political will to legislate Hard Way policies will emerge before Mr. Market fixes the imbalances the Harder Way.

I contributed to America\'s Bubble Economy: Profit When It Pops

because I do not expect to see intellectual honesty and strong political will–from either Republicans or Democrats–return without a crisis to motivate it, and I want iTulip readers to have a specific, actionable plan to address the risks posed to them and their families.Join our FREE Email Mailing List

Copyright � iTulip, Inc. 1998 - 2006 All Rights Reserved

All information provided "as is" for informational purposes only, not intended for trading purposes or advice. Nothing appearing on this website should be considered a recommendation to buy or to sell any security or related financial instrument. iTulip, Inc. is not liable for any informational errors, incompleteness, or delays, or for any actions taken in reliance on information contained herein. Full Disclaimer

Comment