Tweet

Tweet

Railway behind Walden Pond, Concord, Massachusetts, August 2012

� No QE3 but the Fed throws Bill Gross a bone

� The world's largest public housing project

� When is a bond not a bond? When it's money.

� Who just bought a pile of gold?

CI: Hope you enjoyed your summer.

EJ: I did, thanks. Hope did too and took my advice from June to rest up. I'm expecting a long, cold winter.

CI: For this interview we'll cover the state of the U.S. economy, talk about the Fed and QE, gold, housing, and the state of household balance sheets here in Part I. In Part II we cover a smorgasbord of topics, ranging from the euro to Peak Cheap Oil and conclude with your ideas about how the 30 plus year bull market in bonds ends (aka the Janszen Scenario). We'll start with your June 2012 prediction for new QE3 until "The White of Their Eyes," that is, not until a clear and present crisis will the Fed act. That is absolutely contrary to the universal belief that QE3 will be announced on September 13th. Bill Gross has staked his reputation on a QE3 announcement today. Do you still expect the Fed to hold back on the 13th? Also, after languishing in the low $1,600 range all year gold finally broke above $1,700 last week. Is that just gold hoping for more cash from the Fed along with stock market investors after the jobs report came out?

EJ: Six out of ten dentists and economists say the gold price rise was caused by the announcement of bad US employment numbers. The markets interpreted the BLS report, on top of other data that show the U.S. economy slowing, as a virtual guarantee of a QE3 announcement on the 13th. As I explained back in June, it isn't going to happen. No Fed action before the election unless there is an acute crisis. In recent weeks the financial media has talked itself into a major announcement from the Fed on Thursday. I think Gross took the lead or has been the most outspoken. I think they are going to be disappointed. We may get a minor tweak to policy, like an extension of an existing program, but nothing new. However, the impact of that disappointment will not be the same for the stock market as for the gold market because stock prices and gold prices moved at different times and for different reasons over the past two weeks. Gold will move but not as much as stocks. Keep in mind that short-term forecasting is not my forte, but that's how I see it.

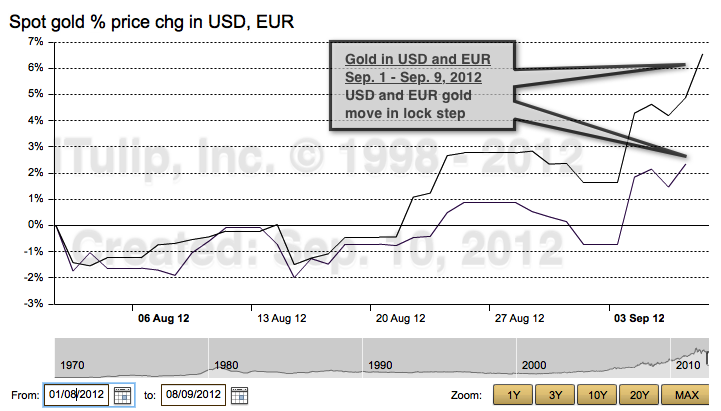

CI: Gold did not rise on September 4 on QE3 hopes?

EJ: The problem with the theory that a bad jobs numbers report was the gold price rise catalyst is that if that were the case the dollar (USD) price of gold should have risen more than the euro (EUR) price because a promise by the central bank print more money should cause the dollar to weaken relative to the euro (EUR), which had recently strengthened versus the USD anyway because of the ECB�s promise to buy euro bonds until the cows come home to ease the euro zone liquidity crisis. Instead gold went up in both EUR and USD in equal amounts at the same time.

The theory that last week�s US jobs numbers were the news that moved gold doesn�t jibe

with gold's jump in both USD and EUR.

Overall the USD and EUR price of gold have been tracking closely all year,

although the dollar price of gold diverged somewhat from the euro gold price in May.

CI: If not the promise of QE3 then what made gold go up in dollars and euros that day?

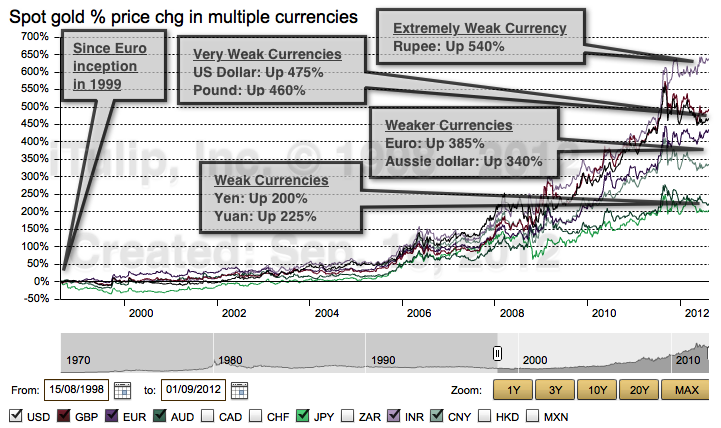

EJ: Before I answer that and give you my theory on that, as our man Finster frequently reminds us, thinking of the gold price in terms of currencies is the wrong way to think about gold. Gold, as the only commodity held as a currency reserve by global central banks, is the base currency against which all government issued currencies are valued. Gold gives central banks essential liquidity in times of loss of confidence in government issued currencies. The question is not how many ounces of gold you can buy with 10,000 USD or 10,000 EUR but how many units of each currency are needed to buy an ounce of gold. This may seem like a meaningless rhetorical distinction but the difference is important.

Looking at the chart above we can see that more and more units of all currencies have been needed to buy an ounce of gold since 2001 when we took our gold position. Every currency is weakening relative to the base currency, but not all at the same rate.

Now, you often hear it said that the USD as the least-worst currency. But this formulation, despite constant repetition, is incorrect. In reality the world�s two parallel currencies, the USD and EUR, are the two weakest among major currencies in terms of the number of units required to buy an ounce of gold. A parallel currency is one that is used by countries other than the issuer to settle international trade, such as when Japan buys oil from the Saudis and pays in USD or India buys oil from Iran and pays in EUR. For comparison purposes above, we show that the rupee was doing about as well as the EUR and USD until 2011 when it took a dive, but the rupee is not considered a major currency.

I�m repeating a point I�ve made before because it�s important from the standpoint of the Janszen Scenario. The world�s two parallel currencies, the USD and EUR, are weaker than non-parellel major currencies because the US and Europe are issuing too much money in the form of near zero interest rate bearing government bonds. When I say money rather than bonds I am referring to a side-effect of government bond price fixing that Milton Friedman and Anna Jacobson Schwaartz note in "World War II Inflation, September 1939 to August 1948." It was the last previous period when the Fed and Treasury fixed bond prices.

In April 1942, the Federal Open Market Committee announced that it would keep the rate on Treasury bills, mostly 90-day maturities, fixed at 3/8 of one per cent per year by buying or selling any amount offered or demanded at that rate.

That rate was kept fixed until the middle of 1947. No such rigid commitment was made for other government securities but an effective pattern was established for them as well�ranging from roughly 7/8 of one per cent for certificates to 0.9 per cent for 13-month notes, 1.5 per cent for 4-1/2-year notes, and 2.5 per cent for longterm bonds.

The System bought whatever amount of these securities was necessary to prevent their yields from rising but did not commit itself to sell them freely in order to prevent yields from falling. The relatively fixed pattern of rates on government securities was the counterpart in World War II of the relatively fixed discount rate in World War I. The support program converted all securities into the equivalent of money.

One of many unintended consequences of the Fed and Treasury fixing Treasury bonds at high prices and low yields -- the Fed prefers the more polite term "yield curve shaping" -- is that this policy turns bonds into money. The implication of that is that these bonds, even long-dated bonds, are not treated by investors like bonds that are for the most part held to maturity. Instead these securities behave like cash. Not a problem when inflation expectations are low, but when inflation expectations rise the bonds that act like money are exchanged for assets that are more likely to preserve purchasing power.

CI: What happened in the 1940s after the war ended when the U.S. government stopped rigging the bond market?

EJ: In the 1940s the risk of a sudden selloff was far more limited than today for several reasons. First because most of the bonds were held domestically. Second the exchange rate was fixed at the time; the small portion of overseas UST holdings did not impact, nor where they impacted by, the exchange rate. Today that is not the case. Today a sell-off can become self-reinforcing with a rise in inflation expectations setting off a run on near zero interest rate bonds, causing the currency -- the dollar in the US case or the euro in the EU case -- to weaken, raising import prices, further raising inflation expectations, and so on. In response to this risk, central banks hedge declines in the value of EUR and USD reserves they hold as near zero interest rate bonds by buying gold to maintain the ratio of gold to USD and EUR low interest rate bond reserves.

CI: That's interesting, especially the part about how near-zero rate bonds are money, but how does this relate the recent pop in the gold price and QE3?

EJ: When central banks on net -- some are buying while others are selling -- increase gold reserves the number of units needed to buy an ounce of gold increases for all currencies and the price of gold rises in all currencies. As you�d expect, since the purchase results in a change in the gold supply the price remains at the new higher level, with some price changes at the margin, on an all-currencies basis until either the next net positive gold purchase rumor causes a further rise or the next net negative central bank gold transactions occur -- not any time soon. Since 2009 when central banks became net buyers, the gold price has made many such step function jumps in all currencies. A Fed policy hope driven price spike, on the other hand, doesn�t tend to hold.

CI: The jump in gold in all currencies last week was the result of gold investors around the world buying in all currencies not gold investors betting that the U.S. central bank will announce QE this week. A rumor of central bank buying moved the gold market?

EJ: Yes, in my opinion. We�ll know after the Fed doesn�t announce QE3 on the 13th. That said, the gold price will likely correct somewhat in sympathy with stock prices, but the decline should not be nearly as dramatic as for stocks. We shall see.

CI: Why is the financial media so dead set on the Fed announcing QE3 this week?

EJ: As I�ve said since June when guys like Bill Gross started to talk up the idea of QE3, the Fed has no intention of unilateral action unless there is a major crisis to provide political cover, not so close to elections, and not with so little dry powder left to cope with a new crisis. Yes, the economy is slowing down. Yes, the price level is trending in a way that if it continues will take the CPI below the Fed�s stated 2% goal. Nonetheless the Fed has to wait. Besides, QE1 and QE2 worked as expected. They inflated financial asset prices.

CI: Explain.

EJ: Another reason why the Fed is not contemplating full-on QE3 is because QE1 and QE2 worked as intended to reflate financial assets. Bernanke stated in a press conference back in June that QE helped the U.S. economy by reflating financial asset prices. I recommend readers read the transcript of his June 2012 press conference or watch below.

Here is his exchange with the Washington Post�s Zach Goldfarb.

ZACH GOLDFARB. Mitt Romney recently said that QE2 had a relatively little impact on the economy. He said that was in part because of the President�s policies, and he said that QE3 was unwarranted and could have negative effects. Do you agree that QE2 had little effect on the economy? Do you think the President�s policies have had an effect on the effectiveness of monetary policy? And do you think it�s appropriate for a presidential candidate to comment on the future path of monetary policy?

CHAIRMAN BERNANKE. Well, I�ll just say first that we think that both of the asset purchase programs, so-called QE1 and QE2, did have significant effects on asset prices and financial conditions. And although there were certain problems in transmission�for example, the housing market has not been as responsive as it�s been in some times in the past�we do think that they were both effective in providing support for the economy, and in particular, so called QE2 ended what looked to be an incipient deflation problem when we first introduced it.

When asked of QE1 and QE2 helped the economy, Bernanke replied that QE helped the economy by inflating financial asset prices. He did not say QE added jobs or help businesses. Here's why the Fed thinks inflating financial assets makes good Fed policy.

FINANCIAL WEALTH, AGGREGATE DEMAND DETERMINANT:

One of several specific aggregate demand determinants assumed constant when the aggregate demand curve is constructed, and that shifts the aggregate demand curve when it changes. An increase in financial wealth causes an increase (rightward shift) of the aggregate curve. A decrease in financial wealth causes a decrease (leftward shift) of the aggregate curve. Other notable aggregate demand determinants are interest rates, federal deficit, inflationary expectations, and the money supply.

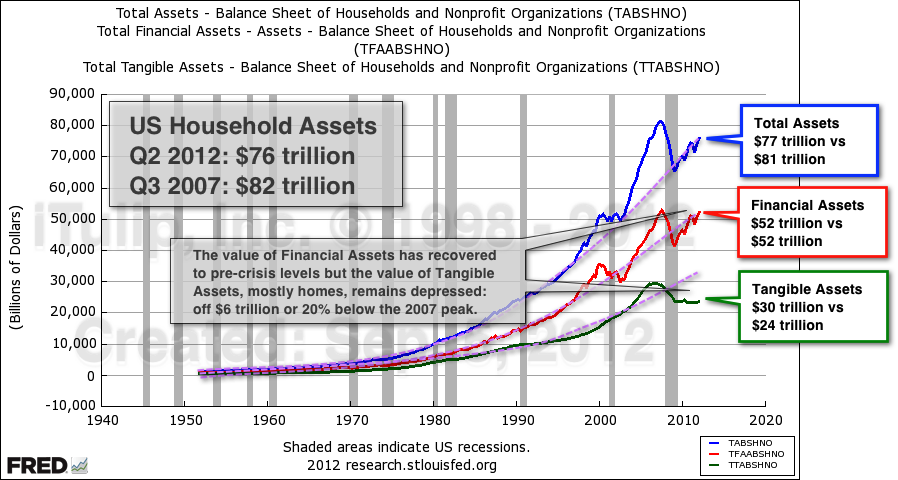

The goal of QE1 and QE2 was to inflate the price of financial assets to repair the assets side of household balance sheets that was wrecked by the crash. Inflating financial assets increases aggregate demand via positive wealth effects. This is standard economic theory. Insofar as the goal was to reflate financial assets, QE1 and QE2 worked.

The financial assets of households have recovered to pre-crisis levels, but Tangible Assets, aka housing, remain depressed.

Household financial assets are now back to pre-crisis levels. So why launch a new round of QE, especially when fund managers like Bill Gross are publicly goading you into doing it?

CI: But did QE increase demand?

EJ: That's impossible to measure, but intuitively you can see that when households get quarterly statements from their investment firm and the balance is back to where it was before the crap hit the fan then they are going to tend to spend more money than they would if the statement told them they'd lost a pile of money. This helps explain why higher income household consumer spending has improved so much more than lower and middle income spending; lower and middle income households, if they have any assets, have them in real estate not in financial assets like stocks and bonds. QE is grossly regressive, but the Fed must figure it's better than nothing.

CI: What's your take on housing? Cover of this week's Barron's says the housing market is up.

EJ: To me the so-called mystery of the slow recovery is all about housing. Housing used to lead every recovery since the early 1980s. Home mortgages make up the vast majority of household liabilities. If they are not rising that means households aren't taking out new mortgages to buy homes as fast as they are paying off or defaulting on existing mortgages. The Fed can reflate financial assets by buying the bonds that underpin all asset prices. However, the Fed cannot reflate home prices. For all but the highest income groups, the crash has left US households with a collective $6 trillion hit to household assets and most of that is home values. So we have positive wealth effects for the rich and negative wealth effects for everyone else. Not too surprising, then, that the 99% versus 1% social split resonates with so many Americans. It wasn't only the crash but that combined with the regressive reflation measures that made a once unthinkable and un-American rich vs poor split in the centerpiece of campaign rhetoric.

CI: Can the U.S. economy recover without a housing recovery?

EJ: No, not the way the economy is currently structured, that is, around the Finance, Insurance, and Real Estate industries. As I said, every recovery since the start of the FIRE Economy in the early 1980s has been led by housing. The recovery from the 2001 recession was fueled by a housing bubble. Without a strong housing market the FIRE Economy cannot recover.

CI: What can be done? Can the housing market recover and the FIRE Economy take off again?

EJ: The problem is the time scale. At this rate the housing market will never recover because a new crisis is bound to come along to halt the recovery, such as it is, and set it back.

CI: What kind of time scale are we talking about.

EJ: Current course and speed, another 10 years. But I guarantee you there will be another recession before 10 years go by. Bottom line, the U.S. economy has to be restructured. The truly terrible problem for the U.S. is that the last restructuring was financed with Federal government spending. I'll get to that point in Part II when we talk about austerity measures in Europe versus the economic restructuring that the U.S. went through in the 1980s and Germany in the 1990s.

Two factors are keeping housing depressed, one on the credit availability side and the other on the housing demand side.

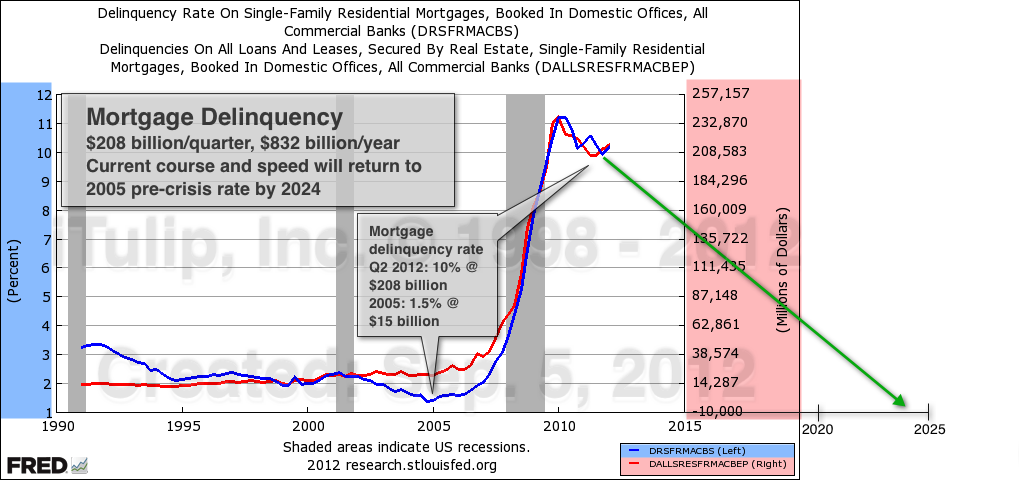

A broken home finance industry on the credit availability side keeps lending standards high even if mortgage interest rates are low. Again, it's a rich man's verus poor man's housing market. It's easy to get a loan to buy a home if you are one of the few who made it through the recession with a strong credit and employment history. Everyone else is having a hell of a time getting a mortgage. The reason for the broken home finance industry is visible in the persistently high mortgage delinquency rate. Hard to imagine but three years into the so-called recovery home owners go delinquent on more than $200 billion in loans every single quarter, that's up from an average of $15 billion per quarter from 1990 until 2005.

Current course and speed, no return to historical delinquency rates until 2024.

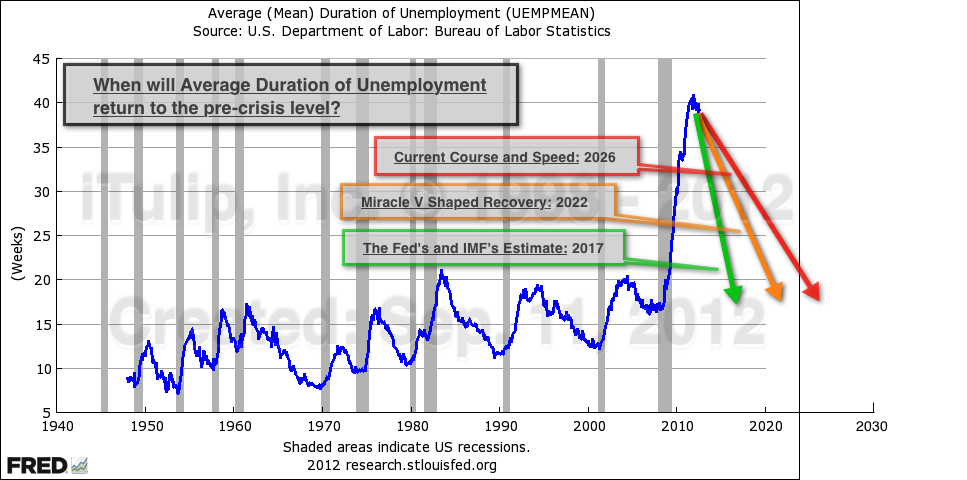

Mortgage credit isn't going to loosen up until delinquency rates fall, and delinquency rates are not going to get better until the labor market improves. The improvement in the mortgage delinquency rate can only be as rapid as the rate of improvement in long term unemployment.

Current course and speed, no return to historical average duration of unemployment until 2026.

I think we're stuck with this screwed up home finance market for many years to come, which is why the Treasury threw in the towel week before last and gave up on the idea of ever privatizing Fannie Mae and Freddie Mac. There is no hope for a private secondary market for US housing until 2020 at the earliest.

Fannie and Freddie: The Walking Dead

By Deborah Solomon Aug 17, 2012

After nearly four years of a zombie existence, the U.S. Treasury Department finally pulled the trigger on Fannie Mae and Freddie Mac.

In revising the terms of the companies' bailouts, the Treasury is ensuring the mortgage giants never resume their heady roles as private companies. It's an ironic twist for Fannie and Freddie, which once employed armies of lobbyists to protect their status.

Under the new arrangement, the companies will not be able to keep a single dime of profit they earn -- the money will all flow back to the U.S. Treasury. The move, which also requires Fannie and Freddie to shrink their mortgage portfolios more quickly, is intended to hasten reform of the housing finance market, which is almost completely dependent on the U.S. government.

CI: If the housing finance market is almost completely dependent on the U.S. government, doesn't that make the U.S. housing market government dependent?

EJ: I refer to U.S. residential real estate as the world's largest government housing project. No surprise; I told Perter Warburton in 2008 that this was the inevitable outcome of the housing bubble.

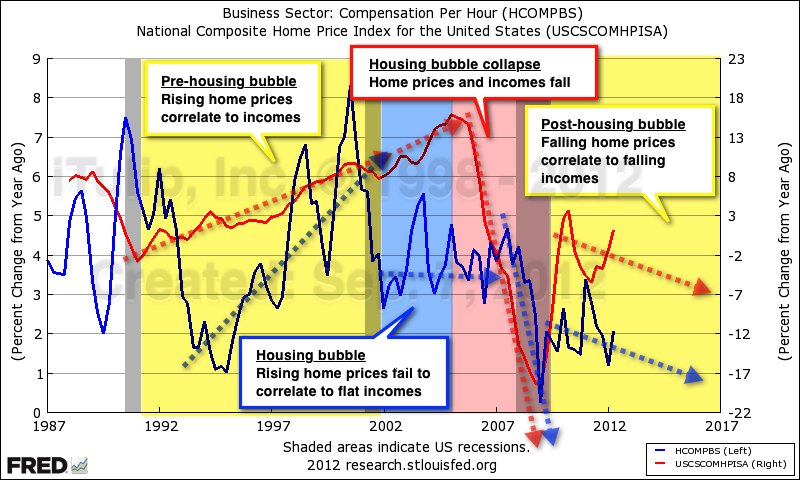

After the credit market problem, the second and more daunting issue for the housing market is on the demand side, with employment and incomes. Before the housing bubble home prices correlated to regional incomes. One of the ways we identified the start of the bubble in 2002 was that home prices had de-coupled from regional incomes. Incomes flattened out after the stock market bubble crashed and caused a mild recession, but that dip in incomes didn't impact home prices because the Fed got busy inflating a housing bubble. Then, after that bubble collapsed, home prices once again correlated to incomes. First housing prices tracked a collapse in incomes. Today they track a steady decline in incomes.

CI: The good housing news is that rise we see on your chart? And you are saying then that rise is temporary?

EJ: Without a rise in incomes across the board there will be no sustained housing recovery. Period. Instead we'll have an economy like that of any other third world country. Poor and middle income neighborhoods will get shabbier and wealthy neighborhoods will get more opulent. Add gates at the entrances and bars on the windows and the process of turning the US into a third world country is complete,

CI: You show QE as beefing up the assets side of the household balance sheet, for those who have financial assets. What about net worth overall?

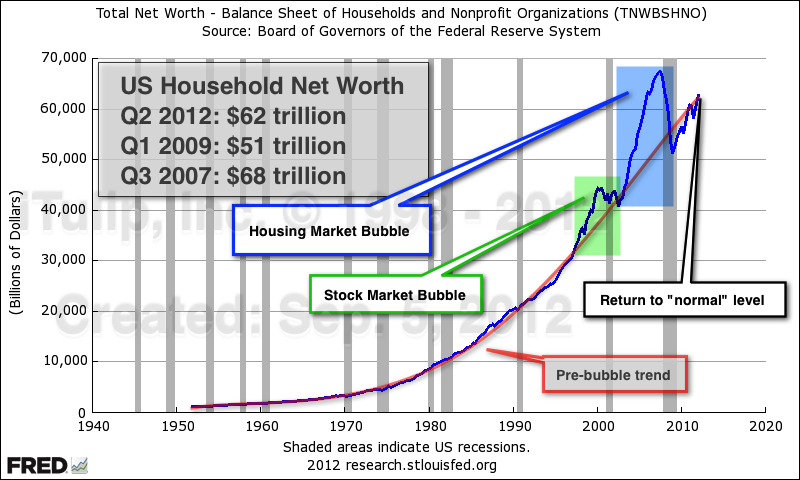

EJ: Peak to trough we're talking about a $16 trillion decline in household net worth from $68 trillion to $52 trillion. As of Q2 2012 households made back $10 trillion of that; now its off $6 trillion from the peak.

CI: From the chart above, household net worth is where is should be if the stock market and housing bubbles didn't happen?

EJ: Absolutely. That looks encouraging, but before we break out the champaign we have to consider the way it recovered. Big gains in financial assets on the asset side of the balance sheet, thanks to the Fed, contributed to the net but liabilities have staged an historic decline.

CI: You mean de-leveraging? Isn't that good?

EJ: Not the way our economy is structured it isn't. The portion of the increase in net worth is happening on the liabilities side of the balance sheet. It's not a huge number relative to $62 trillion in total net worth. It's only about $1 trillion but again it's all about the housing market. Most of the household liabilities number is home mortgages. We are seeing an historically anomalous decline in home mortgage liabilities as home owners continue to default and repay mortgages faster than they take out new ones. The chart below shows periods of de-leveraging of liabilities since the early 1950s. You can hardly make out any decrease at all. That all changed in 2007. We cannot call what is happening to the liabilities side of the household balance sheet "de-leveraging." It's collapsing. It's collapsing because the price of the collateral that backs the mortgages -- homes -- is collapsing.

CI: That looks ominous.

EJ: But it's inevitable; as home prices fall so will mortgage debt.

By the way, we've stopped using the Case-Shiller home price indexes that are so popular with most of the financial media. We prefer the index built of actual home sale transactions. It's more reliable even if it doesn't supply fodder for the endless debate about the bottom of the housing market. As you can see there are no bounces in the transactions data but a continuous decline.

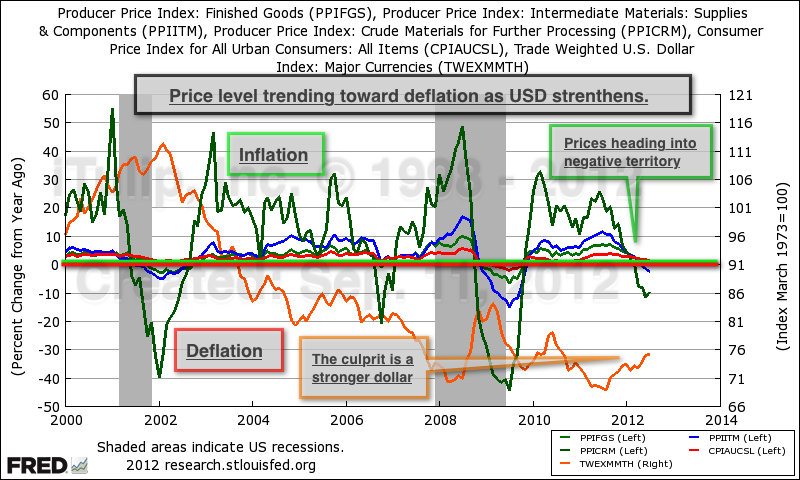

CI: In one chart, what's the inflation picture? Rising or falling the rest of 2012?

EJ: Prices are heading into negative territory. The reason is that the dollar has been allowed to strengthen since Q4 2011.

CI: I can't believe my ears. Are you forecasting deflation?

EJ: Don't worry, they'll think of something to reduce demand for dollars. It's not so hard to do when the world is swimming in them already. I'm expecting some kind of surprise policy move after the election. I don't yet know what they're planning to do but it will be novel. I'll let readers know if I can collect enough hints from enough contacts to figure it out.

CI: Sum it up for us.

EJ: Again, our economy structured around FIRE. Recovery all about real estate at this point. The home price index, the delinquency rate, household liabilities, and average duration of unemployment tell us everything we need to know about the state of the US economy. In sum:

1. The collapse of the housing bubble and resulting recession wrecked the market for home mortgage finance. Combined with high unemployment, housing has been eliminated as a driver of economic recovery.

2. Without the stimulus of the housing market unemployment will remain high and demand will remain weak.

3. QE can reflate financial assets but not home prices. For that we need declining unemployment and rising incomes first and a functioning mortgage finance market second.

4. QE can only stimulate demand by inflating financial assets to stimulate demand via positive wealth effects. It's regressive and its work has been done.

5. The one and only avenue for stimulus remaining with interest rates at zero is additional deficit spending.

6. Additional fiscal stimulus will further worsten the US fiscal position, cause the dollar to weaken, stimulate exports, raise commodity prices and prices in the economy.

7. But deficit reduction is an election platform for both candidates, so none until after the election. After the election, we will see more fiscal stimulus no matter which party is elected.

CI: So no QE3 and yes to more deficit spending after the election. Man, you really are a contrarian.

EJ: Not for the sake of being contrarian. I hope the data have made my case for me.

Where is all of this headed? In Part II we refine our thinking about the essential question of our time, once the historic government intervention in the UST market ends, then what? How will it end? What will end it? And, of course, when?

Election as Forcing Function - Part II: What will collapse the U.S. Treasury Bond market?

If the above image above looks familiar that may be because you have been reading this site for a long time and recall my November 1999 article published Bankrate.com titled �What will pop the Internet bubble?� The image below led the article on iTulip.com.

Investors await their fate on Wall Street: iTulip, 1999

In this section we identify two of the most likely triggers of a future collapse of the U.S. Treasury bond (UST) market. I dislike the use of the term �bubble� to describe the effect of the Fed and Treasury herding all of us en masse into a wealth destruction pit. The term "bubble" used to have a specific meaning in the context of financial markets. It used to refer to a complex process of asset price inflation wherein a group of insiders engaged the greed instinct of the great public heard of human animals with an assist by government but now refers to anything that appears excessive and temporary.

Are investors greedily piling into UST to get rich? No, today the word "bubble" doesn't mean anything.

Rather than bubble I think of the UST market as a cage that after a decade of interest rate manipulation by government is crammed to bursting with more or less the same herd as rode the rise and plunge of two bubbles in ten years.

The human is an intelligent animal but with certain weaknesses, such as the inability to make decisions independent of a bunch of other human animals, or it defers to a high ranking human animal in which, for good but usually ill, it places its trust.

In this conception of today's UST market we investigate one event that may occur to produce a panic that by the sheer force of the bodies inside the cage trying to get out causes the herd to suddenly bust the gate down and spill willy, nilly in all directions into the grounds while the keepers of the flock look on helplessly. In the second scenario the keepers by intention unlock the main gate, after carefully laying the groundwork, or so they think, convinced that by setting certain expectations of the keepers' future actions the terrified and yield-starved herd will exit in an orderly fashion, chattering and mumbling like a black tie crowd leaving a bad opera rather than screaming and turning over lit cars like a group of drunken, angry soccer fans who lost the match on the home field.

History has always proved otherwise, but (more... $ubscription)

Editor's Note: Part II is not ready for publication as of Sept. 13, 2012 8AM EDT at the time Part I was moved from the staging area to the public forums. We are taking the usual step to publish Part I before Part II is ready due to the time-sensitive nature of material in Part I in order to publish EJ's prediction for no QE3 announcement today before Bernanke's speech. Subscribers will be notified by email as usual when Part II us ready, we hope either later today or tomorrow. You may also receive notification by following EJ on Twitter.

iTulip Select: The Investment Thesis for the Next Cycle�

__________________________________________________

To receive the iTulip Newsletter or iTulip Alerts, Join our FREE Email Mailing List

Copyright � iTulip, Inc. 1998 - 2012 All Rights Reserved

All information provided "as is" for informational purposes only, not intended for trading purposes or advice. Nothing appearing on this website should be considered a recommendation to buy or to sell any security or related financial instrument. iTulip, Inc. is not liable for any informational errors, incompleteness, or delays, or for any actions taken in reliance on information contained herein. Full Disclaimer