Tweet

Tweet

Re: A Financial Market Crash is a Process, Not an Event

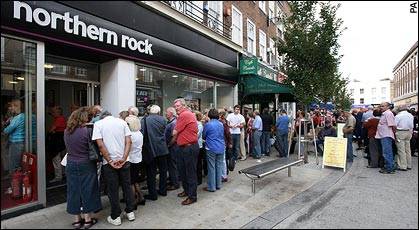

Jim, did you see the crash in T Bill rates? ... from 5% to 3.7% in the last few weeks. And then the run on banks (Countrywide) and the run on hedge funds. It appears that the fear is insolvency and default. I think the switch from risk taking to hoarding is in full gear... as well as it should be with 80 million aging boomers.

Originally posted by Jim Nickerson

View Post

Jim, did you see the crash in T Bill rates? ... from 5% to 3.7% in the last few weeks. And then the run on banks (Countrywide) and the run on hedge funds. It appears that the fear is insolvency and default. I think the switch from risk taking to hoarding is in full gear... as well as it should be with 80 million aging boomers.

Comment