Tweet

Tweet

Originally posted by SalAndRichard

View Post

Originally posted by SalAndRichard

View Post

EJ does not need to share his work with anyone. Mish has a financial incentive to do so clearly.

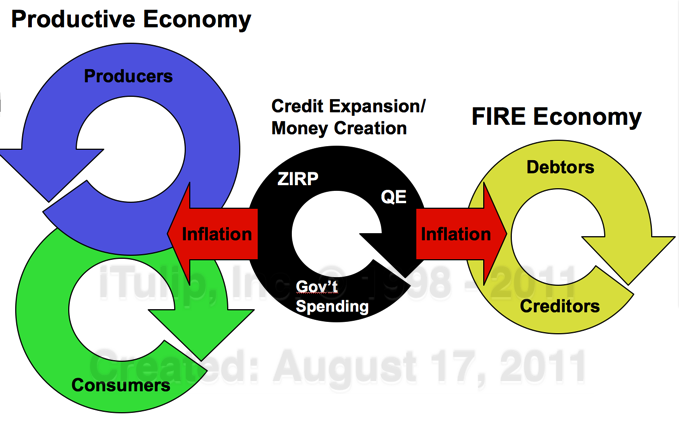

, and stated that the only way to prevent this result is to directly reduce debt levels in the FIRE Economy to eliminate the need for inflationary Fed policy to prevent debt deflation in the private sector.

, and stated that the only way to prevent this result is to directly reduce debt levels in the FIRE Economy to eliminate the need for inflationary Fed policy to prevent debt deflation in the private sector.

Comment